CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

“You’ll forgive me if I don’t think about monetary policy.” So spoke Prime Minister Justin Trudeau on the campaign trail before the September 20, 2021, election.

Obviously, many Canadians weren’t thinking about it either because they elected the Trudeau Liberals for the third time in six years.

What a difference a year makes. All the major issues today are fundamentally economic. Rising inflation and interest rates and the escalating cost of everything, particularly energy and food. This is extremely acute in Europe where skyrocketing energy costs have created an economic crisis. Depending on how cold it gets this winter, it could deteriorate into a humanitarian disaster.

How did we get into this mess?

The default answer is Russia’s invasion of Ukraine in February, and Vladmir Putin’s subsequent reduction of natural gas deliveries via the Nord Stream I pipeline. That just got worse due to alleged subsea sabotage rendering Nord Stream I and its sister line inoperable.

But the problems with European energy markets were well underway a year ago. The price of electricity spiked when calm winds exposed the risks of Europe’s increasing reliance on renewable energy. Backup gas and coal-fired power generation, considered undesirable for years, was limited or mothballed.

Today there is growing recognition that years of underinvestment in replacement oil and gas production, persecution of fossil fuels in every way possible, and the political overselling of the commercial utility of existing low-carbon energy alternatives have played a significant role the current predicament.

Because whatever the climate concerned have been told or want to believe, wind and solar are not yet dependable alternatives in scale for oil, gas and coal 24/7/365. Fossil fuels have an established global delivery and distribution infrastructure. Electricity does not. This fundamental strength of the incumbent is rarely mentioned.

But if Canada will re-elect a Prime Minister who, by his own admission, has little interest in or understanding of macroeconomics, can voters in all the other countries which elected “climate friendly” governments be any wiser?

If this many voters pay little or no attention to economics, physics, or energy security of supply, it no surprise that the political agenda has been hijacked by actors with agendas not necessarily focused on the basic needs of ordinary citizens.

**********

A major contributor the current situation was the five frothy years from early 2015 to early 2020 when the world really did believe was no longer bound by fundamentals of energy, finance and economics. This was when many of the grand plans to save humanity from itself that aren’t working today were conceived.

Fossil fuel divestment. ESG investing. The 2015 Paris emission reduction commitments. Net Zero by 2050. Decarbonization through a global “energy transition.” Mark Carney’s Glasgow Financial Alliance For Net Zero (GFANZ). Suing oil companies for alleged malfeasance and future climate damage. Pipeline protests and cancellations. Governments elected around the world on pro-climate, anti-carbon platforms. Modern Monetary Theory, the premise that government debt no longer matters.

In the back half of the last decade, things were going so well for so many that material needs – the basics of energy, food, housing and the cost of living – were taken for granted. As was energy security of supply.

In an era of low prices and energy plenty, it become accepted – even essential – that mankind could and should make massive changes to its energy types and sources without a thorough analysis of the cost, challenges or potential for disruption.

Those who asked the tough questions were routinely dismissed as climate change deniers.

Most people only worry about the long-term future of the climate when their immediate necessities have been satisfied. Such was the case from 2015 to 2020.

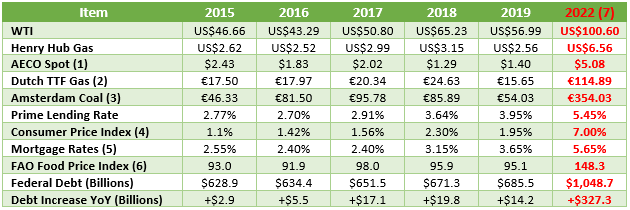

Following are some of the major macroeconomic indicators from this period and their most recent 2022 values.

- Alberta government AECO spot reference price

- Dutch TTF Gas Futures in MW/day average month 2015 – 2019, YTD average 2022

- Price per tonne, last month each year 2015 – 2019; average last five-months of 2022

- Annual average 2015 – 2019, month of August 2022.

- 5- year rate annual average, current rate 2022

- UN Food & Agricultural Organization global index of meat, dairy, cereals, vegetable oil and sugar, YTD average for 2022

- YTD average for WTI, Henry Hub, AECO, latest rates for interest, mortgages, CPI, 2021 federal debt fiscal year ended March 31/22

During these five years the global petroleum industry was in tough shape because of the oil price collapse. But the rest of the world was doing great. That’s because the global economy got a huge financial boost from much lower energy input costs.

But for 2022 the exact opposite is true. Fossil fuels prices are much higher. But as the cost of energy increases, so does the cost of everything else being extracted, grown, processed, manufactured or distributed.

Prices for gas and coal in 2022 in Europe are five times higher than the five-year averages for 2015 to 2019.

Canada’s core inflation rate for August was over three times higher than the five-year average.

The UN’s Food and Agricultural Organization food price index average for 2022 is 50% higher than these five years.

It took a long time to create this situation. Rising public debt even while the economy was doing well was a carry-over from the 2008/2009 world economic crisis. Coined the Great Recession, the collapse or near-collapse of major financial institutions like Bear Stearns, Lehman Brothers and AIG (American International Group) due to overleverage, subprime mortgages and credit default swaps, caused central banks to vastly increase liquidity to sustain investor confidence.

The fact that oil in 2008 had reached an all-time record high of US$145.31 on July 3 – which made everything more expensive for everyone – is notably absent from the historical record. Converted to 2022 dollars, it was US$171 a barrel. That same day Henry Hub gas closed at US$13.00, US$17.88 in current dollars.

The Great Recession of 2008/2009 was instead blamed on greedy banks and subprime mortgages, not skyrocketing energy costs. However, oil prices and demand did indeed decline.

Even though real oil and gas prices are half what they were 14 years ago, the markets are fixated on the belief that the impending recession will cap oil prices and demand. This is always a factor when the price goes up and the economy goes down.

But the Great Recession did not have to grapple with the geopolitical supply drama caused by Russia and the multi-year anti-fossil fuel crusade. In 2008/2009 nobody was trashing fossil fuels, opposing new supplies, sabotaging international pipelines, or creating political embargoes on oil and gas from one of the world’s largest producers.

The behavior of oil prices in 2022/23 could be quite different than prior economic downturns if supply becomes as big an issue as demand.

While central bank “bazookas” in 2008 and 2009 had a positive effect in stabilizing the economy and investor confidence, governments clearly liked what they saw. So they continued the economic stimulus after the economy recovered.

It would certainly have been much different if they hadn’t.

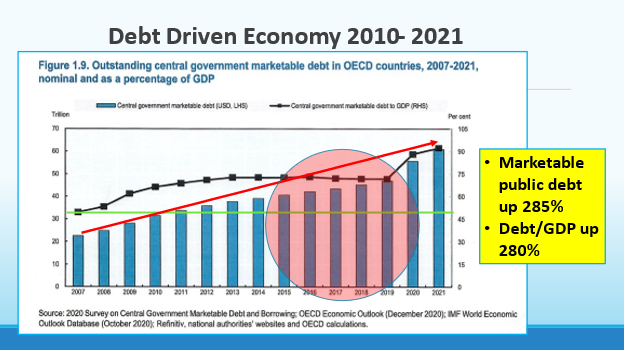

The following chart shows the debt to GDP ratio of the OECD countries from 2007 to 2021. Following the end of the Great Recession in 2010, the developed world continue to fund a debt-fueled economic party that never really ended until 2022.

Note the shaded area in red. This is the period when the collapse of oil and gas prices had a major positive impact on global economy. Before the Great Recession, the debt/GDP ratio of the OECD countries was only about 35%. By 2010 it was up nearly one-quarter to 45%. It peaked at nearly 50% in 2013 and 2014.

But then the debt/GDP ratio declined for the next five years. Why? Because the energy price collapse turbocharged the economy by reducing the cost of everything and increased everyone’s disposable income. Even as public debt grew continuously, the only declines in the debt/GDP ratio during this period were achieved because of lower energy costs.

Central banks kept the money flowing and debt rising anyway. They gave it a nice name, QE or quantitative easing. Then Modern Monetary Theory became a popular policy discussion, the idea that governments could create liquidity and support the economy forever because continually rising government debt levels didn’t matter.

Record low interest and inflation rates supported this thesis.

What kept inflation in check as central banks continued to prime the economic pump was greatly reduced energy input costs. This made everything more affordable. Including wind turbines and solar panels.

Then along came the pandemic and more heavy government borrowing. According to this chart, debt/GDP in 2021 was over 90% which made it 280% higher than it was in 2007. Total central government debt for the OECD countries nearly tripled.

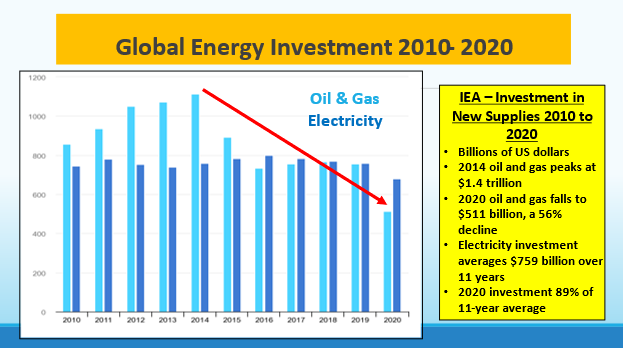

With oil and gas prices in the dumpster and the western crusade against fossil fuels well underway, from 2015 onwards the developed world got what it had convinced itself it needed – a massive decline in investment in new supplies of oil and gas. Here’s the data for annual global capital investment in new energy supplies from the International Energy Agency.

Plummeting capital expenditures in new oil and gas supplies from 2015 to 2020 was driven by several factors including low commodity prices. But this was assisted by the multi-pronged attack on fossil fuels through restricted debt and equity capital, market access restrictions, and continued interference in where new supplies could be developed.

OPEC, IEA and major producers like ExxonMobil have warned for years that underinvestment would cause a supply crunch in 2022 or 2023. Low-carbon energy supplies were not being developed in sufficient scale to move the needle on materially replacing fossil fuels globally.

Hydrocarbon shortages were exacerbated by Russia’s invasion of Ukraine. And with one of the world’s largest oil and gas producers now a political pariah, the global supply issue has become much more complex.

**********

As the world became complacent and energy security concerns declined, elections were fought and won on pledges to inflict damage on current and future fossil fuels supplies.

Climate was a winner at the ballot box. Justin Trudeau’s Liberals won in 2015 in part by promising to kill the Northern Gateway pipeline. John Horgan’s NDP was elected in BC in 2017 by pledging to stop TMX. Francois Legault’s CAC in Quebec will likely win October 3 in part because of last year’s pledges to cancel LNG exports and make oil or gas production in that province illegal.

Similar campaigns took place all over Europe and in the US in 2020.

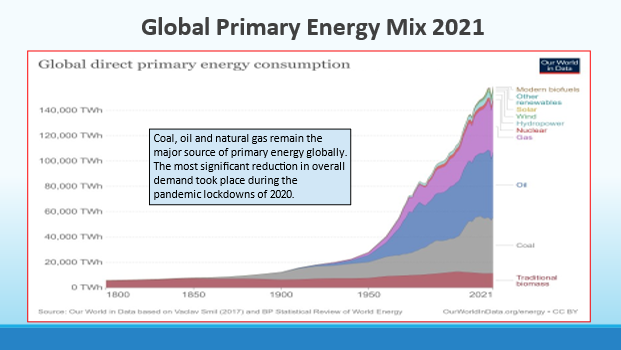

But reality looms. The following chart shows the progress of decarbonizing primary energy supplies in the past 50 years. For all the trillions spent on renewable energy, climate crusades, elections, protests, conferences, pledges, promises and endless public expressions of deep concern, fossil fuels still power the world.

And given current circumstances, this is not going to change anytime soon.

What were we thinking?

But out of necessity rapid changes are underway. The UK is opening up North Sea exploration and revisiting its frac ban for shale gas. Those with mothballed coal fired power generation are restarting them. Nuclear plants scheduled for retirement and being kept going. European countries are securing LNG imports from anywhere but Russia. Germany is fast tracking floating LNG unloading terminals to get more non-Russian gas as quickly as possible.

Capital markets are changing fast. The “E” in ESG is much less important than even six months ago. While it is nice to believe investment managers are altruistic, this reversal is partly because energy is the top performing sector on the markets this year, and partly because many of the things that rose in value during the go-go years are undergoing a well-deserved correction.

American banks that supported GFANZ a year ago prior to the Glasgow COP 26 conference are considering pulling out of Carney’s US$130 trillion climate capital masterpiece. Jamie Dimon, CEO of JP Morgan, publicly accused banks that refuse to fund fossil fuels of creating “the road to hell for America.” The plan for western countries to somehow cap the price Russia gets for its oil will be impossible to enforce. And by the time the EU gets around to introducing its Russian oil boycotts on December 5, the way things are going nobody will remember who’s idea it was in the first place.

On September 26 Fortune published an article titled, “You really don’t understand how bad it could get in Europe this year.” It opened, “An energy crisis the likes of which hasn’t been seen in decades is unfolding around the world. Nowhere is this crisis more pronounced and more dangerous than in Europe, where a long-standing gambit on cheap Russian gas has backfired.”

It continued, “The situation is so dire that governments that previously renounced fossil fuels and nuclear power are desperately reopening coal plants and nuclear sites, and nationalizing utility companies to save them from going bankrupt. With winter and higher gas demand on the way, even the slightest uptick in energy demand anywhere in the world could entirely shut down some manufacturing sectors.”

There has been great market volatility around whether or not there will be a recession. Europe is already in recession, and depending on the weather and energy supplies things could get worse. It may take years for Europe’s economy to recover. The potential for massive human suffering is real and looming.

That the combination of climate politics and geopolitical conflict is destroying the economy of Europe is something that everyone in the public policy arena must consider when they make their next grand pronouncement about what the world must do next on decarbonization.

That the solution is more wind, solar or non-existent “green hydrogen” is so disconnected from reality that thankfully we’ll hear much less of this in the days, weeks and months ahead.

The fact that the governments responsible for keeping their countries functioning are looking for coal, not solar panels, explains the gravity of the crisis. Whatever the politicians said last campaign is being eclipsed by current events.

As the world goes in a different direction than what climate central planning envisioned, we must also reassess the future of fossil fuels.

Cheap, reliable, plentiful and versatile fossil fuels built the modern world. More oil, gas and coal at lower prices as soon as possible are essential to restoring order to the world economy.

The longer we wait, the worse the situation will become and the longer it will be before the world is back on its feet.

Canada must respond by expediting the rapid development and export of its enormous oil and gas resources. As conditions in Europe deteriorate, public opinion polling is showing that more Canadian support this position.

At some point even the Liberals will figure this out.

David Yager is an oil service executive, oil and gas writer, energy policy analyst, and author of From Miracle to Menace – Alberta, A Carbon Story. Find the book to www.miracletomenace.ca. He is President and CEO of Winterhawk Well Abandonment Ltd. which has commercialized a new casing expansion technology for improving annular wellbore integrity.

Share This: