CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

October 4, 2021

Imagine if Greta Thunberg and Alexandria Ocasio-Cortez became the thought leaders for the future of global energy.

Oh dear. They did.

But only the western world’s media and politicians were listening.

As fossil fuel prices skyrocket and shortages loom, we are again reminded that market forces rule. It is the world’s 7.9 billion consumers who drive the global energy bus.

Following the unprecedented collapse of oil prices and demand in the spring of 2020, aspirational speculation about oil’s ideal future exploded.

Oil was dead. Never coming back. Sunset industry. Stranded assets. Dump your fossil fuel investments before they become worthless.

Last September BP surprised everyone by announcing it was exiting its legacy business. This was accompanied by a forecast that “net zero by 2050” would require oil demand to fall by 75% in thirty years.

Because net zero by 2050 was no longer a dream. Everybody was saying it. Even oil producers that knew it was technically impossible without crushing the world economy adopted the slogan.

Life was simpler that way.

Decarbonization advocates invented more slogans like Build Back Better, Green New Deal, Resilient Recovery, Great Reset and Just Transition.

Switching from fossil fuels to renewables would power the post-pandemic economic recovery. Enlightened public policy funded by more public debt and government financial support would be the catalyst. A job-rich economic boom was assured.

It didn’t happen. And it never will.

Too much pandemic chaos and not enough time, money, public support or political will.

As the economy recovered, so did demand for oil. But supply is a looming problem.

Today’s energy news is about significant shortages of coal and natural gas for electricity in Europe and Asia. On September 30 Bloomberg carried the headline, “China Orders Top Energy Firms to Secure Supplies at All Costs.” The global supply chain for the myriad of things made from fossil fuels and cheap energy could also be at risk.

This should not be surprising. Energy forecasts have moved from data-based to aspiration-based. It’s a new era where inputs are chosen to achieve the desired outcome. Forecasts now include low cost, low carbon energy technologies that don’t exist. Or assume that intermittent energy sources will be stable and predictable.

Historic energy forecasts were based on established inputs such as population, income, reliable and ample energy sources, and the absence of suitable alternatives. Suitable is defined as doing the same thing at the same price.

More people with more money meant more petroleum consumption. It’s been that way for a century.

That all changed with the climate emergency. Fossil fuels were doomed because so many declared they should be. The public bought the story because they had been told repeatedly that it can and must be done.

Those who raised doubts were ignored or labelled “deniers.” Experts reported that the energy transition as advertised was impossible. They calculated how many solar panels, wind farms, nuclear reactors, storage batteries and trillions of dollars would be required. There wasn’t enough of anything from land to minerals to money to make it happen.

Nobody listened. Severe weather, burning forests and houses, and the impending climate catastrophe dominated the media. Facts and physics were boring.

But replacing oil is so much easier to say than do. As the world was told what to think, say and do, nobody bothered to ask 7.9 billion people what they wanted or needed.

That was an enormous mistake.

**********

In 1990 I had the opportunity to meet Secretary General of OPEC Dr. Subroto while he was in Alberta. I asked him, “What will happen to oil prices?”

He replied with this take-it-to-the-bank answer. “The only thing certain about oil is uncertainty.”

Oil’s volatility was obvious by then. Corrected for inflation in the past twenty years it had gone from $US23.90 (1970) to $US124.39 (1980) to $US48.21 (1990). A huge boom followed by a massive bust. WTI averaged only $US30.35 (inflation corrected) for the next ten years.

High oil prices in the 1970s had brought significant new production on stream from all over the world like the North Slope, North Sea and Alberta’s oil sands. It took years of low prices and population growth for all the new supplies to be absorbed.

Starting in 2000, the supply/demand curves crossed again. By 2008 the average price for the year was US$99.67. It peaked at a record US$145.31 on July 3. After a big but brief slump caused by the world financial crisis in 2008/2009, it averaged US$95.02 from 2011 to 2014.

Higher prices worked their magic again. New supplies from American light/tight shale oil and Alberta’s oil sands created another surplus. After OPEC abandoned supply management in late 2014, for the next five years WTI averaged only US$53.

Dr. Subroto was both right and wrong.

The “uncertainty” Subroto cited was the impact of unpredictable geopolitical factors, so-called “black swan” events. These included the original OPEC oil embargo of 1973, the Iran/Iraq War from 1980 to 1988, and the world financial crisis of late 2008 which caused crude to fall US$110 a barrel from July to December.

The global pandemic lockdown of early 2020 was the mother of all black swans. Oil collapsed. Everything that could stop did to counteract oil prices that averaged only US$16.55 in April.

Where Dr. Subroto was wrong was that the fundamentals of oil supply and demand and the subsequent impact on price have not changed in 50 years.

When demand exceeds supply, prices rise. The difference between 2020 and 2021 from the previous 100 years was agenda-driven prognosticators somehow believing that the climate interventionist forces driving global energy policies were as powerful as the market fundamentals of production, consumption and consumer choice.

**********

November will mark seven years since the fateful OPEC meeting that collapsed oil in late 2014. That’s a long time. Oil prices have stayed low and affordable. Supply was never in question thanks to excess capacity among OPEC+ producers and, until 2020, the relentless growth in US production.

Politicians, environmentalists and investors could interfere with new supplies from sources like Alberta’s oil sands without affecting consumers. Who needed more oil?

Since early 2015 there has been a multi-faceted assault on global oil supply. It was a combination of market forces and the new influences of climate and political activism.

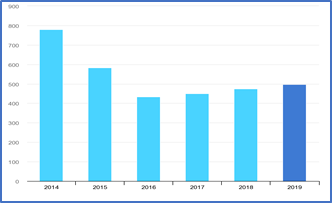

The predictable market response was the decline in capital expenditures. High oil prices had supported a multi-year growth in investment which peaked in 2014. The following chart from the International Energy Agency shows “Global oil and gas upstream expenditures 2014 – 2019”.

The left axis is in hundreds of billions of US dollars. Spending fell from US$790 billion in 2014 – the highest in history – to about half that amount in 2016. By 2019 spending had only recovered to about 60% of 2014 levels. Because of the pandemic, for 2020 the IEA reports this figure fell again to $350 billion, the lowest in recent history and under half of 2014 levels.

The oil price collapse coincided with a sharp rise in anti-oil activism on multiple fronts. A major catalyst was the UN COP 21 climate conference in Paris in 2015. Although multiple UN meetings since 1992 had pledged and failed to reduce fossil fuel emissions, Paris was different. The participation and pledge of US President Barack Obama added a new level of commitment and credibility.

Following Paris, climate activism migrated into capital markets. A milestone in 2017 was the creation of the Task Force on Climate-Related Financial Disclosures by business news tycoon Michael Bloomberg and Governor of the Bank of England Mark Carney.

Risk always gets the attention of capital markets. It is irresponsible to ignore it. Because if the Paris commitments were achieved, the future for fossil fuels was certainly in question. As more financial institutions got on board, this evolved into today’s ESG investing phenomenon.

It was an easy time for major financial institutions to embrace climate activism and the energy transition. Because of collapsed prices, oil and gas investments were hardly attractive. Massive wealth destruction occurred. Under continuous political and public pressure, European banks began to proudly announce they would no longer fund coal or oil sands developments. Opposing fossil fuels became a badge of honor. Politicians, religious leaders, fund managers and eventually business leaders joined the cause.

Significant new pools of capital emerged to focus on renewable electricity and other clean energy sources. They were supported by governments through direct subsidies, favorable legislation, fixed returns, and preferential grid access. They didn’t generate much if any free cash, but neither did oil and gas.

With politicians driving the policy bus and central banks pursuing continued quantitative easing through rising public debt and low interest rates, investors gained confidence that moving their capital from fossil fuels to renewables was not only good for the planet but financially rewarding.

You could simultaneously make money and save the world. Capitalism and altruism became synonymous. Corporate social responsibility began to rival generating profits for shareholders.

Historically low interest rates, growing government spending, cheap energy, relentless media coverage, and what appeared to be a sustainable expanding economy left the public with the illusion that the climate-saving energy transition was happening quickly and painlessly.

Sleep well and move your savings and retirement funds into the capable hands of ESG fund managers.

Because the consumers of the world wouldn’t voluntarily reduce fossil fuel consumption for their own good, this plan would restrict supply. It was a moral imperative. Pipeline obstruction and carbon taxes were not a problem. They were essential!

Another black swan, but this one flew well below the radar.

But not enough attention was paid to demand driven by population growth, rising incomes, and the reality of how difficult it is to replace fossil fuels.

This graph from the 2021 BP Statistical Review of World Energy charts just how little the “energy transition” has moved the needle in the past 15 years despite growing public pressure the investment of trillions of dollars.

Globally, growth in clean energy was steady before markets collapsed in 2020. But so was demand for oil, gas and coal.

Why have renewables not gained more traction? Because given the choice, they are not commercially attractive replacements in terms of availability, practicality and reliability. An electric vehicle is a great idea. Except that to participate you have to buy a new car and refueling is not easy.

And whatever they could or should do, renewables are still not suitable for heavy transportation, petrochemicals, 24/7/365 electricity generation, or a myriad of other applications.

Consumers buy the lowest cost and most easily accessible products. This is fundamental economics. And in the absence of market-distorting subsidies, regulation or restricted supply, this behavior will never change.

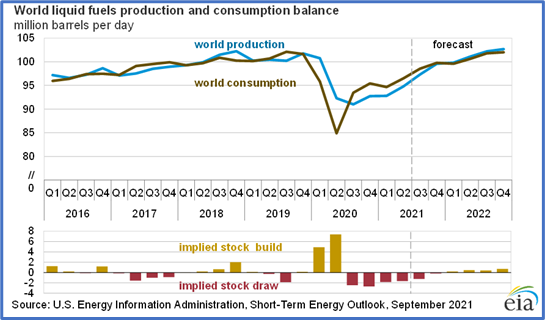

As the economy began to reawaken in the last half of 2020, oil demand grew with it. This chart from America’s Energy Information Administration shows how quickly oil demand bounced back once people were permitted to resume normal lives.

Because nobody read the memo on what energy they were supposed to buy, or that staying trapped at home was really good for the global atmosphere.

The information that matters is the spread between production (blue) and consumption (brown) and the implied stock (inventory) changes in the bar charts below. The pandemic caused a big build in inventories in the first half of 2020, but they have been drawn down steadily since. The EIA sees markets in balance last this year and all of 2022.

ESG investing only affects the behavior of publicly traded OECD-headquartered companies. Only 16% of the world’s 7.9 billion people live in OECD countries. The other 84% live in developing economies. This is where all the demand growth is taking place. And where oil production growth will continue.

The most astonishing aspect of the very public climate emergency/energy transition/ESG investment phenomenon is how seldom it acknowledges that these 6.6 billion people exist, and how greatly their needs and aspirations differ from those in the wealthy west.

**********

OPEC has no intention of cutting output nor does it project any drop in oil demand thanks to a growing population and disposal income in the non-OECD world. As the west tries to force its oil producers to change their behavior, OPEC sees its market share growing.

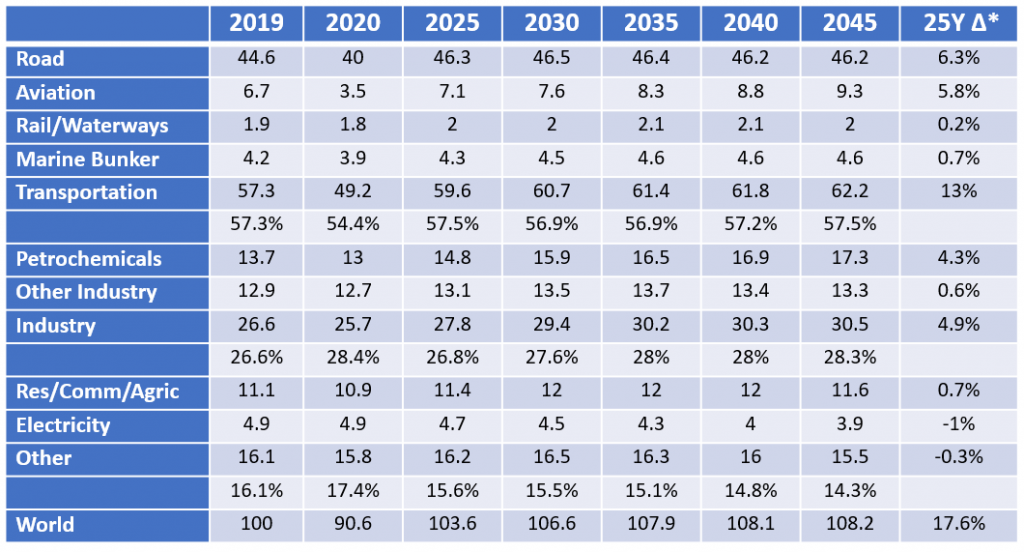

OPEC released its 2021 World Oil Outlook 2045 on September 30. OPEC member countries speak to and for the world’s oil consumers, not European and North American voters.

The result is an entirely different future for oil. The spread between OPEC’s forecast oil demand in 2045 and BP’s Net Zero by 2050 scenario is over 50 million b/d.

Somebody is very wrong.

Source: 2021 OPEC World Oil Outlook – *Change from 2020 to 2045

The two foundational drivers for OPEC’s 2045 forecast are that the population of the world will increase by 1.7 billion to 9.5 billion, and 96% of that will take place in non-OECD countries.

OPEC’s market growth will occur in countries where nobody cares about the latest utterances of Greta, AOC, Carney, Bloomberg, Biden or Trudeau.

If the ESG acronym was used it would stand for Energy, Safety and Groceries.

A Wall Street Journal article October 1 was titled, “OPEC Boss Says World Can’t Afford to Underinvest in Oil”. It opens, “…consumers should brace for more energy shortages unless the world boosts investment in new oil-and-gas development…”

OPEC head Mohammed Barkindo said, “The energy crisis in Europe and many parts of the world is a wake-up call. It all comes back to the issue of investment across the oil-and-gas industry.”

The drop in investment in new supplies is clear. Barkindo said, “We need to buckle up more investment in capital to revive the production cycle.” The article continues, “…’On top of that (investment) contraction, you have the energy transition,’ he said, which has added more pressure on governments and oil companies to divert money for oil-and-gas development to renewables. Mr. Barkindo said there has been ‘a global campaign (against) the oil industry to crowd investors out of oil and gas’.”

The current outlook for energy prices is grim going into winter. China is short of coal and is actively seeking secure supplies which is driving up prices. Spot LNG prices in Asia have reached US$34/GJ, the equivalent of US$200 a barrel oil. Electricity price spikes in Europe caused in part by a heavy dependence on interruptible renewables and tight natural gas supplies are shutting down industries and clobbering consumers.

Meanwhile, the ability of governments to borrow even more money to support the economy is reduced because of the pandemic. Inflation is hurting global consumers as it hits essentials like food. Higher taxes are inevitable to service exploding public debt.

Regardless, energy transition proponents keep urging governments to spend even more to replace fossil fuels. In Canada continuously higher carbon taxes are proudly promised by the Trudeau Liberals.

Because fossil fuels must be replaced by clean energy in the next nine years to meet the Paris 2015 targets commitments. No cost is too high.

Yet.

But globally, billions face much more pressing, life-sustaining challenges.

In the short-term, powerful, real-world market forces are making us all acknowledge what really drives international oil and energy markets.

In the medium and long term, we’ll learn how much discomfort, dislocation and lost opportunity the rest of the world is prepared to accept to fulfill the energy infrastructure decarbonization goals of the west’s warm and wealthy.

David Yager is an oil service executive, energy policy analyst, oil writer and author of From Miracle to Menace – Alberta, A Carbon Story. More at www.miracletomenace.ca

Share This: