CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Biomethane and e-methane could be additional trump cards in the ocean carrier industry’s complex game of bridge

By Resource Works

More News and Views From Resource Works Here

The bridge to a decarbonized commercial shipping fleet needs widening.

The current single-lane liquefied natural gas (LNG) option is too narrow to get containership fleets to the emission-reduction destination in the time mandated by the International Maritime Organization (IMO) and other global shipping agencies.

Budget and timeline pressures

Budget and timeline pressures are intensifying.

Compliance with FuelEU Maritime regulations and the IMO’s Net Zero Framework (NZF) are just two pressure points.

As noted previously in the Substack Shipping News, the estimated annual cost to decarbonize maritime shipping ranges between US$8 billion and US$28 billion.

Compliance with the IMO’s NZF, according to some estimates, would double containership fuel costs by the mid-2030s.

However, even though the decision to delay the NZF adoption vote to October 2026 could postpone net-zero carbon mandates into the 2030s, decarbonization momentum continues to tread water.

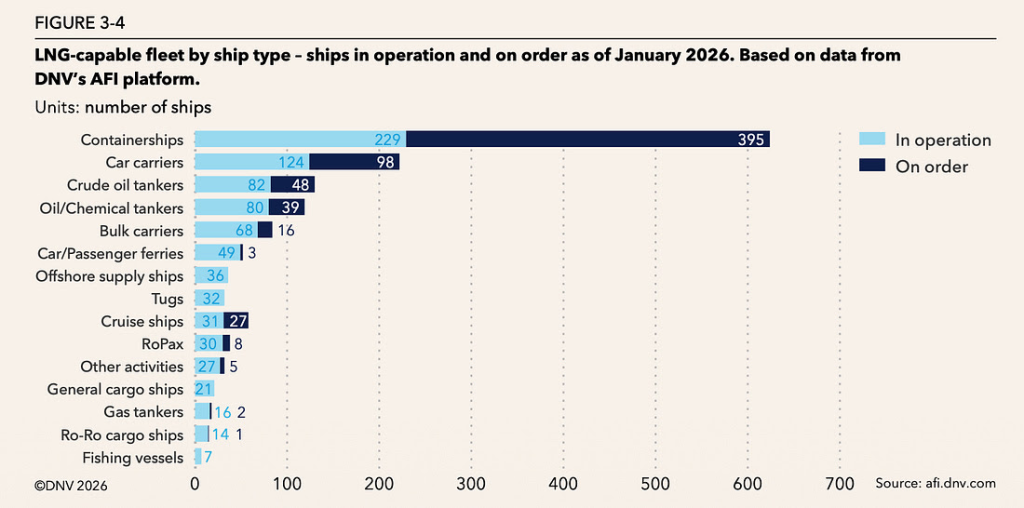

DNV notes in the maritime industry risk-management company’s Methane in Shipping report that there are now more than 800 LNG-capable ships. That is up 330% from five years ago. Another 600 have been ordered.

The container shipping sector is by far the leader in shifting to dual-fuel propulsion technology to comply with lower emissions regulations on its way to a decarbonized future | DNV’s Methane in Shipping report

There are also 700 LNG carriers and 300 on shipyard order books.

Still, in a global fleet of approximately 109,000 ships, the percentage that can run on fuel other than heavy marine oil remains small. And the ability to burn alternative fuel does not mean a ship will use that option.

The primary bridging fuel

That brings us back to the one-lane bridge fuel to a cleaner shipping future, and the three pillars DNV says are needed to support a bridge that includes low GHG-methane (biomethane and e-methane):

- Ship technology to use the fuel;

- Commercial production and availability of low-GHG methane; and

- Low-GHG methane bunkering infrastructure to refuel ships.

Progress in checking those boxes is ongoing.

Low-GHG methane also has many advantages over more expensive, more hazardous, and less commercially available options, such as ammonia and hydrogen.

LNG, however, remains the primary bridging fuel for shipping.

Primary, but pricey.

According to DNV, LNG technology increases the price of a large cargo ship by roughly 20% compared with its heavy marine oil-fuelled counterpart.

On the positive side of the ledger, LNG is widely available and has been used for nearly half a century in the shipping industry. It reduces nitrogen oxide emissions by up to 90%, sulphur oxide emissions almost entirely, and particulate matter significantly.

Ships powered by LNG can burn low-GHG methane and biodiesel. They can also be reconfigured to run on ammonia and other low-carbon options that are still not commercially viable.

So, when you are set to sink US$110 million today into a new 10,000 TEU containership that traditionally has a working life of at least 25 years, technical flexibility to keep it current with emissions regulations well into the future is a priority.

That extra US$20 million fuel-flexibility premium will likely be cheaper than the penalties and potential lost business resulting from noncompliance with increasingly stringent emissions regulations.

Low-GHG methane, which can be produced from sustainable biomass and renewable electricity, can be swapped into existing LNG infrastructure.

It can therefore increase capacity and velocity on the bridge to a cleaner container shipping future.

Challenges and speed limits

Not without challenges, however.

Availability is one.

The DNV report estimates that roughly 20,000 tonnes of biomethane were bunkered by ships at 17 ports in 2025, but electricity generation and land-based transportation consume the lion’s share of biomethane production today.

E-methane is far less available.

Another speed limit on the decarbonization bridge: cost.

According to the DNV report, the December 2025 price of liquefied biomethane in Rotterdam was three times the price of LNG. It estimated that e-methane would be at least double the price of biomethane.

Fear of the unknown also complicates shipping’s risk management calculus.

“For a fuel to achieve broad adoption,” says the DNV report, “confidence must extend beyond early adopters to the majority of shipowners and charterers. These stakeholders need assurance that the fuel is reliable and safe for routine operations.”

To that end, as the report notes, there are approximately 1,700 biomethane plants in Europe and another 500 in North America. Among the major energy players with biomethane production skin in the game: TotalEnergies (EPA:TTE), Shell (LON:SHEL), and BP (NYSE:BP).

So, we have a widened fuel bridge to decarbonized shipping, but we do not have a headcount of who is ready, willing, and able to pay the tolls required to cross that bridge to get to the other side.

This article originally appeared in The Substack Shipping News. Timothy Renshaw can be reached at [email protected].

Share This: