CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Enjoy the recovery for now, but brace for inevitable disruptions

Despite the possibility of oversupply, trade disputes, and slowing economic growth, oil prices have steadily recovered in 2019 – both internationally and in Canada. The hope, as it should be, is that this welcome period of rising oil prices and lower volatility will continue as we move towards 2020.

Unfortunately, that hope may be short lived, as the conditions that resulted in significant instability in broad equity markets and commodity prices in late 2018 are still very much in play in 2019.

Crude oil prices rebounding in 2019 after late-2018 price swings

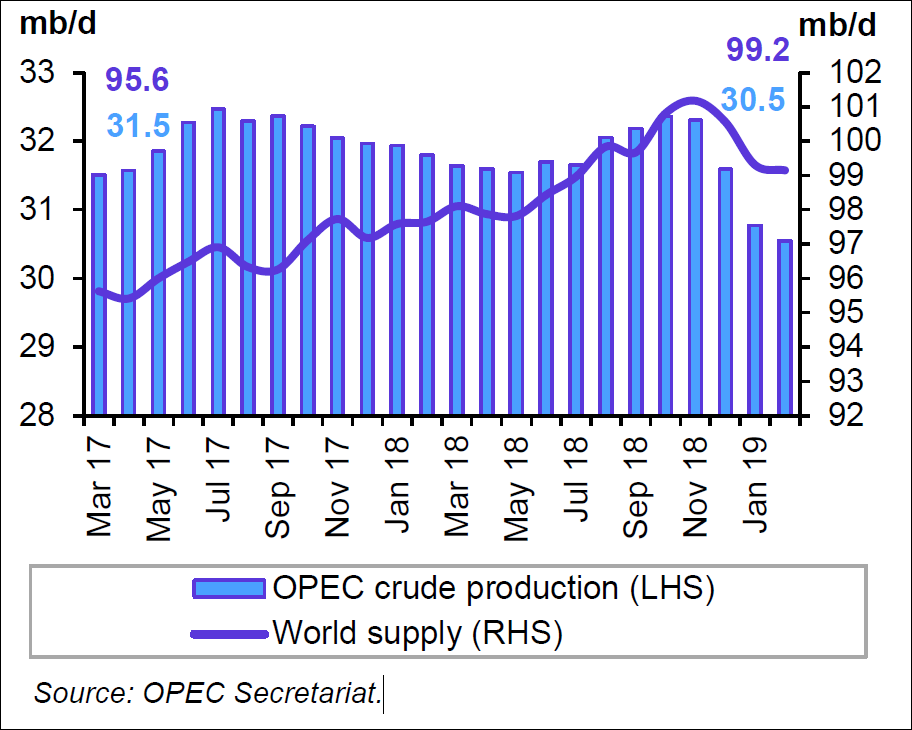

Tighter global market supply is primarily the result of production cuts from OPEC+ (OPEC plus Russia). OPEC crude oil production volumes have trended down in early 2019, consistent with the December decision to cut 1.2 MMbbl/day to support oil prices.

OPEC’s internal crude oil production estimates show a total production of 31.6 MMbbl/day in December 2018, 30.8 MMbbl/d in January 2019, and 30.5 MMbbl/day in February 2019. The bulk of the reduction comes from Saudi Arabia and Venezuela production. Although current supply and demand are near balance, the availability of significant spare capacity could act as a ceiling to more significant oil price gains.

Policy change or incomplete compliance to current production limits could quickly upend the market. Any supply shortfall from collapsing Venezuela production or reduced Iranian oil exports (which depends on whether the United States decides to extend waivers from sanctions that expire in May) is not expected to have a significant effect on total OPEC supply as Saudi Arabia has ample spare capacity that can quickly be brought back on production.

Crude by rail a major factor in Canadian oil prices

Canadian oil prices have recovered from record discounts vs. WTI with the implementation of mandatory curtailments in Alberta. The strong demand for Canadian heavy oil from US Gulf Coast refiners continues as they look to replace Venezuelan heavy oil imports. Heavy Canadian crude that can access the US Gulf Coast has been selling at a premium to WTI, improving crude by rail economics despite the historically low Western Canadian Select (WCS) differential of around $10 US/bbl.

The gradual reduction in the size of the curtailment program has not resulted in widening oil price differentials to WTI so far. The original curtailment of 325 Mbbls/day was reduced by 75 Mbbls/day in February with proposed reductions in April, May, and June of 25 Mbbls/day per month.

With Enbridge’s recent announcement that their Line 3 pipeline expansion is set for completion a year later than anticipated, the ability to move more oil out of Alberta in 2019 depends on increasing the volume of crude transported by rail. We expect the WCS differential to WTI to widen from current levels as curtailment unwinds and as we wait for increased pipeline takeaway capacity.

Natural gas prices looking to improve in the long term

Despite a significant cold snap, North American natural gas prices continue to languish amid surging US production and international market access constraints. Western Canadian gas continues to sell at a significant discount to Henry Hub. Early 2019 Western Canadian gas production volumes are slightly below 2018 values while US production continues to see robust growth.

The significant gap between North American and international natural gas prices continues to incentivize the development of LNG export capacity. With the advancing development of LNG exports, we anticipate price improvement in the long term, falling more in line with global natural gas prices.

Be wary of economic disruption

Overall economic growth is slowing, and many pundits are touting the increased risk of an economic recession. Heightened expectations of economic disruption are expected to add volatility to commodity prices and capital markets. Let’s take a moment to appreciate the start of spring and the relative calm of early 2019 while preparing for potential disruptions.

GLJ’s recently released April price forecast has WTI and Brent long-term forecasts as 69.00 USD/bbl and 73.00 USD/bbl, respectively (in real 2019 dollars). GLJ’s gas price forecasts have been adjusted with Henry Hub and AECO long-term forecasts at 3.20 USD/MMBtu and 2.92 CAD/MMBtu, respectively (in real 2019 dollars).

About GLJ Petroleum Consultants

GLJ Petroleum Consultants Ltd is a leading energy resource consulting firm. With comprehensive industry expertise and client-focused philosophy, GLJ provides technical excellence to a global client base. The company’s long-term record of success comes from an experienced team of professionals who have an absolute commitment to delivering high-quality results for their clients.

Learn More: https://www.gljpc.com

Share This: