CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

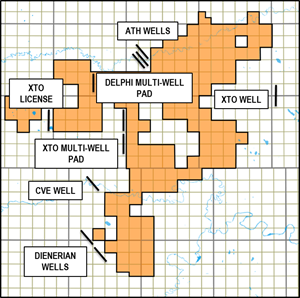

Delphi Energy Corp Adjacent Drilling Activity

Delphi Energy Corporation

CALGARY, Alberta, March 13, 2019 (GLOBE NEWSWIRE) — Delphi Energy Corp. (“Delphi” or the “Company”) is pleased to announce its financial and operational results for the year ended December 31, 2018.

2018 HIGHLIGHTS

- Successfully executed a twelve (7.80 net) well drilling program and various infrastructure projects to support future growth;

- Completed construction and commissioned the amine processing facility which has reduced natural gas processing costs and diversified Delphi’s natural gas processing options;

- Increased production by 16 percent to 9,774 barrels of oil equivalent per day (“boe/d”) from 8,401 in 2017 and increased the liquids yield from 103 barrels per million cubic feet (“bbls/mmcf”) to 113 bbls/mmcf;

- Shifted production mix to higher value commodity with a 29 percent increase in field condensate production versus a 12 percent increase in natural gas and natural gas liquids (“NGL”) production, resulting in field condensate comprising 26 percent of total production on a boe basis versus 23 percent in 2017;

- Increased annual crude oil and natural gas revenue by 25 percent over 2017 to $127.3 million due to higher production and higher realized prices before hedging for NGL and field condensate offset by a lower realized price for natural gas;

- Operating expenses per barrel of oil equivalent (“boe”) were $7.33 and $8.38 in the three and twelve months ended December 31, 2018, down 31 percent and 13 percent, respectively, in comparison to the same periods in 2017;

- Reduced general and administrative expense by 10 percent resulting in a 23 percent decrease on per boe basis;

- Realized a natural gas price including risk management and marketing income of $3.53 per thousand cubic feet (“mcf”) and $3.45 per mcf in the three and twelve months ended December 31, 2018, more than double the average price for AECO benchmark for the same respective periods;

- Realized a cash netback before risk management of $16.54 per boe in 2018 compared to a cash netback of $10.96 per boe before risk management in 2017. The increase in cash netback is principally due to a combination of higher production and stronger realized prices of field condensate and NGLs as well as cost reductions in operating, transportation and general and administrative expenses; and

- Continued to build a strong hedge book with commodity risk management contracts valued at $26.6 million as at December 31, 2018, providing protection in 2019 and into 2020 against the volatile commodity price environment.

| FINANCIAL AND OPERATIONAL HIGHLIGHTS | ||||||||||||

| Three months ended December 31 |

Twelve months ended December 31 |

|||||||||||

| 2018 | 2017 | % Change | 2018 | 2017 | % Change | |||||||

| Financial | ||||||||||||

| (Cdn, $ thousands, except per share) | ||||||||||||

| Crude oil and natural gas revenues | 26,786 | 30,896 | (13 | ) | 127,254 | 101,836 | 25 | |||||

| Net earnings (loss) | (17,318 | ) | (1,764 | ) | 882 | (26,366 | ) | 6,902 | (482 | ) | ||

| Per share – basic and diluted | (0.09 | ) | (0.01 | ) | 800 | (0.14 | ) | 0.04 | (450 | ) | ||

| Cash flow from operating activities | 9,428 | 9,490 | (1 | ) | 54,128 | 31,044 | 74 | |||||

| Per share – basic and diluted(1) | 0.05 | 0.05 | – | 0.29 | 0.18 | 61 | ||||||

| Adjusted funds flow(1) | 8,890 | 14,144 | (37 | ) | 46,615 | 36,670 | 27 | |||||

| Per share – basic and diluted(1) | 0.05 | 0.08 | (38 | ) | 0.25 | 0.21 | 19 | |||||

| Net debt(1) | 181,985 | 136,421 | 33 | 181,985 | 136,421 | 33 | ||||||

| Capital expenditures, net of dispositions | 26,942 | 42,156 | (36 | ) | 90,834 | 117,292 | (23 | ) | ||||

| Weighted average shares (000s) | ||||||||||||

| Basic | 185,547 | 185,472 | – | 185,547 | 173,171 | 7 | ||||||

| Diluted | 185,547 | 185,472 | – | 185,547 | 173,975 | 7 | ||||||

| Operating | ||||||||||||

| (boe conversion – 6:1 basis) | ||||||||||||

| Production: | ||||||||||||

| Field condensate (bbls/d) | 2,644 | 2,374 | 11 | 2,542 | 1,968 | 29 | ||||||

| Natural gas liquids (bbls/d) | 1,289 | 1,315 | (2 | ) | 1,411 | 1,250 | 13 | |||||

| Natural gas (mcf/d) | 33,063 | 35,391 | (7 | ) | 34,925 | 31,098 | 12 | |||||

| Total (Boe/d) | 9,444 | 9,588 | (2 | ) | 9,774 | 8,401 | 16 | |||||

| Average realized sales prices, before financial instruments | ||||||||||||

| Field condensate ($/bbl) | 42.66 | 64.20 | (34 | ) | 66.96 | 59.14 | 13 | |||||

| Natural gas liquids ($/bbl) | 38.87 | 47.34 | (18 | ) | 44.88 | 35.42 | 27 | |||||

| Natural gas ($/mcf) | 3.71 | 3.39 | 9 | 3.23 | 3.78 | (14 | ) | |||||

| Netbacks ($/boe) | ||||||||||||

| Crude oil and natural gas revenues | 30.83 | 35.03 | (12 | ) | 35.68 | 33.22 | 7 | |||||

| Marketing income (1) | 1.61 | 1.63 | (1 | ) | 1.41 | 0.58 | 141 | |||||

| Realized gain (loss) on financial instruments | (3.38 | ) | 1.25 | (370 | ) | (3.47 | ) | 1.00 | (445 | ) | ||

| Revenue, after realized financial instruments | 29.06 | 37.91 | (23 | ) | 33.62 | 34.80 | (4 | ) | ||||

| Royalties | (1.72 | ) | (2.26 | ) | (24 | ) | (2.08 | ) | (2.35 | ) | (11 | ) |

| Operating expense | (7.33 | ) | (10.59 | ) | (31 | ) | (8.38 | ) | (9.60 | ) | (13 | ) |

| Transportation expense | (4.43 | ) | (4.62 | ) | (4 | ) | (4.86 | ) | (5.67 | ) | (14 | ) |

| Operating netback (1) | 15.58 | 20.44 | (24 | ) | 18.30 | 17.18 | 6 | |||||

| General and administrative expenses | (1.61 | ) | (1.54 | ) | 5 | (1.61 | ) | (2.08 | ) | (23 | ) | |

| Interest | (3.80 | ) | (3.02 | ) | 26 | (3.53 | ) | (3.08 | ) | 15 | ||

| Foreign exchange gains (losses) | 0.26 | 0.15 | 73 | 0.10 | (0.06 | ) | – | |||||

| Settlement of unutilized take-or-pay contract | (0.19 | ) | – | – | (0.19 | ) | – | – | ||||

| Cash netback (1) | 10.24 | 16.03 | (36 | ) | 13.07 | 11.96 | 9 | |||||

(1) Refer to non-GAAP measures

MESSAGE TO SHAREHOLDERS

Delphi has maintained a high level of drilling activity over the past two years with 29 (18.8 net) new wells drilled, increasing the total number of wells drilled by Delphi on its 148 sections of Montney acreage to 60 over the past 6 years. This increased pace of capitalization has materially de-risked the overall acreage. The Company believes the most recent well results represent the significant value potential of West Bigstone.

Achieving success through optimizing fracture design at West Bigstone has been more challenging than it was at East Bigstone. The delineation and single well development drilling operations, with impacts to offset producing wells, has presented challenges related to producing well down time and corporate production forecasting. With recent success at West Bigstone, the Company is now positioned to move to multi-well pad operations with higher intensity fracture completion operations required to efficiently deliver superior results, while more consistently reaching production growth expectations.

Through the first half of 2019, Delphi will complete and bring on production its four-well pad in West Bigstone. Facility upgrades and pipeline construction to route the West Bigstone production to Delphi’s 7-11 facility in East Bigstone is expected to be completed in late March. Capital spending in the first half of 2019 is expected to be approximately $26 million, funded entirely from adjusted funds flow.

Beyond delivering superior well results at West Bigstone, the Company is focused on capital and operating efficiencies through pad drilling operations, increasing revenues from condensate, and continuing efforts to lower operating and general administrative costs. Drilling plans for the second half of 2019 will be funded with cash flow from operations and dependent on both commodity prices and the results of the four-well pad currently being completed. Free cash flow generated in excess of the capital program will be used to reduce bank debt. Guidance for full year 2019 is not anticipated to be released until later in the second quarter.

In 2018, the greater Bigstone area began to see new industry multi-well pad drilling activity on lands adjacent to Delphi’s West Bigstone core land position, as well as to the south in proximity to Delphi’s 100 percent owned land position. Montney development activity also continued immediately north of the Company’s lands in East Bigstone. The Company views this activity positively, both accelerating the delineation of the potential of Delphi’s lands, as well as opening up possibilities for consolidation in the greater area. David J. Reid, President and CEO stated, “While Delphi’s core strategy has been to delineate and efficiently develop its large Bigstone Montney asset, where we have a strategic competitive advantage, consolidation in the area will drive even greater efficiencies.”

Delphi remains well positioned with a high quality resource base supported by a significant infrastructure footprint and a large drilling inventory, a strategic “long Alliance Chicago” natural gas marketing strategy, and a strong commodity hedge position. The Company looks forward to providing an update to its ongoing operations in the second quarter.

OPERATING AND FINANCIAL HIGHLIGHTS FOR THE QUARTER AND YEAR ENDED DECEMBER 31, 2018

Delphi completed a $90.8 million capital program in 2018 which included the drilling of twelve (7.8 net) horizontal Montney wells, the completing, equipping and tie-in of 12 (7.8 net) wells, three of which were drilled in the fourth quarter of 2017, and various infrastructure projects including an amine facility capable of sweetening 17 (11 net) million cubic feet of raw natural gas per day for final processing at Delphi’s 25 percent owned Bigstone sweet natural gas plant.

The amine facility was commissioned and commenced operation in May 2018. The purpose of the amine facility is to reduce operating costs through reduction of third party natural gas processing fees and diversify the Company’s natural gas processing options. Initially, the natural gas sweetened in this facility and processed at the Bigstone sweet natural gas plant is being sold in the AECO market via shipment on the Nova Gas Transmission system (“NGTL”). Delphi expects that the Alliance lateral pipeline at the Bigstone plant will be reactivated in mid-2020 at which time the natural gas from this processing stream will be shipped on the Alliance pipeline system and sold in the Chicago market. Until the Alliance lateral pipeline is reactivated, Delphi expects to transport about 60 percent of its natural gas on Alliance and 40 percent on NGTL compared to about 90 percent on Alliance after reactivation of the lateral pipeline. While the greater proportion of natural gas currently shipped on NGTL results in a lower average realized price for Delphi’s natural gas, this is more than offset by lower natural gas processing and transportation costs and increased marketing income generated from Delphi’s additional excess capacity on the Alliance system.

Production in 2018 averaged 9,774 boe/d, a 16 percent increase over 2017 due to a 29 percent increase in field condensate production and a 12 percent increase in NGL and natural gas production. Production in the fourth quarter averaged 9,444 boe/d, a two percent decrease from the comparative quarter in 2017, though field condensate production was up 11 percent reflecting a shift in production mix to more valuable field condensate. Delphi’s production portfolio for the fourth quarter of 2018 was weighted 28 percent to field condensate, 14 percent to natural gas liquids and 58 percent to natural gas.

Annual crude oil and natural gas revenue was $127.3 million, an increase of 25 percent over 2017 due to higher production and higher realized prices before hedging for NGL and field condensate offset by a lower realized price for natural gas. Field condensate contributed 49 percent of crude oil and natural gas revenue while natural gas and NGL contributed 32 and 18 percent respectively. Crude oil and natural gas revenue in the fourth quarter was $26.8 million, a decrease of 13 percent over the same period in 2017 principally due to a historically wide discount of Edmonton condensate to WTI and apportionment of pipeline capacity for delivery of condensate resulting in a 34 percent decrease in the realized price before hedging of field condensate.

Operating expense in 2018 was $8.38 per boe, a reduction of 13 percent from 2017 principally due to commissioning of the amine sweetening facility which decreased natural gas processing costs per boe and expansion of the Company’s water disposal facility which decreased water trucking and disposal fees, combined with an increase in production. Transportation expense was $4.86 per boe in 2018, a reduction of 14 percent principally due to commissioning of the amine sweetening facility which resulted in a shift of some of Delphi’s natural gas from the Alliance pipeline system to the lower cost NGTL system.

The operating netback before hedging in 2018 was $21.77 per boe, an increase of 35 percent over 2017 due to higher realized prices and marketing income and lower royalties, operating expense and transportation expense. Despite lower royalty, operating and transportation expense per boe in the fourth quarter of 2018, the operating netback per boe before hedging was one percent lower than it was in the fourth quarter of 2017 due to a lower realized price for field condensate.

The cash netback in 2018 was $13.07 per boe, an increase of 9 percent principally due to a higher operating netback and lower general and administrative expenses which were partially offset by a higher interest expense and a hedging loss of $3.47 per boe versus a gain of $1.00 in the 2017.

Annual adjusted funds flow increased 27 percent from the prior year to $46.6 million. On a per share basis adjusted funds flow increased 19 percent to $0.25 per basic and diluted share.

In the fourth quarter, Delphi identified indicators of impairment primarily related to a sustained outlook for lower commodity prices and a deficiency between the market value of its outstanding common shares and the book value of its shareholders’ equity. Accordingly, Delphi performed an impairment test on its Bigstone property which resulted in a $51.0 million impairment loss. Delphi recorded a net loss of $26.4 million in 2018 compared to net earnings of $6.9 million in 2017 primarily due to the impairment loss offset by higher adjusted funds flow and a $25.8 million unrealized gain on risk management contracts.

The borrowing base of Delphi’s senior credit facility was reconfirmed at $105.0 million in the fourth quarter. Bank debt at the end of the year was $66.7 million and outstanding letters of credit were $7.5 million, leaving $30.8 million available to be drawn on the senior credit facility. Net debt at the end of the year was $182.0 million.

NATURAL GAS MARKETING

Natural gas accounted for 32 percent of crude oil and natural gas revenues in 2018.

Delphi sells natural gas in the Chicago and AECO markets. The Company sold approximately 90 percent of its natural gas in the Chicago market prior to commissioning the amine sweetening plant in May. As a result of commissioning the plant, approximately 72 percent of natural gas sales in 2018 and 62 percent of natural gas sales in the fourth quarter were in the Chicago market. Delphi expects the proportion of gas sold in Chicago will remain at about 60 percent until the Alliance lateral pipeline at the Bigstone sweet natural gas plant is reactivated, at which time it will return to approximately 90 percent.

Delphi has approximately 45.8 mmcf/d of firm service and 11.4 mmcf/d of priority interruptible service on the Alliance pipeline system and about 22 mmcf/d of firm service on NGTL. Delphi generates marketing income from its excess firm service on Alliance through temporary assignment to other shippers at a premium over cost or through the purchase of natural gas in Alberta or British Columbia for sale in Chicago.

With the benefit of its attractive natural gas marketing arrangements and marketing income equivalent to $0.39 per mcf, Delphi realized an average natural gas price including marketing income of $3.62 per mcf in 2018 compared to an average Chicago City Gate monthly price equivalent to $3.97 per mcf and an average AECO daily price of $1.50 per mcf.

HEDGING

Delphi’s realized prices for condensate and NGL in 2019 are well protected by WTI crude oil swap contracts for an average volume of 2,950 bbl/d at an average price of $85.96 per bbl and Conway propane swap contracts for an average volume of 400 bbl/d at an average price of $44.16 per bbl. The Company’s realized price for natural gas in 2019 is protected by NYMEX HH natural gas swap contracts for an average volume of 17,479 million British thermal units per day (“mmbtu/d”) at an average price of $3.78 per million British thermal units (“mmbtu”) and Chicago – NYMEX natural gas basis swap contracts for an average volume of 19,000 mmbtu/d at an average basis discount of $0.31 per mmbtu, resulting in an average swap price of $3.48 per mmbtu in Chicago.

Hedging contracts in place for 2019 protect the realized price for approximately 85 percent of Chicago natural gas sales and approximately 85 percent of field condensate and NGL sales combined, based on production in the fourth quarter of 2018.

Delphi’s commodity risk management contracts were valued at $26.6 million as at December 31, 2018, providing protection in 2019 and into 2020 against the volatile commodity price environment.

2018 OPERATIONS REVIEW

The 2018 capital program consisted of delineation drilling and completions to further evaluate the potential of West Bigstone, as well as single well development drilling to continue optimizing the fracture treatment design to best unlock the condensate-rich potential at West Bigstone, prior to moving to multi-well pad operations. Production results for the West Bigstone wells drilled and completed during the second half of the 2017 and first half of 2018 were quite variable, but given the fracture treatment design innovations implemented, the 2018 program now contains some of the most prolific condensate-rich wells ever drilled in Bigstone. The first four well pad in West Bigstone has been drilled and completion operations are ongoing. Pad development will mitigate offset well frac impacts and reduce downtime of offset wells, which has often had a significant impact on the Company’s corporate production through the initial development phase of West Bigstone.

| Delineation Wells Completed |

Development Wells Completed |

Total Wells Completed |

Total Wells Drilled Not Completed |

|

| West Bigstone | 3.0 (1.95) | 5.0 (3.25) | 8.0 (5.20) | 3.0 (1.95) |

| South Bigstone | – | 1.0 (0.65) | 1.0 (0.65) | – |

| East Bigstone | – | 3.0 (1.95) | 3.0 (1.95) | – |

Well completions have evolved significantly over the past two years as the Company moved from east to west with its drilling program. At West Bigstone the Company has moved beyond the 30 to 40 fracture stages used to develop East Bigstone, successfully utilizing 65 stage hybrid ball drop / plug and perf frac placement techniques on the last three wells. On the four well pad currently being completed, the Company is increasing the stage count to 80 on two of the wells and is implementing limited entry placement technology with 200 clusters or fracture initiations on the other two wells. These ongoing operations are proceeding according to plan.

| 2018 Bigstone West Wells – Initial Production (IP) Rate Well Performance(1) | |||||||

| Well | IP30 | IP90 | IP180 | ||||

| Number of fracs |

Total Sales (boe/d) |

FCond to Gas Yield ( bbl/mmcf) |

Total Sales (boe/d) |

FCond to Gas Yield ( bbl/mmcf) |

Total Sales (boe/d) |

FCond to Gas Yield ( bbl/mmcf) |

|

| 15-19 | 49 | 1,828 | 228 | 1,300 | 183 | 974 | 168 |

| 16-07(2) | 28 | 607 | 319 | 565 | 208 | 457 | 183 |

| 16-10 | 64 | 1,441 | 317 | 1,234 | 181 | 1,035 | 150 |

| 16-19(2) | 34 | 953 | 245 | 722 | 188 | 569 | 167 |

| 02/16-31 | 49 | 1,095 | 340 | 800 | 304 | ||

| 02/15-19 | 50 | 998 | 245 | 754 | 199 | ||

| 15-10 | 64 | 1,294 | 245 | 1,100 | 153 | ||

| 03/16-31 | 64 | 1,173 | 394 | ||||

- Average production calculated on operating days, excludes non-producing days. Includes estimated NGL gas plant recoveries.

- Liner failure during completion. Not all planned stages were placed.

- All production numbers represent sales volumes.

The table above shows the results of the West Bigstone wells drilled in 2018. Field condensate production rates are correlating closely to the increased number of stages or fracture initiations, while natural gas production rates have been more variable, creating greater variation in total well production rates on a boe per day basis. The increased condensate recoveries at West Bigstone are having a much larger impact to returns on capital invested than the impact of lower and more variable natural gas production rates. Corporate production forecasts will be re-calibrated to this variability in natural gas production rates as more production history is realized. The high operating netbacks being realized from these more condensate rich wells will continue to drive cash flow and reserve value growth.

The 2018 capital program also included several infrastructure projects that reduced operating costs, and increased both production and processing capacity.

The amine processing facility that commenced sweetening Montney gas in May 2018 is part of the Company’s strategy to reduce operating costs and diversify its processing options, which now include the SemCAMS K3 (sour), Repsol Edson (sour), Delphi Bigstone (sweet), and Delphi Negus (sweet) processing facilities. The new amine facility, capable of sweetening up to 17 mmcf/d of gross raw Montney natural gas, has reduced operating costs on that production stream by approximately $0.95 per mcf. Corporately, operating cost savings of approximately $0.85 per boe are being realized due to the amine facility.

In 2018, Delphi also constructed a field battery at 1-3-60-24W5 (“1-3”) to handle production volumes from the 15-10-60-24W5 and 16-10-60-24W5 West Bigstone wells. Given the success of those wells and the offsetting, soon to be completed four-well pad, the facility’s fluid handling capacity is being expanded and will be ready when the four well pad comes on production in the second quarter of 2019. As well, the 1-3 battery is now connected with its own dedicated pipeline to the Company’s 7-11 compression, dehydration and amine facility in East Bigstone to efficiently handle future growth in West Bigstone. In total, the Company installed approximately 16 kilometres of new pipelines to handle the field expansion both to the west and the south.

A 60,000 cubic metre water storage hub is now in operation, enabling efficient West Bigstone pad development and decreased water management costs for completion operations. This has enabled large scale 24 hour fracturing operations on the existing four well pad and all future multi-well pads, while also providing security of water. In combination with the previously announced fluid disposal agreement with Catapult Environmental Inc., full cycle water management costs and logistics will be reduced and simplified going forward.

On behalf of the Board of Directors and all the employees of Delphi, we would like to thank our shareholders for their continued support.

CONFERENCE CALL AND WEBCAST

A conference call and webcast to review 2018 year end results is scheduled for 9:00 a.m. Mountain Time (11:00 a.m. Eastern Time) on Thursday, March 14, 2019. The conference call number is 1-844-358-8760. A brief presentation by David J. Reid, President and CEO, Mark Behrman, CFO, and Rod Hume, SVP Engineering will be followed by a question and answer period. The conference call will also be broadcast live on the Internet and may be accessed through www.delphienergy.ca or by entering https://edge.media-server.com/m6/p/nmxrqdie in your web browser.

A recorded rebroadcast will be archived and made available on the Company’s website at www.delphienergy.ca or by entering https://edge.media-server.com/m6/p/nmxrqdie in your web browser. Delphi’s annual and fourth quarter 2018 financial statements and management’s discussion and analysis are available on the Company’s website at www.delphienergy.ca and SEDAR at www.SEDAR.com.

About Delphi Energy Corp.

Delphi Energy Corp. is an industry-leading producer of liquids-rich natural gas. The Company has achieved top decile results through the development of our high quality Montney property, uniquely positioned in the Deep Basin of Bigstone, in northwest Alberta. Delphi continues to outperform key industry players by improving operational efficiencies and growing our dominant Bigstone land position in this world-class play. Delphi is headquartered in Calgary, Alberta and trades on the Toronto Stock Exchange under the symbol DEE.

FOR FURTHER INFORMATION PLEASE CONTACT:

DELPHI ENERGY CORP.

2300 – 333 – 7th Avenue S.W.

Calgary, Alberta

T2P 2Z1

Telephone: (403) 265-6171 Facsimile: (403) 265-6207

Email: [email protected] Website: www.delphienergy.ca

DAVID J. REID MARK D. BEHRMAN

President & CEO CFO

Forward-Looking Statements. This news release contains forward-looking statements and forward-looking information within the meaning of applicable Canadian securities laws. These statements relate to future events or the Company’s future performance and are based upon the Company’s internal assumptions and expectations. All statements other than statements of present or historical fact are forward-looking statements. Forward-looking statements are often, but not always, identified by the use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “should”, “believe”, “intends”, “forecast”, “plans”, “guidance”, “budget” and similar expressions.

More particularly and without limitation, this release contains forward-looking statements and information relating to petroleum and natural gas production estimates and weighting, projected crude oil and natural gas prices, future exchange rates, expectations as to royalty rates, expectations as to transportation and operating costs, expectations as to general and administrative costs and interest expense, expectations as to capital expenditures and net debt, planned capital spending, future liquidity and Delphi’s ability to fund ongoing capital requirements through operating cash flows and its credit facilities, supply and demand fundamentals for oil and gas commodities, timing and success of development and exploitation activities, cash availability for the financing of capital expenditures, access to third-party infrastructure, treatment under governmental regulatory regimes and tax laws and future environmental regulations.

Furthermore, statements relating to “reserves” are deemed to be forward-looking statements as they involve the implied assessment, based on certain estimates and assumptions that the reserves described can be profitable in the future.

The forward-looking statements and information contained in this release are based on certain key expectations and assumptions made by Delphi. The following are certain material assumptions on which the forward-looking statements and information contained in this release are based: the stability of the global and national economic environment, the stability of and commercial acceptability of tax, royalty and regulatory regimes applicable to Delphi, exploitation and development activities being consistent with management’s expectations, production levels of Delphi being consistent with management’s expectations, the absence of significant project delays, the stability of oil and gas prices, the absence of significant fluctuations in foreign exchange rates and interest rates, the stability of costs of oil and gas development and production in Western Canada, including operating costs, the timing and size of development plans and capital expenditures, availability of third party infrastructure for transportation, processing or marketing of oil and natural gas volumes, prices and availability of oilfield services and equipment being consistent with management’s expectations, the availability of, and competition for, among other things, pipeline capacity, skilled personnel and drilling and related services and equipment, results of development and exploitation activities that are consistent with management’s expectations, weather affecting Delphi’s ability to develop and produce as expected, contracted parties providing goods and services on the agreed timeframes, Delphi’s ability to manage environmental risks and hazards and the cost of complying with environmental regulations, the accuracy of operating cost estimates, the accurate estimation of oil and gas reserves, future exploitation, development and production results and Delphi’s ability to market oil and natural gas successfully to current and new customers. Additionally, estimates as to expected average annual production rates assume that no unexpected outages occur in the infrastructure that the Company relies on to produce its wells, that existing wells continue to meet production expectations and any future wells scheduled to come on in the coming year meet timing and production expectations.

Commodity prices used in the determination of forecast revenues are based upon general economic conditions, commodity supply and demand forecasts and publicly available price forecasts. The Company continually monitors its forecast assumptions to ensure the stakeholders are informed of material variances from previously communicated expectations.

Financial outlook information contained in this release about prospective results of operations, financial position or cash flows is based on assumptions about future events, including economic conditions and proposed courses of action, based on management’s assessment of the relevant information currently available. Readers are cautioned that such financial outlook information contained in this release should not be used for purposes other than for which it is disclosed.

Although the Company believes that the expectations reflected in such forward-looking statements and information are reasonable, it can give no assurance that such expectations will prove to be correct and such forward-looking statements should not be unduly relied upon. Since forward-looking statements and information address future events and conditions, by their very nature they involve inherent known and unknown risks and uncertainties. Delphi’s actual results, performance or achievements could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits Delphi will derive therefrom. Should one or more of these risks or uncertainties materialize, or should assumptions underlying forward-looking statements prove incorrect, actual results may vary materially from those currently anticipated due to a number of factors and risks. These include, but are not limited to, the risks associated with the oil and gas industry in general such as operational risks in development, exploration and production, delays or changes in plans with respect to exploration or development projects or capital expenditures, the uncertainty of estimates and projections relating to production rates, costs and expenses, commodity price and exchange rate fluctuations, marketing and transportation, environmental risks, competition from others for scarce resources, the ability to access sufficient capital from internal and external sources, changes in governmental regulation of the oil and gas industry and changes in tax, royalty and environmental legislation. Additional information on these and other factors that could affect the Company’s operations or financial results are included in the Company’s most recent Annual Information Form and other reports on file with the applicable securities regulatory authorities and may be accessed through the SEDAR website (www.sedar.com).

Readers are cautioned that the foregoing list of factors is not exhaustive. Furthermore, the forward-looking statements contained in this release are made as of the date of this release for the purpose of providing the readers with the Company’s expectations for the coming year. The forward-looking statements and information may not be appropriate for other purposes. Delphi undertakes no obligation to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws. The forward-looking statements contained in this release are expressly qualified in their entirety by this cautionary statement.

Basis of Presentation. For the purpose of reporting production information, reserves and calculating unit prices and costs, natural gas volumes have been converted to a barrel of oil equivalent (boe) using six thousand cubic feet equal to one barrel. A boe conversion ratio of 6:1 is based upon an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. This conversion conforms to the Canadian Securities Administrators’ National Instrument 51-101 when boes are disclosed. Boes may be misleading, particularly if used in isolation.

As per CSA Staff Notice 51-327 initial test results and initial production performance should be considered preliminary data and such data is not necessarily indicative of long-term performance or of ultimate recovery. “IP” is an abbreviation for “Initial Production” and represents average production rates over the indicated time period in producing days.

Non-GAAP Measures. The release contains the terms “cash flow from operating activities per share”, “adjusted funds flow”, “adjusted funds flow per share”, “net debt”, “net debt to adjusted funds flow ratio”, “marketing income”, “operating netbacks”, “cash netbacks,” and “netbacks” which are not recognized measures under GAAP. The Company uses these measures to help evaluate its performance. Management considers netbacks an important measure as it demonstrates its profitability relative to current commodity prices and costs of production. Management uses adjusted funds flow to analyze performance and considers it a key measure as it demonstrates the Company’s ability to generate the cash necessary to fund future capital investments, abandonment obligations and to repay debt. Adjusted funds flow is a non-GAAP measure and has been defined by the Company as cash flow from operating activities before decommissioning expenditures and changes in non-cash working capital from operating activities. The Company also presents cash flow from operating activities per share and adjusted funds flow per share whereby amounts per share are calculated using weighted average shares outstanding consistent with the calculation of earnings per share. Delphi’s determination of adjusted funds flow may not be comparable to that reported by other companies nor should it be viewed as an alternative to cash flow from operating activities, net earnings or other measures of financial performance calculated in accordance with GAAP. The Company has defined net debt as the sum of bank debt, senior secured notes and the long term portion of unutilized take-or-pay contract plus/minus working capital deficit/surplus excluding the current portion of the fair value of financial instruments. Net debt is used by management to monitor remaining availability under its credit facilities. Marketing income is defined as the margin earned on the sale of purchased third party natural gas volumes and premiums received on the assignment of a portion of committed capacity on the Alliance pipeline system to a third party. Management considers marketing income important measures of the Company’s ability to mitigate the cost of excess committed capacity. Operating netbacks have been defined as revenue plus marketing income less royalties, transportation and operating costs. Cash netbacks have been defined as operating netbacks less interest on bank debt and senior secured notes, general and administrative costs and cash costs related to the Company’s restricted share units. Netbacks are generally discussed and presented on a per boe basis.

Share This: