CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Revenues from the oil and gas sector alone are worth 50 years of federal family allowance and children’s benefit payments

Download the PDF here

Download the charts here

Overview

This Research Brief estimates the gross revenue contribution that Canada’s energy sector broadly speaking, and the oil and gas sector specifically, made to federal, provincial, and municipal governments between 2000 and 2019. Gross revenues include personal and corporate federal and provincial income taxes, indirect taxes, royalties, and crown lease payments. This Research Brief updates previous research that the Canadian Energy Centre undertook on this subject.¹

In brief, on an inflation-adjusted basis,

- The energy sector’s cumulative fiscal contribution to federal, provincial, and municipal government revenue was $701.2 billion between 2000 and 2019, an average of nearly $35.1 billion per year.

- The gross revenue contribution to federal, provincial, and municipal governments exclusively from the oil and gas sector was $504.9 billion between 2000 and 2019, an average of $25.2 billion per year.

1. See CEC’s November 2020 Research Brief #6 which conservatively estimated energy revenues to federal, provincial, and municipal governments at $672 billion between 2000 and 2018.

Background

The broad energy sector in Canada is composed of oil and gas extraction and support activities, utilities (including renewables such as hydro, wind, and solar), petroleum and coal product manufacturing, and pipeline transportation. The oil and gas sector is composed of oil and gas extraction and related support activities.

This Research Brief also makes some broad comparisons between the gross revenue contributions of the energy sector and the oil and gas sector with two other sectors, namely, construction and real estate. The reader should be aware that:

- Numbers for the oil and gas sector are included in the broad energy sector.² The reason for displaying both is that separating out “oil and gas” from “energy” answers the question of how large Canada’s oil and gas sector is vis-à-vis the broad energy category (which also includes, for example, hydro).

- To avoid double-counting, we do not compare the energy sector or the oil and gas sector to manufacturing.³ The potential for double-counting is related to North American Industry Classification (NAICS) categories, where manufacturing includes some oil and gas (manufacturing) activity. (For example, petroleum refining is part of both the energy and the manufacturing sectors.) They are thus not distinct data sets that can be compared side by side, given the overlap. In other words, if we compared the manufacturing sector to the oil and gas sector we would be double-counting because the manufacturing sector includes oil and gas manufacturing.

- We also do not compare energy or oil and gas to the automotive sector or the aerospace sector. The reason is again related to NAICS classifications that make such comparisons difficult, as well as limitations with the data from Statistics Canada beyond personal income taxes.⁴

2. In making these broad types of sectoral comparisons, Statistics Canada uses the North American Industry Classification (NAICS) system to establish the boundaries for various sectors. Under NAICS, sectors are broken down by two-number NAICS (i.e., 23 is construction), three number NAICS (i.e., 531 is real estate), four-number NAICS (i.e., 3361 is motor vehicle manufacturing) and five-number NAICS (i.e., 33612 is heavy-duty truck manufacturing), and so forth. 3. Manufacturing has a broad NAICS (i.e., 31, 32, and 33), and there are close interactions between energy, oil and gas, and broad manufacturing, i.e., how petroleum refining is part of both the energy and manufacturing sectors. 4. In technical terms, since the broad energy sector and the specific oil and gas sector are composed of two- and three-number NAICS, we limit our comparisons, as much as possible, to other two- and three-number NAICS, such as construction (23) and real estate (531).

The revenue estimates for the energy sector and the oil and gas sector are low

The $701.2 billion figure from the broad energy sector and the $504.9 billion figure from the more specific oil and gas sector are conservative estimates of government gross revenues. (For more detail, see Appendix A: Explaining “Gross Revenues.”) They exclude:

- Federal and provincial personal income taxes or direct taxes from persons paid by employees who worked in Canada’s energy sector between 2000 and 2006;

- Income effects resulting from spending on goods and services by Canadians who benefit from the energy sector. (By “income effects,” we mean income generated by the broad energy industry and its agents or suppliers, which gives rise to various types of personal consumer spending across the entire economy. Such consumer spending stimulates GDP, output, and employment in other sectors such as retail, service, and leisure, which then bolsters federal, provincial, and municipal revenues); and

- Taxes, fees, and revenues from benefit agreements paid to First Nations governments.

Summary of Key Findings

Revenues to governments from the broad energy sector: $701 billion

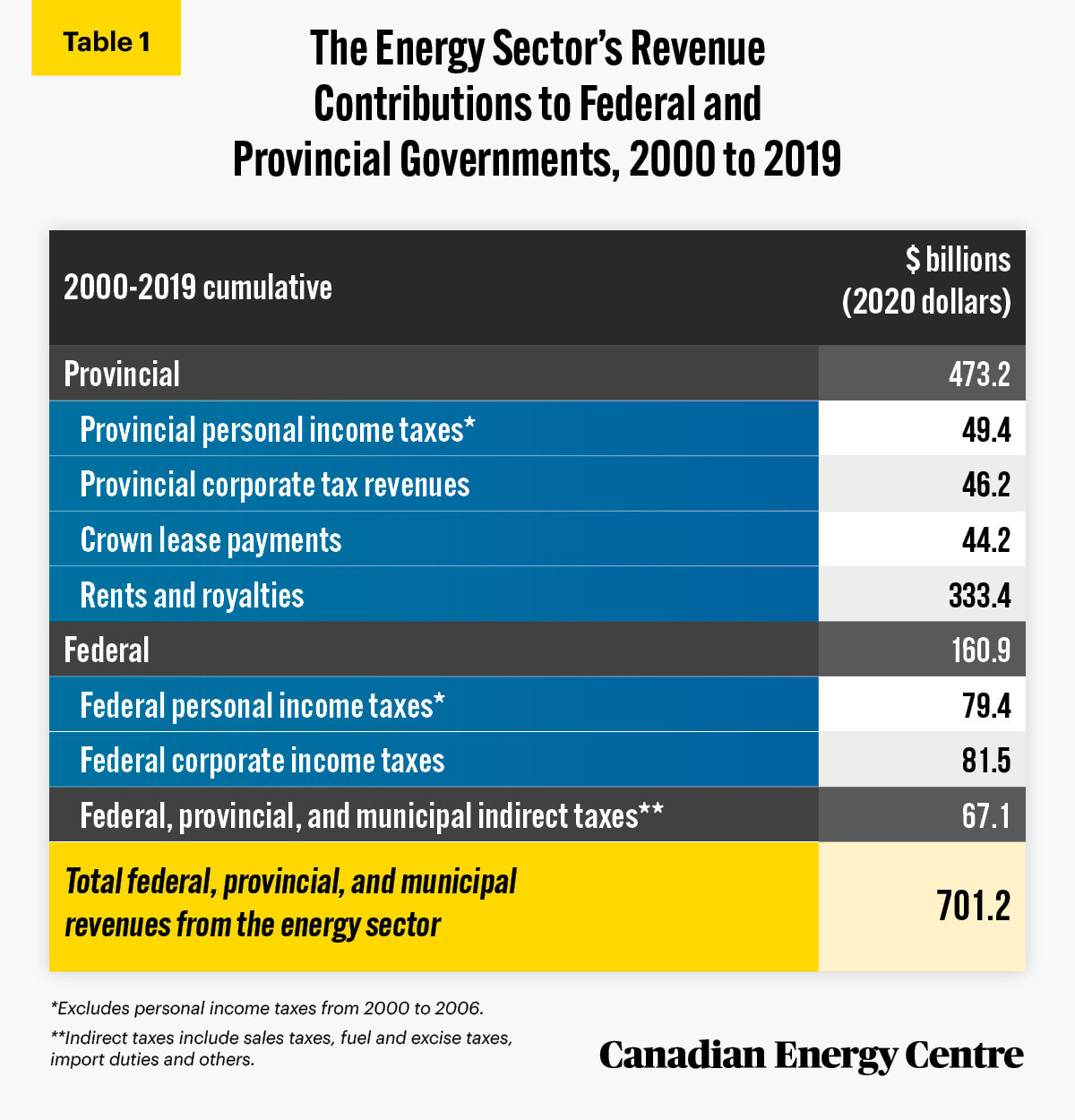

On an inflation-adjusted basis to 2020 dollars, the Canadian energy sector’s cumulative fiscal contribution to federal, provincial, and municipal government revenue was $701.2 billion between 2000 and 2019, an average of $35.1 billion per year (see Table 1).⁵

The $701.2 billion figure includes $473.2 billion in direct provincial revenues, $160.9 billion in direct federal revenues, and $67.1 billion in indirect federal, provincial, and municipal taxes.

5. The nominal figure is $591.7 billion, or an average of $29.6 billion per year. Constant dollars (i.e., inflation-adjusted to 2020) is a more accurate way of comparing revenues (or any other number) over the years. This is because, for example, $10 billion in revenues in 1950 would be very different than $10 billion in 2020 given the erosion of the dollar’s value over 70 years. In this study, we thus use inflation-adjusted 2020 dollars.

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

The contribution from the oil and gas sector alone: $505 billion

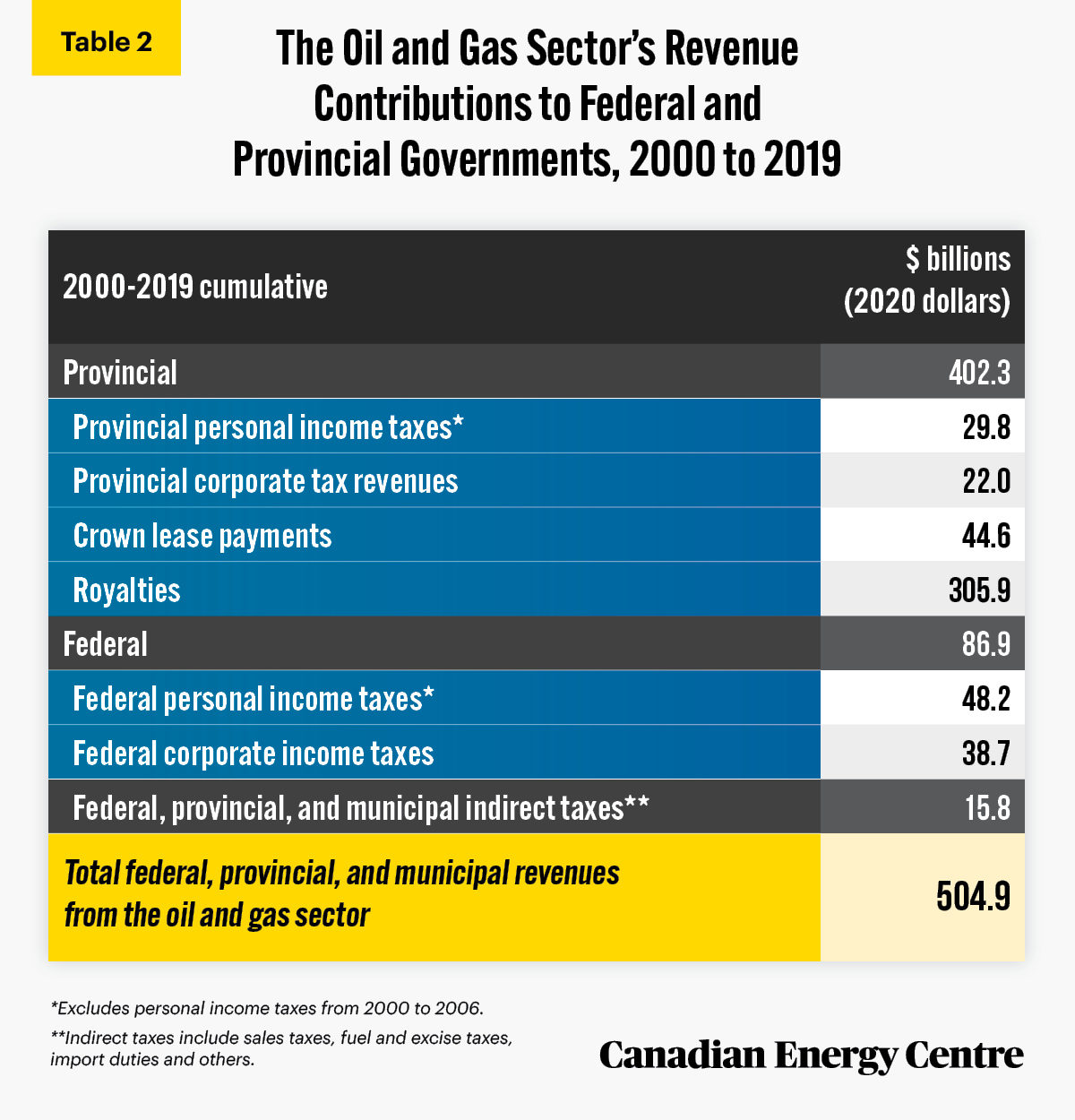

The gross revenue contribution to federal, provincial, and municipal governments exclusively from the oil and gas sector was $504.9 billion between 2000 and 2019, an average of $25.2 billion per year (see Table 2).

The $504.9 billion figure includes $402.3 billion in direct provincial revenues, $86.9 billion in direct federal revenues, and $15.8 billion in indirect federal, provincial, and municipal taxes.

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

Placing $701 billion and $505 billion in context

To put the $701.2 billion in energy revenues (or the $504.9 billion in oil and gas revenues) into context, we compare those figures with recent expenditures or other recent figures, all adjusted for inflation.

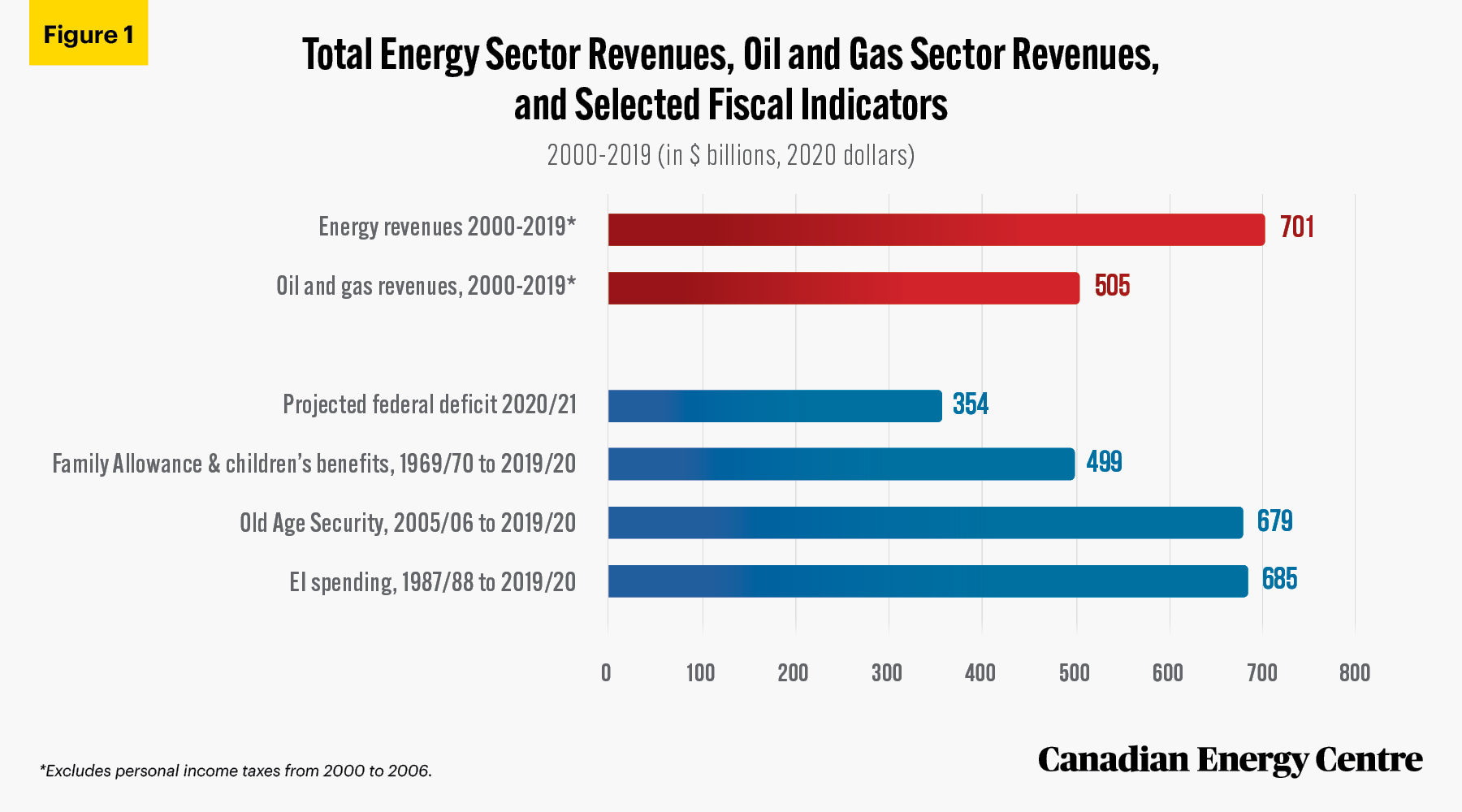

The $701.2 billion in energy revenue is:

- Nearly twice the latest forecast of the federal budget deficit of $354 billion for 2020/21;

- More than the $679 billion paid out in old age security (OAS) benefits between 2005/06 and 2019/20; and

- More than the $685 billion in Employment Insurance benefits paid out between 1987/88 and 2019/20.

The $504.9 billion in oil and gas revenue is:

- More than the $499 billion in Family Allowance and children’s benefits paid out between 1969/70 and 2019/20 (see Figure 1).

Sources: Statistics Canada, 2021 a, b, c, d, e, f, g; CAPP, 2021.

A Breakdown of Revenues from the Energy Sector

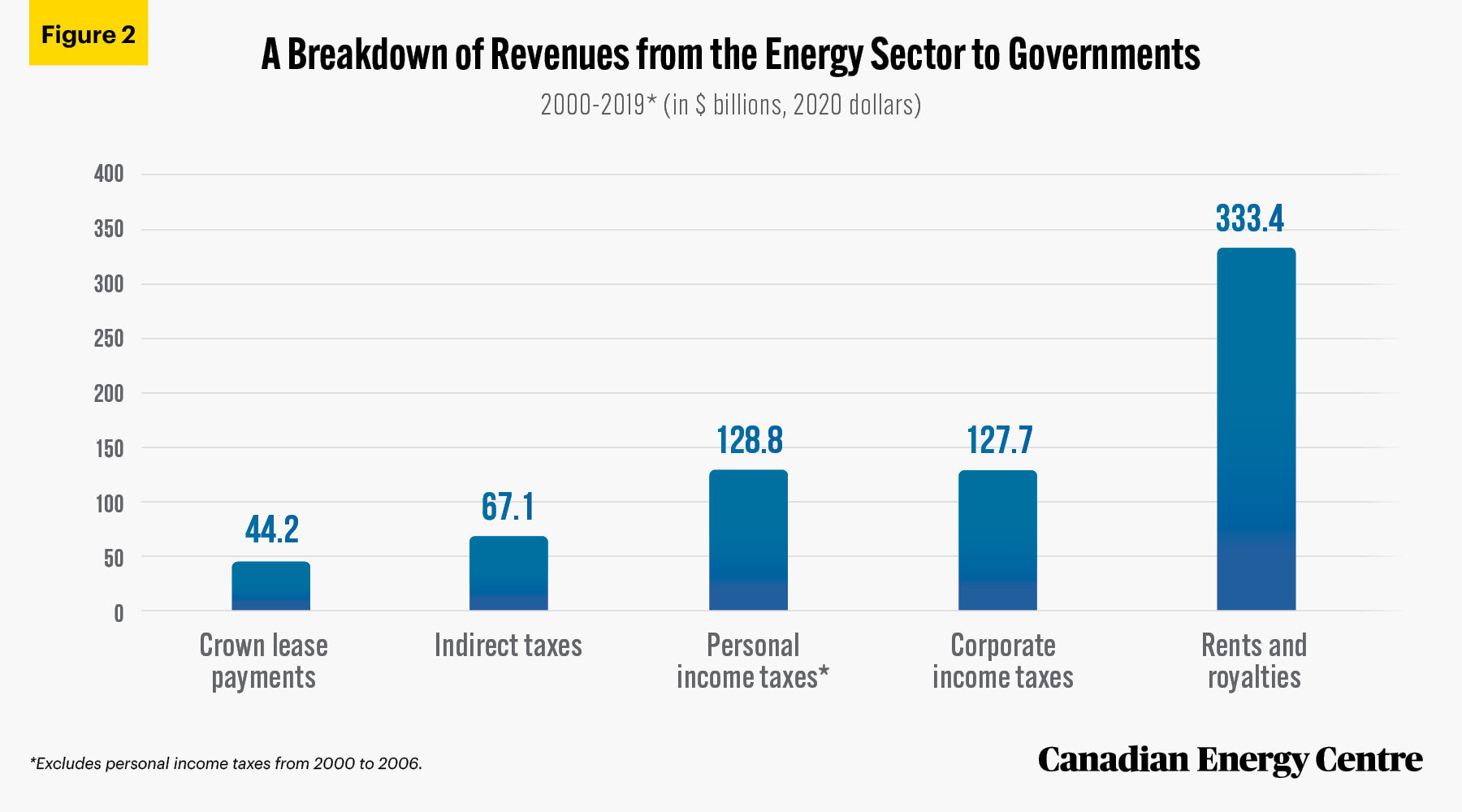

The energy sector pays revenues to government in five main ways: crown lease payments, indirect taxes, personal income taxes, corporate income taxes, and rents and royalties (see Figure 2).

Crown lease payments: $44.2 billion

The Canadian energy sector makes crown leases payments for the leasing of rights that enable companies to explore for and develop petroleum and natural gas resources.

Between 2000 and 2019, the Canadian energy sector made $44.2 billion in crown lease payments to provincial governments, an average of $2.2 billion per year.

Indirect taxes: $67.1 billion

The Canadian energy sector pays indirect taxes annually as a result of its activities. Those indirect taxes include federal and provincial sales taxes, federal and provincial gas taxes, federal excise taxes, federal import duties, and others.

Between 2000 and 2019, Canada’s energy sector paid $67.1 billion, an average of nearly $3.4 billion per year in indirect taxes to the federal government, the provinces, and municipalities.

Personal income taxes: $128.8 billion

Canadians employed in the energy sector pay federal and provincial income taxes, primarily on annual income earned from salaries, wages, and commissions. (For more information, see Appendix B: Personal Income Tax Revenue Comparisons.)

Between 2007 and 2019, Canadians employed in the energy sector paid $128.8 billion in federal and provincial personal income taxes on salaries, wages, and commissions—about $9.9 billion per year. Note that this does not include federal and provincial personal income taxes collected from the energy sector between 2000 and 2006, which are not available from Statistics Canada at this time.

Of that $128.8 billion, federal personal income tax revenues were $79.4 billion and provincial personal income tax revenues were $49.4 billion.

Corporate income taxes: $127.7 billion

Corporations and business enterprises in Canada’s energy sector pay federal and provincial corporate taxes on their annual net profits. (For more information, see Appendix C: Corporate Income Tax Revenue Comparisons.)

Between 2000 and 2019, the energy sector paid $127.7 billion, or nearly $6.4 billion per year in federal and provincial corporate income taxes.

Of that $127.7 billion, Canada’s energy sector paid $81.5 billion in federal corporate income taxes and $46.2 billion in provincial corporate income taxes.

Rents and royalties: $333.4 billion

The Canadian energy sector pays rents and royalties to provincial governments on the production of natural resources such as conventional oil and natural gas, oil sands, and hydro.

Between 2000 and 2019, the energy sector paid $333.4 billion, or an average of $16.7 billion per year in rents and royalties to provincial governments.

Sources: Statistics Canada, 2021 a, b, d, e, f, g; and CAPP, 2021.

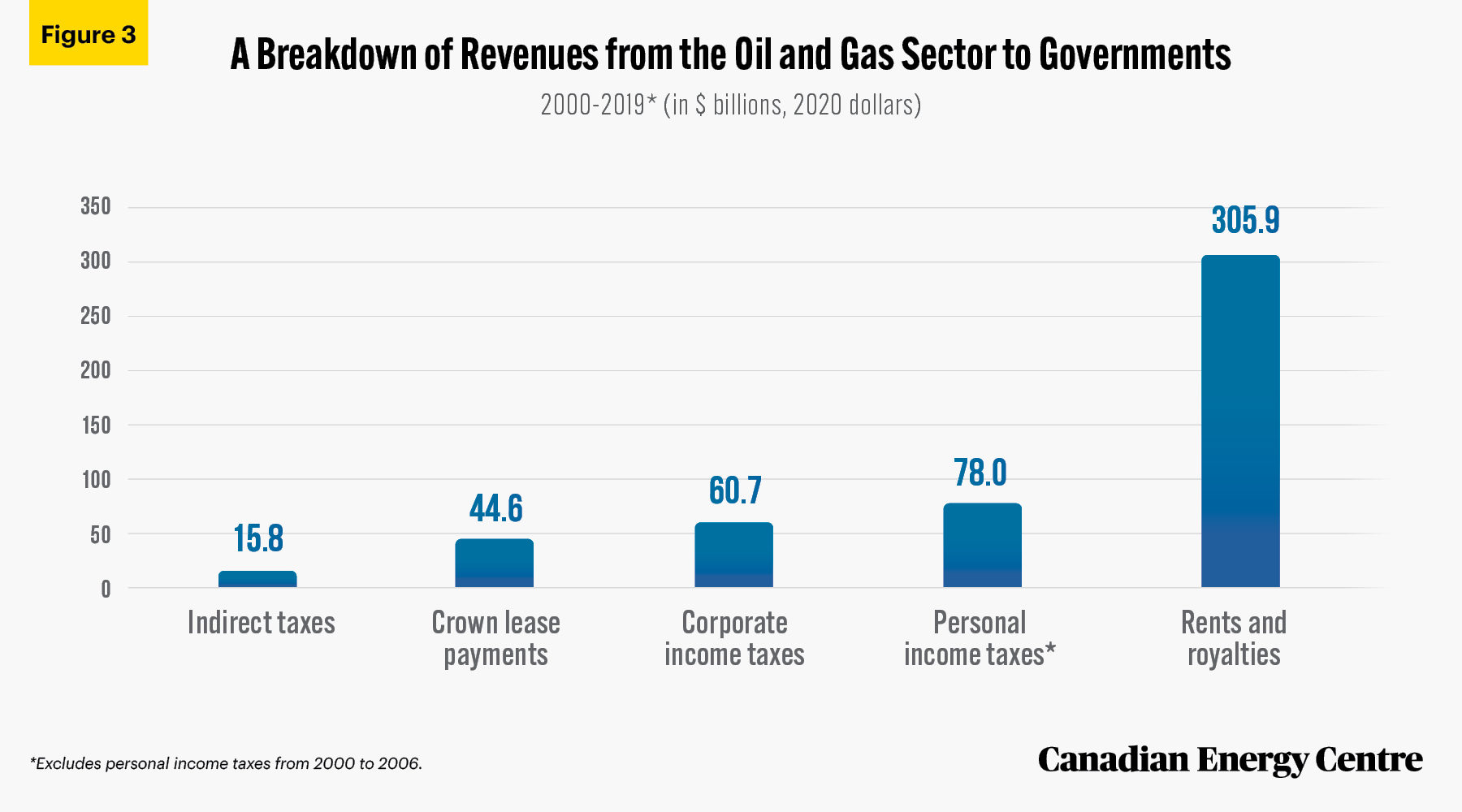

A Breakdown of Revenues from the Oil and Gas Sector

Just as the broad energy sector does, the oil and gas sector pays revenue to government in five main ways: indirect taxes, crown lease payments, personal incomes taxes, corporate income taxes, and rents and royalties (see Figure 3).

Indirect taxes: $15.8 billion

The Canadian oil and gas sector pays indirect taxes annually as a result of its activities. Those indirect taxes include federal and provincial sales taxes, federal and provincial gas taxes, federal excise taxes, federal import duties, and others.

Between 2000 and 2019, Canada’s energy sector paid $15.8 billion, an average of $790 million per year in indirect taxes to the federal government, the provinces, and municipalities.

Crown lease payments: $44.6 billion

The Canadian oil and gas sector is almost the sole contributor of the crown lease payments that accrue to governments. Between 2000 and 2019, the Canadian oil and gas sector made $44.6 billion, or an average of $2.2 billion per year, in crown lease payments to provincial governments.

Federal and provincial corporate incomes taxes: $60.7 billion

Between 2000 and 2019, the oil and gas sector paid federal and provincial corporate income taxes of $60.7 billion, or $3 billion per year.

Of that $60.7 billion, $38.7 billion was paid in federal corporate income taxes and $22 billion in provincial corporate income taxes.

Federal and provincial personal income taxes: $78 billion

Between 2007 and 2019, Canadians employed in the oil and gas sector paid $78 billion, or $6 billion per year, in federal and provincial income taxes on salaries, wages, and commissions. Note that this figure does not include federal and provincial personal income tax collected from the sector between 2000 and 2006, as those data are not available from Statistics Canada at this time.

Of that $78 billion, federal personal income tax revenues were $48.2 billion and provincial personal income tax revenues were $29.8 billion.

Rents and royalties: $305.9 billion

Canada’s oil and gas sector pays rents and royalties to provincial governments on the production of natural resources such as conventional oil, natural gas, and oil sands.

Between 2000 and 2019, the oil and gas sector paid $305.9 billion, or an average of $15.3 billion per year, in rents and royalties to provincial governments.

Sources: Statistics Canada, 2021 a, b, d, e, f, g; and CAPP, 2021.

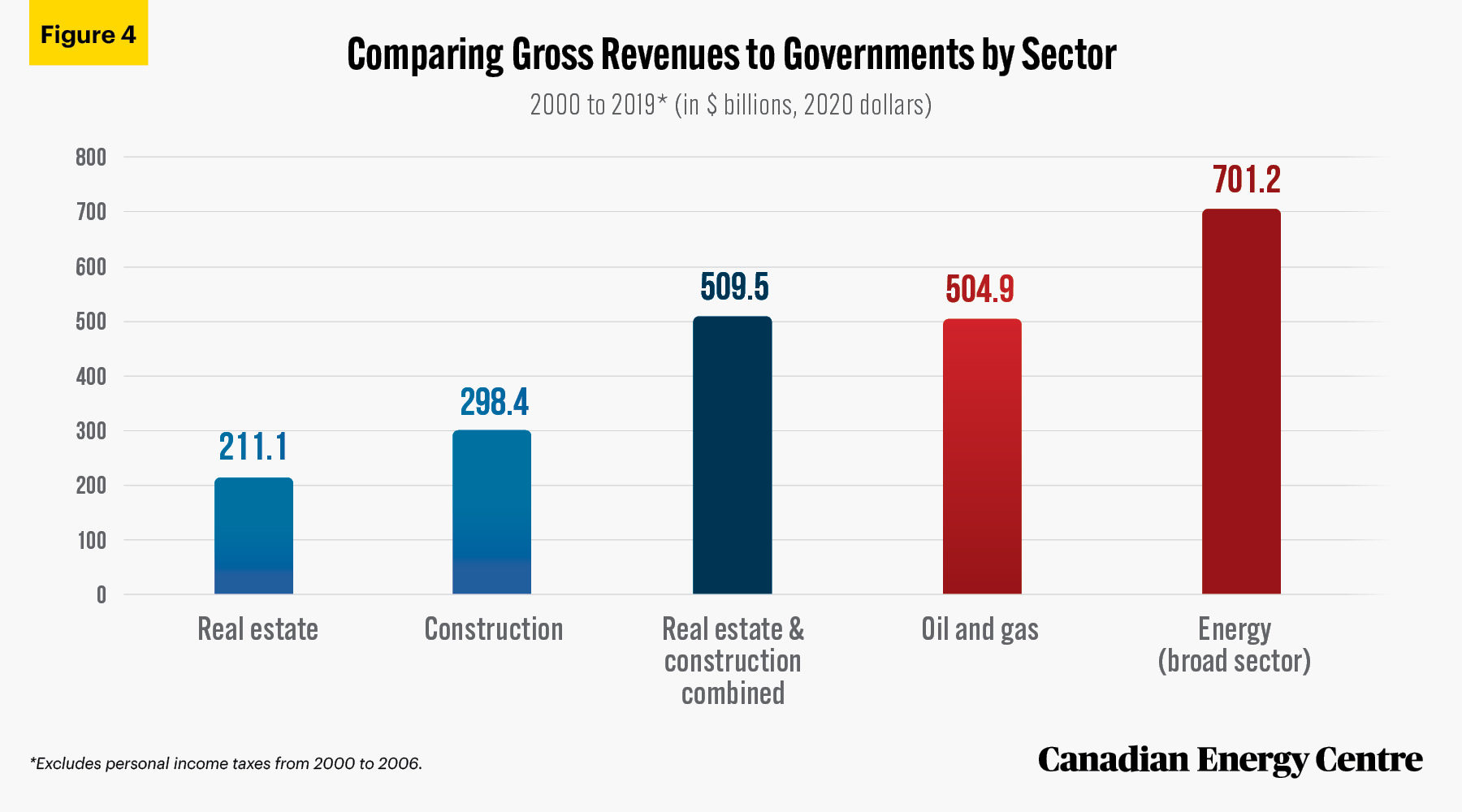

Revenue Comparisons with other Key Sectors

The gross revenue contributions of the oil and gas sector ($504.9 billion) and the broader energy sector ($701.2 billion) between 2000 and 2019 (see Figure 4) are significantly higher than other key sectors such as construction (see Appendix D: Construction Sector Gross

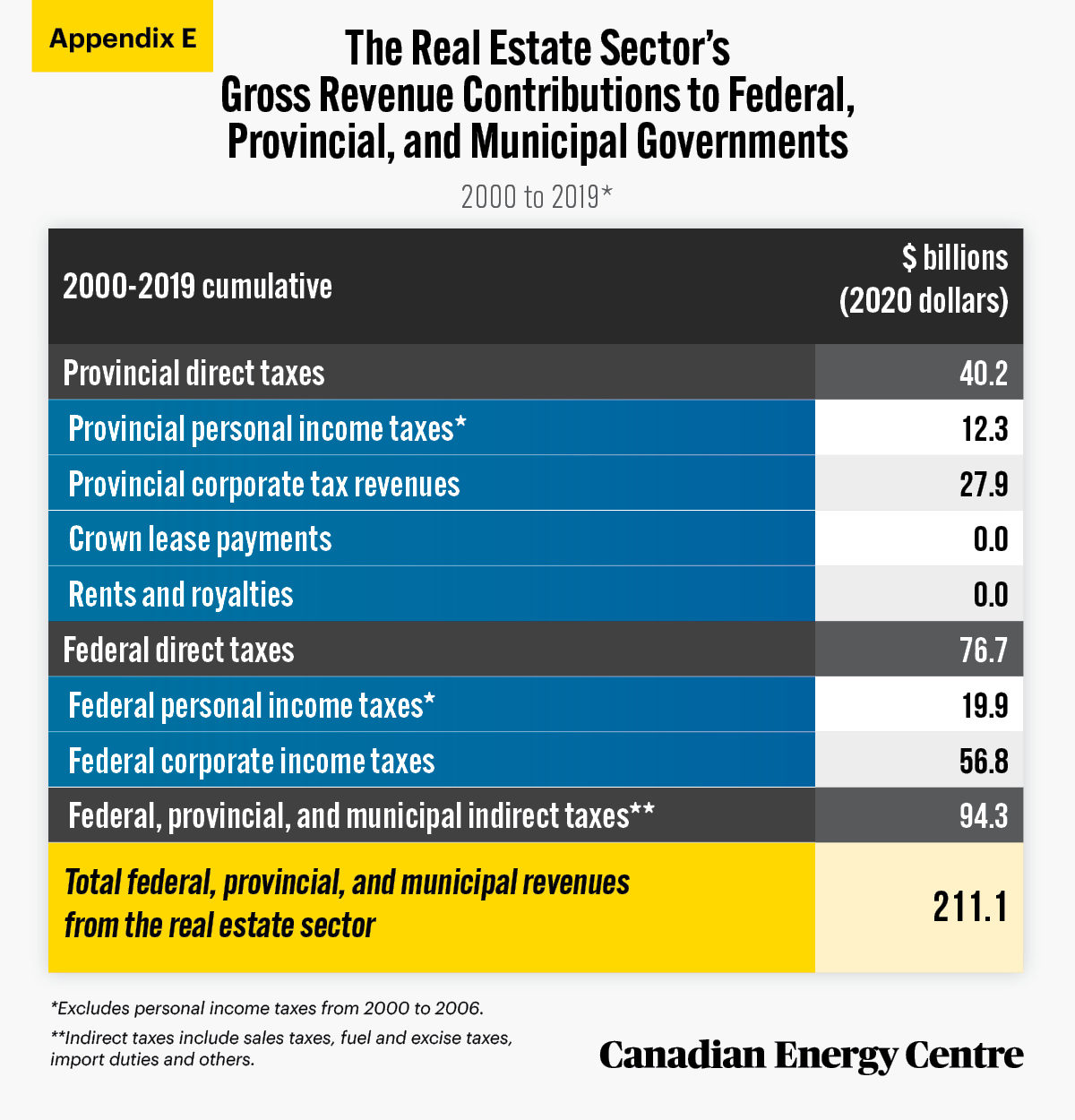

Revenues) and real estate (see Appendix E: Real Estate Sector Gross Revenues).

Between 2000 and 2019, revenues from those sectors were as follows:

- Real estate: $211.1 billion;

- Construction: $298.4 billion;

- Oil and gas: $504.9 billion; and

- Energy (broad sector): $701.2 billion.

Of note, the combined revenues of the real estate and construction sectors ($509.5 billion) was marginally higher than revenues from the oil and gas sector alone ($504.9 billion)—just $4.6 billion more—between 2000 and 2019 inclusive.

Sources: Statistics Canada, 2021 a, b, d, e, f, g; and CAPP, 2021.

Tracking energy revenues over two decades

Figure 5 compares the revenues between 2000 and 2019 by sector: energy, construction and real estate. The broad, overall energy sector has been the biggest contributor to government revenues in every year, ranging from a low of $21.9 billion in 2002 to a high of $54.2 billion in 2008. In the most recent year of available data (2019), the energy sector contributed $29.6 billion to federal, provincial, and municipal governments.

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

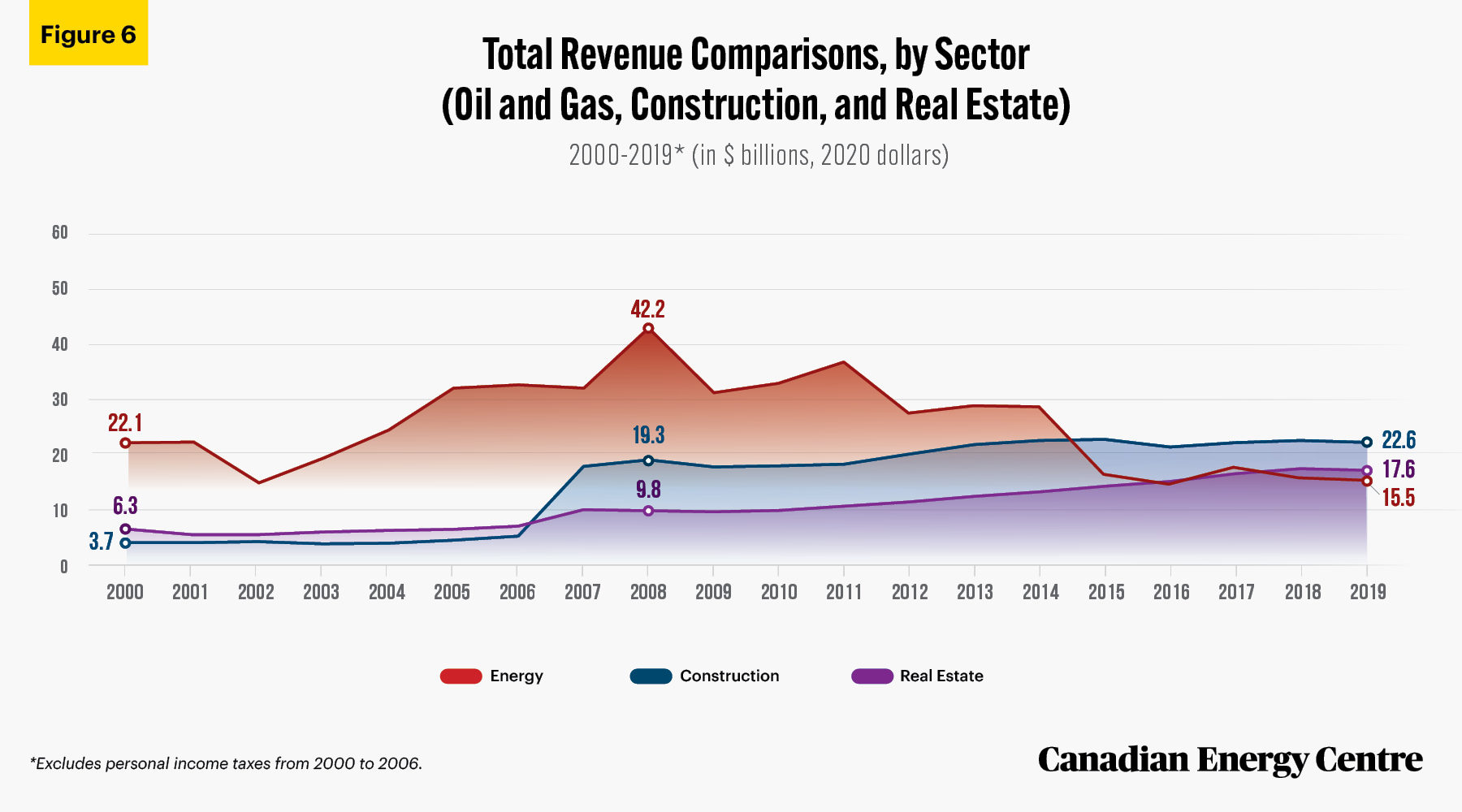

Tracking oil and gas revenues over two decades

Figure 6 compares the revenues of the narrower oil and gas sector (which is part of the broad energy sector) with the construction and real estate sectors between 2000 and 2019.

Of the three industries, the oil and gas sector was the biggest contributor to federal, provincial, and municipal government revenues every year until 2015, supplying as much as $42.2 billion in 2008 with a low of $14.8 billion recorded in 2016.

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

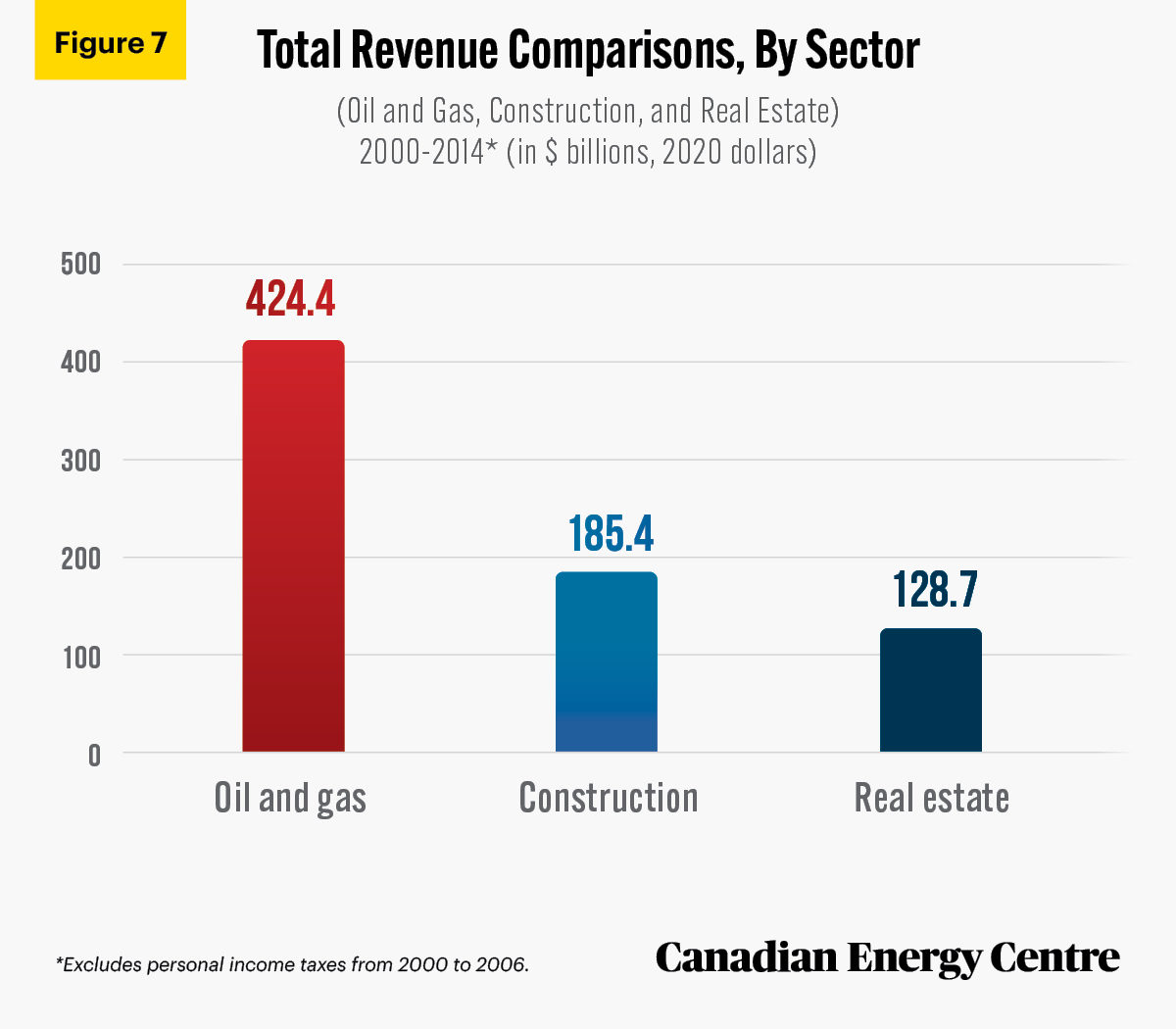

Breakdowns: 2000 to 2014 and 2015 to 2019

Between 2000 and 2014, the oil and gas sector contributed $424.4 billion to federal, provincial, and municipal governments, while construction contributed $185.4 billion and real estate contributed $128.7 billion (see Figure 7).

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

Between 2015 and 2019, the construction sector contributed $113 billion, with real estate contributing $82.4 billion, and oil and gas contributing $80.5 billion (see Figure 8).

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

Conclusion

The broad energy sector generally, and the oil and gas sector specifically, have made a significant contribution to federal, provincial, and municipal government coffers over the past two decades.

A conservative estimate of the gross revenues that Canada’s energy sector has paid to those three levels of government between 2000 and 2019 is $701.2 billion, an average of $35 billion per year.

The gross revenues contributed by the oil and gas sector alone ($504.9 billion) between 2000 and 2019 are significantly higher than those from other key sectors such as construction and real estate.

Appendices

Appendix A: Explaining gross revenues

Gross revenues from the broad energy sector and the narrower oil and gas sector are composed of direct and indirect taxes, royalties, and crown lease payments made annually to federal, provincial, and municipal governments.

They include:

- Federal and provincial personal income taxes or direct taxes from persons paid by employees who work within Canada’s oil and gas sector and the broader energy sector;

- Federal and provincial corporate income taxes or direct taxes from corporations paid by corporations and business enterprises in Canada’s oil and gas sector and the broader energy sector;

- Federal, provincial, and municipal indirect taxes on production and products, such as GST, excise taxes, duties, import taxes, gasoline and motive fuel taxes, and others paid by Canada’s oil and gas sector and the broader energy sector;

- Rents and royalties on the production of conventional oil and gas, oil sands, and hydro paid by Canada’s oil and gas sector and broader energy sector; and

- Crown lease payments for the leasing of rights that enable companies to explore for and develop petroleum and natural gas resources.

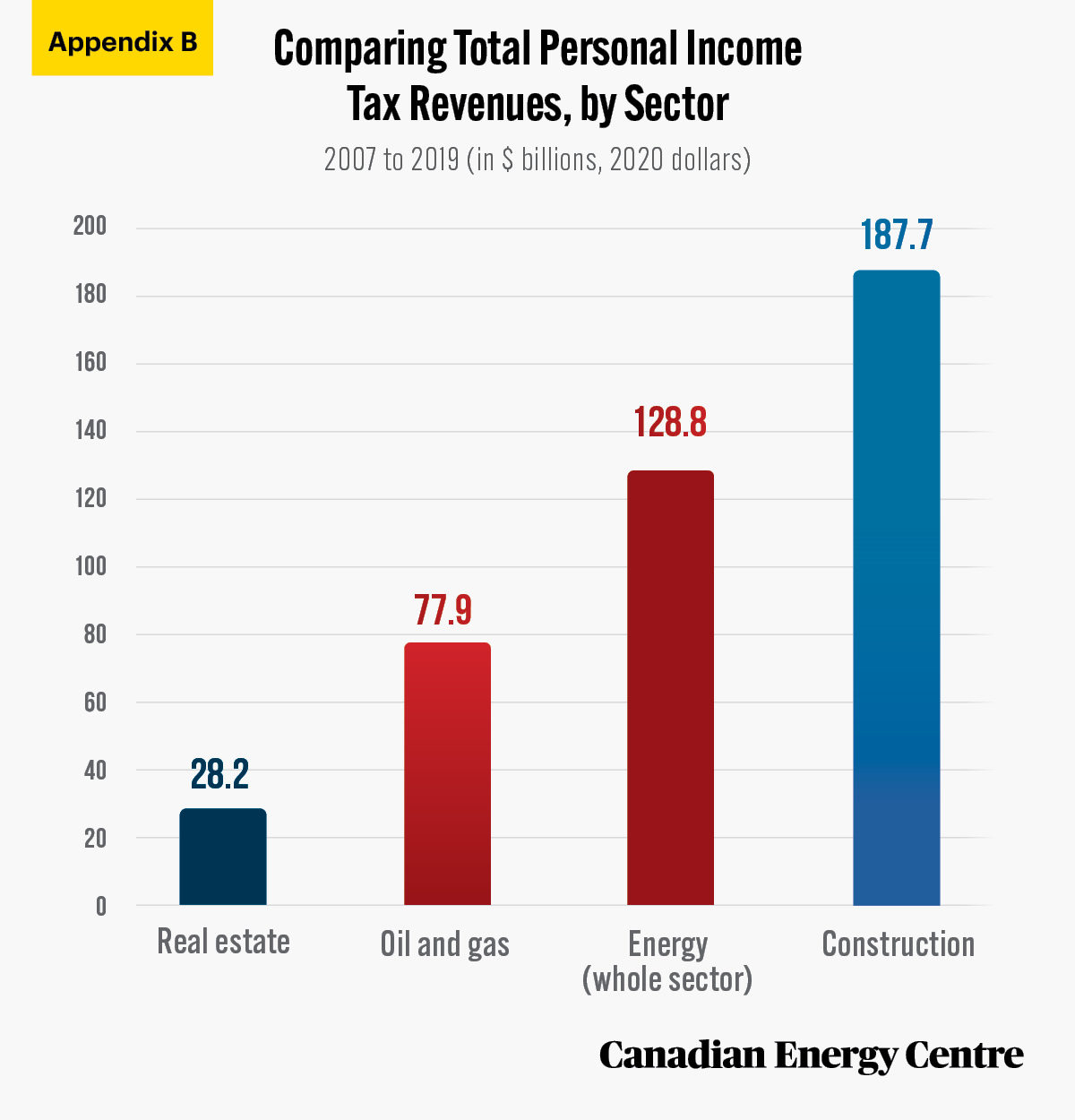

Appendix B: Personal income tax revenue comparisons

Between 2007 and 2019, direct personal income tax revenues (to the provincial and federal governments) from the various sectors were:

- Real estate: $28.2 billion

- Oil and gas: $77.9 billion

- Energy: $128.8 billion

- Construction: $187.7 billion

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

Appendix C: Corporate income tax revenue comparisons

Between 2007 and 2019, direct corporate income tax revenues (to the provincial and federal governments) from the various sectors were:

- Oil and gas: $60.7 billion

- Real estate: $84.7 billion

- Construction: $86.1 billion

- Energy (broad): $127.7 billion

Sources: Statistics Canada, 2021 (a, b, d, e, f, g) and CAPP, 2021.

Appendix D and E: Gross revenues from the construction and real estate sectors

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

Sources: Statistics Canada, 2021 a, b, d, e, f, g and CAPP, 2021.

References (as of July 22, 2021)

Canadian Association of Petroleum Producers (2021). CAPP Statistical Handbook for Canada’s Upstream Petroleum Industry. <https://bit.ly/36LFHR3>.

Finance Canada (2021a). Budget 2021. <https://bit.ly/3eEJwdU>.

Finance Canada (2021b). Fiscal Reference Tables. <https://bit.ly/3xk12ui>.

Statistics Canada (2021a). Table 10-10-0016-01: Canadian Government Finance Statistics for the Federal Government. <https://bit.ly/2GPmmDt>.

Statistics Canada (2021b). Table 10-10-0017-01: Canadian Government Finance Statistics for the Provincial and Territorial Governments. <https://bit.ly/3lwJhCI>.

Statistics Canada (2021c). Table 33-10-0006-01: Financial and Taxation Statistics for Enterprises, by Industry Type.<https://bit.ly/33Mkzba>.

Statistics Canada (2021d). Financial and Taxation Statistics for Enterprises, by Industry Type (x 1,000,000). Custom tabulation.

Statistics Canada (2021e). T1 Family File of the Centre for Income and Socio-Economic Well-Being. Annual Income Estimates for Census Families and Individuals (T1 Family File). Custom Tabulation.

Statistics Canada (2021f). Table 11-10-0073-01: Wages, Salaries and Commissions of Tax Filers Aged 15 years and over by Main Industry Sector and Sex. <https://bit.ly/2SEsO2X>.

CEC Research Briefs

Canadian Energy Centre (CEC) Research Briefs are contextual explanations of data as they relate to Canadian energy. They are statistical analyses released periodically to provide context on energy issues for investors, policymakers and the public. The source of profiled data depends on the specific issue. All percentages in this report are calculated from the original data, which can run to multiple decimal points. They are not calculated using the rounded figures that may appear in charts and in the text, which are more reader friendly. Thus, calculations made from the rounded figures (and not the more precise source data) will differ from the more statistically precise percentages we arrive at using the original data sources.

About the authors

This CEC Research Brief was compiled by Lennie Kaplan, Chief Research Analyst at the Canadian Energy Centre and Mark Milke, Executive Director of Research for the Canadian Energy Centre.

Acknowledgments

The authors and the Canadian Energy Centre would like to thank and acknowledge the assistance of Philip Cross for his review of the initial data for this paper.

Creative Commons Copyright

Research and data from the Canadian Energy Centre (CEC) is available for public usage under creative commons copyright terms with attribution to the Canadian Energy Centre. Attribution and specific restrictions on usage including non-commercial use only and no changes to material should follow guidelines enunciated by Creative Commons here: AttributionNonCommercial-NoDerivs CC BY-NC-ND.

Photo Credits

Dr. Pepper Scott, Shaun Undem, Anita Starzycka, Ave Calvar Martinez, Munir777, and Vardan Sevan

Share This:

COMMENTARY: Taxes and Regulations Will Increase the Cost of Producing New Energy In Alberta, Making it Less Competitive Than the US – Jack Mintz