CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

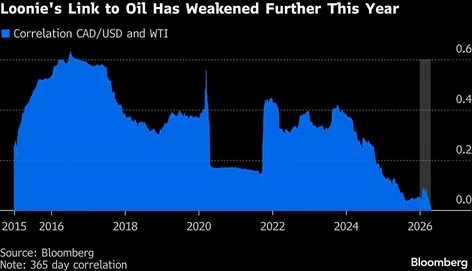

The declining competitiveness of Canada’s oil extraction has also helped decouple the currency from oil prices

By Anya Andrianova and Erik Hertzberg

When oil prices surge, the Canadian dollar usually strengthens — but that dynamic has shifted.

Since the war in the Middle East erupted in late February, the loonie slipped 0.2 per cent against the United States currency as West Texas Intermediate crude oil rose roughly 34 per cent. The divergence prompted traders to boost their bets against the Canadian dollar. Meanwhile, the Norwegian krone and Australian dollar, other commodity-linked currencies, have rallied in that period.

“In the current conflict, the Canadian dollar is showing more responsiveness to risk off than oil prices,” said Noah Buffam, strategist at CIBC Capital Markets. “In recent years, the loonie sensitivity to oil prices has been declining as investment in the oil sands has been falling as a share of the economy.”

CIBC recommends betting on the Australian dollar gaining to parity with the Canadian currency from the current levels of 0.9775. Foreign-exchange strategists at JPMorgan Chase & Co. suggest shorting the loonie against the Australian dollar and Norwegian krone. The bank, along with Citigroup, also advises selling the Canadian currency against the Mexican peso as the Canada-U.S.-Mexico trade agreement review process begins.

Traders have been souring on the loonie, with hedge funds turning the most bearish on the currency this year in the week through April 14. Consumer price growth has accelerated, but excess supply in the economy and the ongoing uncertainty posed by U.S. tariff policy and the war in Iran are likely to keep the Bank of Canada on hold when it sets interest rates next week. When the correlation was stronger, the higher oil prices drove inflation higher, but part of it was mitigated by a stronger domestic currency. This buffer is no longer there.

The declining competitiveness of Canada’s oil extraction has also helped drive a decoupling of the currency from oil prices.

As recently as 2013, Canada’s loonie traded at — or above — parity with the U.S. dollar. That strength coincided with a wave of foreign investment, as global energy firms poured capital into Canada’s oilsands to extract heavy crude. The high-cost nature of this production was justified by constrained North American supply and oil prices near US$100 per barrel.

Foreign investment to expand production often took place in the form of reinvested profits into the oil sands, pushing up demand for Canadian dollars. Then came the collapse of oil prices in 2014, as the U.S. shale boom opened up cheaper sources of production, making expanding oil sand production in Canada less appealing.

Canadian companies are returning a big portion of their revenue to shareholders, where 75 per cent of those are not Canadians, meaning a smaller share of oil revenue is being invested back into operation and domestic economy, diminishing demand for the local currency, according to Charles St-Arnaud, chief economist at Servus Credit Union.

The source of the oil price shock also plays a role in how closely tied the loonie is to the commodity, according to Olivier Gervais, director of modelling and forecasting at Scotiabank. It depends on whether the oil shock event is driven by demand or supply, he said in a Thursday note.

“Despite the apparent decoupling between the CAD and oil prices, the link has not completely disappeared,” he wrote. “Should future oil price gains be driven more clearly by global demand, the correlation could re‑emerge.”

Bloomberg.com

Share This: