CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Revenue Effects of Tax Rate Changes in Alberta

- As recently as 2014, Alberta enjoyed a significant tax advantage, which included a single 10% personal income tax (PIT) rate, the lowest in Canada. However, in 2015, the newly elected NDP government introduced a progressive five-bracket PIT system with a top rate of 15%, eroding Alberta’s tax advantage.

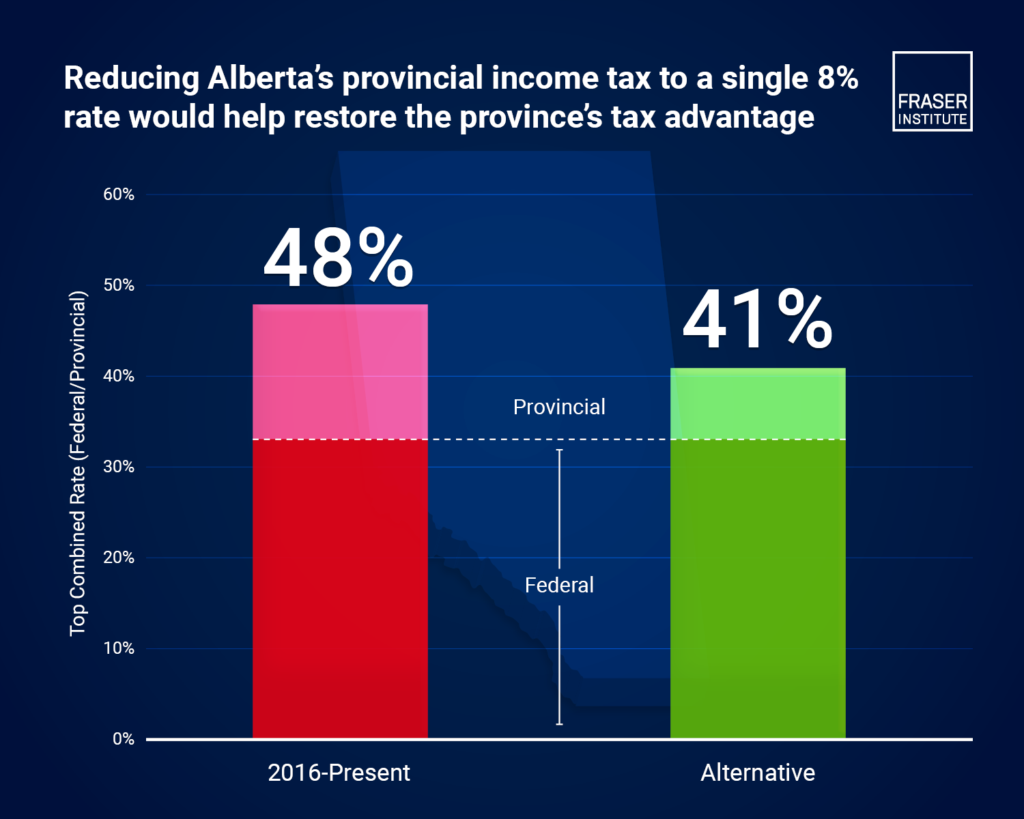

- Alberta’s top combined provincial and federal PIT rate is 48%, ranking it the tenth highest in North America. As well, its tax competitiveness is lower, compared with other energy-producing regions.

- The main objective of this study is to examine the revenue implications of replacing Alberta’s current five-bracket PIT system with a single rate of 8%. The study analyzed three alternative reform scenarios: Immediate transition to an 8% single rate starting in 2025, gradual transition to 8% over three years, ending in 2027, and an immediate 20% across-the-board tax reduction in the current five-bracket system in 2025.

- After accounting for the positive behavioural effects of reduced taxes, this study finds that if Alberta immediately switches to a single 8% PIT rate, PIT revenue would drop by $6.1 billion (a 35.6% reduction) in the first year. Gradual transition to a single 8% rate would initially reduce revenue by $264 million (1.5%), rising to $6.9 billion (a 37.0% decline) by 2027. In contrast, an immediate 20% across-the-board cut in the current PIT system would reduce provincial revenue by $5.1 billion (a 29.5% drop) in 2025.

Share This: