CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Charles St‑Arnaud, Chief Economist, Servus Credit Union

Key takeaways:

- More than 20% of Alberta’s fiscal revenues come from non-renewable resource royalties. While this seems high, it is still lower than the 2000 to 2008 period, when it averaged around a third of fiscal revenues.

- Hence, the lower oil prices compared to the assumptions used in Budget 2025 will have some consequences. We estimate Alberta’s fiscal deficit will reach C$6.4bn in FY2025-26, roughly unchanged from the mid-year fiscal update but $1.2bn higher than in Budget 2025.

- While this deterioration appears relatively small, it masks a significant countercurrent. As such, the weaker WTI oil prices alone would have led to a $3.6 bn wider deficit. However, thanks to the opening of the expanded TMX pipeline, the spread between the WCS and the WTI has narrowed substantially (see Year one of TMX: Increased export diversification, disappearing oil discount, and C$13bn in extra revenues for more).

- With a wider deficit in FY2025-26 as a starting point, we estimate that the deficit for FY2026-27 is likely to widen further, just shy of $10bn, at $9.8bn, if we assume an oil price of US$60 a barrel for WTI, roughly in line with current market expectations.

- However, this estimate is highly sensitive to the assumption regarding the price of oil over the course of the fiscal year. Nevertheless, unless oil prices break above US$75, it is virtually impossible to balance the budget without significant spending cuts.

- With the oil differential roughly at its fair value, i.e. Canadian oil is no longer sold at a discount, any further narrowing of the WCS-WTI spread is very unlikely. Hence, the oil price differential is unlikely to reduce the deficit in FY2026-25 and act as a buffer against lower oil prices as it did in FY2025-26.

In Alberta, variations in energy prices can make or break the provincial Budget. As such, a decline in energy prices reduces revenues and worsens the fiscal balance, while an increase in energy prices raises revenues and improves the fiscal balance.

Last fall, ahead of Alberta’s mid-year fiscal update, we examined the impact that lower oil prices relative to Budget 2025 assumptions would have on the province’s fiscal situation.

In this report, we update our estimates for the expected deficit for FY2025-26 and FY2026-27. In addition, the Appendix provides background on the rising sensitivity of fiscal revenues to changes in oil prices and an analysis of the level of oil prices required to balance the budget.

FY2025-26 deficit is likely little changed from the mid-year update

Budget 2025 assumed that WTI oil prices would average $68 in FY2025-26, the WCS-WTI spread would be $17.10, and the exchange rate would be US$0.696 per C$. Based on these assumptions and the economic outlook presented in the Budget, the Government of Alberta expected a deficit of $5.3bn for FY2025-26.

However, so far for FY2025-26, the WTI oil price has been lower at $62.85. This decline in oil prices has resulted from expected slower global growth due to the impact of US tariffs on the global economy and from an increase in global oil supply as OPEC gradually normalizes oil production after a period of curtailment.

While recent geopolitical uncertainty stemming from the situations in Venezuela and Iran has pushed oil prices higher in recent months, the increase has come too late in FY2025-26 to make a significant difference. Nevertheless, the current situation will provide a better starting point for FY2026-27, if prices remain at current levels.

As we have shown (see Year one of TMX: Increased export diversification, disappearing oil discount, and C$13bn in extra revenues), thanks to the opening of the expanded TMX pipeline, the spread between the WCS and the WTI has narrowed substantially, averaging $11.45 so far this fiscal year. This is significantly narrower than in previous years, when it averaged almost $20 in 2022 and 2023. We estimate that the narrower spread over the first year of operation of the TMX pipeline has boosted oil revenues by $26bn since entering operations, with a significant impact on Alberta’s fiscal situation.

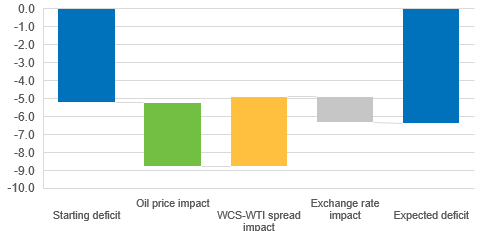

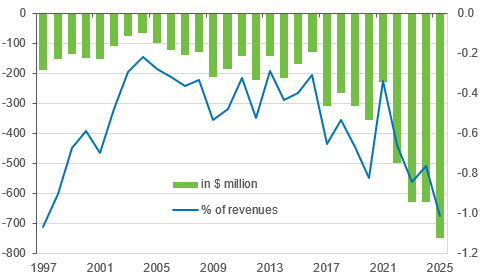

Fig 1. Estimated changes in Alberta’s fiscal balance for FY2025-26 (C$ bn)

Note: Using elasticities from Alberta’s Budget 2025-26 and using the Bloomberg forecast for WTI and the Canadian dollar. Source: Treasury Board and Finance, Bloomberg, Servus Credit Union

Using the elasticities from the Budget, if we assume oil prices, the price differential and the exchange rate remain at their current levels for the remainder of the fiscal year, we estimate that lower oil prices lead to a $3.6bn deterioration in the deficit, and a stronger Canadian dollar to a worsening of $1.5bn. However, the narrower WCS-WTI spread would improve the fiscal balance by $3.9bn, more than fully offsetting the impact from lower WTI prices. Overall, under these assumptions, the deficit for FY2025-26 would be about $1.2bn wider than in the Budget at $6.4bn, roughly unchanged from the mid-year update.

It is very important to highlight that, without the narrowing in the oil price difference as a result of the opening of the expanded TMX pipeline, the fiscal deficit would have been $10.5bn, double the estimate in the Budget 2025, and would have been the biggest fiscal deficit in Alberta’s history, if we exclude the pandemic period.

More fiscal deterioration expected for FY2026-27

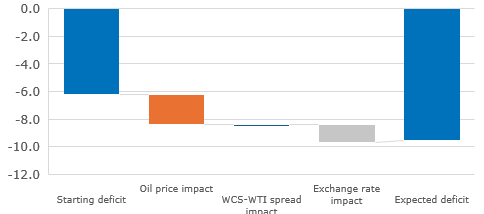

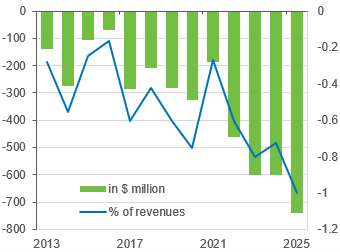

Looking at FY2026-27, we assume a starting budget deficit of $6.4bn, as estimated above. For 2026, the current median forecast for WTI oil prices from the private sector on Bloomberg is $58.70 on average for FY2026-27, but let’s assume it averages $60 over the fiscal year; the current forecast for the exchange rate is 0.737, and the oil differential is assumed to average $12 over the period. Using these assumptions, we estimate that the deficit could widen by about $2.9bn in FY2026-27 to $9.8bn.

Fig 2. Estimated changes in Alberta’s fiscal balance for FY2026-27 (C$ bn)

Note: Using elasticities from Alberta’s Budget 2025-26, $60 for WTI and 0.737 for the exchange rate. Source: Treasury Board and Finance, Bloomberg, Servus Credit Union

The estimated deficit is highly sensitive to assumptions.

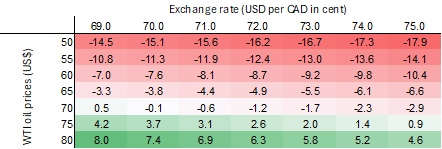

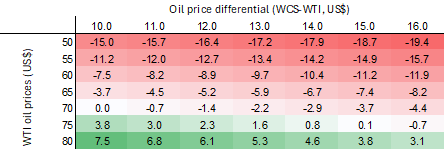

The Table below also shows estimates of the fiscal deficit for FY2026-27 under various combinations of WTI oil prices and exchange rates. A second table shows the deficit under various combinations of WTI oil prices and WCS-WTI differential. What is clear from both sets of simulations is that it is almost impossible to balance the budget for FY2026-27, unless WTI oil prices rise to at least $75. This shouldn’t be a surprise since, as shown in the Appendix, it is the level of WTI oil prices required to balance Alberta’s budget. While a breakeven level of $75 seems elevated, given that oil prices have averaged $63.80 over the past decade, it is significantly lower than the $90 required to balance the budget before 2019.

Fig 3. FY2026-27 deficit based on WTI oil prices and the exchange rate

Note: Using elasticities from Alberta’s Budget 2025-26. Source: Treasury Board and Finance, Bloomberg, Servus Credit Union

Fig 4. FY2026-27 deficit estimates based on WTI oil prices and oil price differential

Note: Using elasticities from Alberta’s Budget 2025-26. Source: Treasury Board and Finance, Bloomberg, Servus Credit Union

An important point is that the oil differential is roughly at its fair value, i.e. as Canadian oil is no longer sold at a discount, any further narrowing of the WCS-WTI spread is very unlikely. This means the distribution of potential outcomes is tilted toward a widening of the oil spread rather than a narrowing. Hence, the WCS-WTI differential is unlikely to meaningfully reduce the deficit in FY2026-27 or act as a buffer against lower oil prices, as it did in FY2025-26.

Another important factor to consider is that the fiscal balance and revenue sensitivities to changes in oil prices, in oil price differential, and the exchange rate will increase in the coming years, as Alberta’s oil production volume continues to grow and more projects reach “post-payout status” and start paying higher royalty rates. As a result, changes in oil prices are likely to have a larger impact on Alberta’s fiscal position in the coming years than was estimated for FY2025-26. Hence, our estimate of the impact of lower oil prices in FY2026-27 could prove to be underestimated.

Conclusion

The deficit for FY2025-26 is expected to exceed the budget forecast, C$6.4bn, due to lower oil prices and a stronger Canadian dollar over the fiscal year. However, if it were not for the narrower oil price differential over the period, thanks to the TMX pipeline expansion, the deficit would have been closer to C$10bn, almost twice the budget estimate.

Oil prices are expected to remain weak over the course of FY2026-27, despite recent gains, amid heightened geopolitical uncertainty, as market fundamentals continue to point to global oil oversupply. In addition, the Canadian dollar is expected to appreciate slightly over the fiscal year. With the oil price differential unlikely to narrow further, this will lead to an increase in the fiscal deficit for FY2026-27 of C$9.7bn.

The size of the deficit will depend on the assumptions the government uses to estimate revenues. However, as shown, unless the government uses extremely optimistic assumptions or dramatically cuts spending, it will be very difficult for the deficit to be smaller in FY2026-27.

Appendix A

Volatile oil prices lead to a volatile fiscal situation, but it is not the whole story

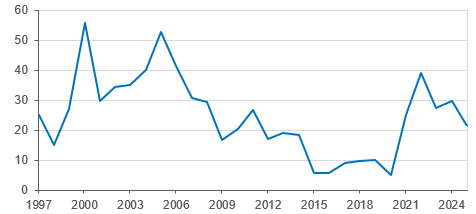

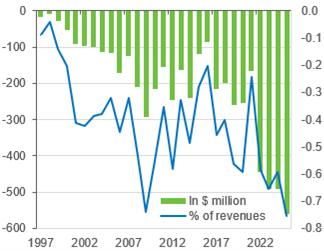

The links between oil prices and Alberta’s fiscal situation are obvious, with the value of oil produced in the province a significant source of revenue for the province’s economy. The most direct impact is that higher oil revenues increase royalty revenues from non-renewable resources, i.e. a tax on the value of oil extracted in the province, which currently accounts for about 21.5% of the Government of Alberta’s revenues. While more than 20% of fiscal revenues being derived directly from oil and gas extraction may seem high, this proportion was approximately one-third of revenues on average between 2000 and 2008.

Fig 5. Non-renewable resources royalties as % of spending

Source: Treasury Board and Finance, Servus Credit Union

Higher oil revenues, primarily when driven by higher prices, also lead to higher government revenues, as they translate into higher industry profits and higher corporate tax payments. Similarly, the higher oil revenues and improved profitability in the industry will boost personal income, via wages, salaries, and other compensation like bonuses, leading to an increase in personal tax payments. Hence, changes in energy prices not only affect non-renewable resource royalties but also broader tax revenues, thereby impacting fiscal revenues.

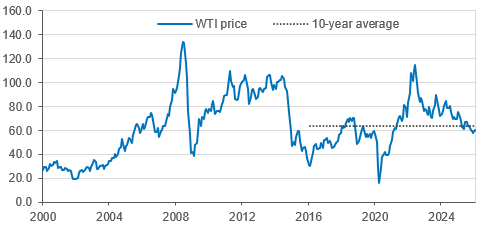

Fig 6. WTI oil prices (US$)

Source: World Bank, Servus Credit Union

The main issue for the province’s fiscal position is that oil revenues are highly volatile, which in turn leads to similarly volatile fiscal revenues. Oil production volumes have been steadily increasing since 2008, with only modest volatility, from about 100 million cubic meters to about 153 million cubic meters in 2023. The volatility in oil revenues stems from price changes: WTI hovered between $80 and $100 from 2010 to mid-2014, before falling mainly below $60 a barrel from late-2014 to 2021. The price spiked to about $120 in 2022 following Russia’s invasion of Ukraine, but moderated to around $80 by late 2022, remaining there until it started moderating in mid-2014. WTI oil prices have averaged almost $62.5 a barrel so far in 2025, but have been closer to $65 in recent weeks.

Looking at the relationship between oil prices and Alberta’s fiscal revenues and balance, we find a powerful link. As such, we estimate that the correlation between changes in WTI and fiscal revenues was 0.88 over the past 10 years, while the correlation between changes in WTI and the fiscal balance was 0.96. Hence, the volatility in oil prices explains the volatility in Alberta’s fiscal situation.

The Government of Alberta is very transparent about the impact of changes in oil prices on its fiscal situation. As such, the Budget assumes that a $1 decline in oil prices results in a net $750 million decline in its fiscal balance. This is equivalent to a 1.0% decline in revenues for each $1 reduction in oil prices.

Other factors affecting the value of the oil produced also significantly affect the fiscal balance. As such, a $1 narrowing of the differential between the prices of heavy oil (Western Canadian Select – WCS) and light oil (WTI) is estimated to improve the fiscal balance by $740 million. This is equivalent to a 1.0% increase in revenues.

These elasticities have been increasing over the years as oil production volume has increased. As such, back in 2010, a $1 decline in oil prices led to a $130 million deterioration in the fiscal balance, equivalent to a 0.4% decline in revenues. For the oil price differential, back in 2015, a reduction in the spread would have raised revenues by $105 million, or a 0.2% increase.

Fig 7. Net impact of a $1 decline in WTI

Source: Treasury Board and Finance, Servus Credit Union

In addition, because oil revenues are in US dollars but the Government of Alberta collects revenues in Canadian dollars, the exchange rate also affects fiscal revenues. As such, over the past 10 years, the correlations between changes in the value of the Canadian dollar and changes in fiscal revenues are 0.73 and 0.67 with changes in the fiscal balance. The Government of Alberta estimates that a 1-cent appreciation of the Canadian dollar relative to the US dollar results in a $560 million deterioration in the fiscal balance. Like the sensitivity to oil prices changes, this elasticity has also been increasing with the rising value of oil exports, from about $85 million per dollar change back in 2015.

It is interesting to note that there is no relationship between the sensitivity of the fiscal situation to oil prices and the share of fiscal revenues derived from royalties. Hence, having a greater share of fiscal revenues tied to oil production does not make these revenues more sensitive to oil price changes.

Fig 8. Net impact of a $1 widening in the WCS-WTI spread

Source: Treasury Board and Finance, Servus Credit Union

Fig 9. Net impact of a 1¢ Canadian dollar appreciation

Source: Treasury Board and Finance, Servus Credit Union

Appendix B

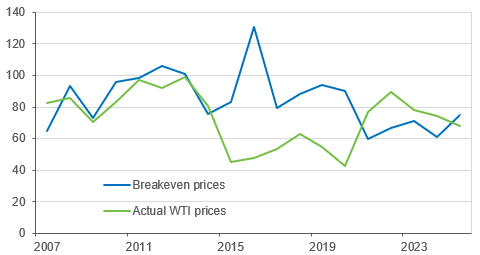

What oil prices are needed to balance the Budget?

Even before oil prices began to decline in 2025, the Government of Alberta estimated a $5.3bn deficit for FY2025-26. The Budget assumed that oil prices would average $68 during FY2025-26. While this assumption looks optimistic now, at the time of the Budget release in February, it was in line with the private-sector average forecast. Nevertheless, it raises a question: What price of oil would have been required to balance the fiscal position in FY2025-26? This question can be answered using the elasticities provided in the Budget.

If we do not consider the impact of changes in the oil price differential and exchange rate fluctuations, we estimate that WTI oil prices would have needed to be $75 to balance the Budget.

To put it in perspective, oil prices averaged $77.6 in 2023 and $75.6 in 2024, suggesting that the budget would have been balanced if oil prices had not eased since September 2024. However, taking a long-term perspective, oil prices have averaged closer to $63.4 over the past 10 years; they have been rarely above $80 during that period, except in 2022 following the Russian invasion of Ukraine.

On the flip side, the narrowing of the oil spread thanks to the TMX pipeline has lowered this breakeven price. Assuming an oil differential of $12, we estimate that the price of oil required to balance the Budget would be about $70. Yet, this is still above the average oil price of the past 10 years.

Adding the impact of a strong Canadian dollar since the start of the fiscal year, the oil prices required to balance the fiscal book are $71.9. It can be argued that the Canadian dollar is weak at the moment. Hence, if we assume that it reverts to its 10-year average of $0.755 US dollar per Canadian dollar, the breakeven price rises to $74.4.

These estimates provide an alternative way to assess the volatility of the budget balance to changes in oil prices. Using the same reverse engineering with the fiscal balance and oil-price sensitivities for each year, we can estimate the oil prices required to balance the Budget over the past 20 years.

The results show that the breakeven oil prices averaged $90 between 2005 and 2020. Since 2021, it has averaged $67. The decline in breakeven oil prices since 2021 is due to changes in royalty rates, as many projects reached post-payout status (total project revenue exceeds total capital and operating costs. However, this increase in oil royalties increases the sensitivity to fluctuations in oil prices.

Fig 10. Estimated breakeven oil prices

Note: WTI oil prices are required to balance the fiscal position. Source: Treasury Board and Finance, Bloomberg, Servus Credit Union

Share This: