CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

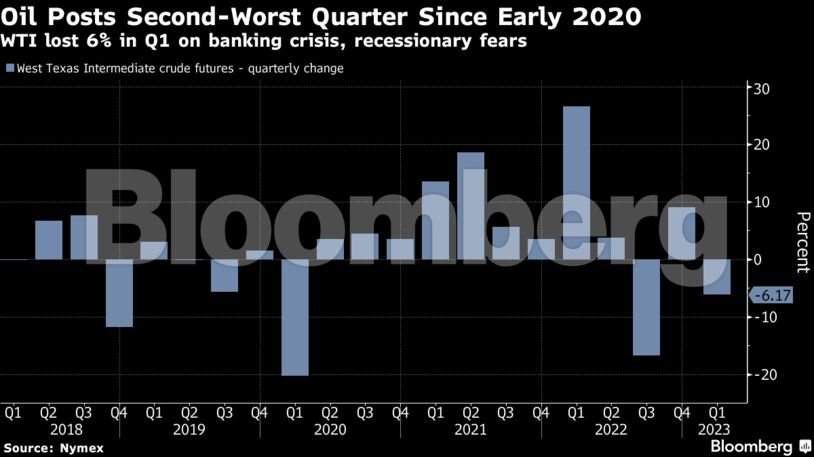

Oil fell for the fifth consecutive month, culminating in its second quarterly drop since early 2020.

Prices have slid against a backdrop of gloomy US economic sentiment and a banking crisis that rattled broader markets. While oil bulls have hung their hopes on a rebound China’s demand as it ends Covid Zero policies, the recovery has been slower than some expected.

Major banks and industry observers have issued bullish price projections for the remainder of the year, and crude posted its best week of 2023 amid disruptions to Iraqi exports. The next test for the current rally will be the 50-day moving average, which could present short-term resistance in the absence of a positive catalyst, said Rebecca Babin, a senior energy trader at CIBC Private Wealth.

“Fundamental developments such as positive non-manufacturing PMI data in China, inventory draws in the US and financial market stability, coupled with very limited long positioning, have lit a fire under crude,” Babin said.

Prices:

WTI for May delivery rose $1.30 to settle at $75.67 a barrel in New York.

Brent for May settlement, which expires Friday, gained 50 cents to settle at $79.77.

The more-active June contract advanced $1.29 to $79.89.

Share This: