CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

The opponents of oil have done everything they can think of to precipitate the permanent decline of this essential industry.

It isn’t working very well, at least not yet. While the critics of fossil fuels have had some success in western countries at reducing market access and supply, on a global basis none of these efforts have materially impacted demand.

A June 24th Reuters article titled “Reducing oil use to meet climate targets is tougher than cutting supply” tells the story. “Governments around the world have been slow to take uncomfortable decisions to persuade consumers to cut energy consumption to help achieve climate targets, often because consumers are not ready to pay up or compromise their lifestyles.”

Citing the International Energy Agency’s recent report that stated the development of new fossil fuels supplies must stop immediately, the article quoted IEA boss Fatih Birol who said, “Consumer behavior needs to change as a result of government steps.” Reuters continued, “Birol said the IEA has over 400 milestones that need to happen to achieve net zero targets by 2050 and 95% of those milestones should be driven by changes in demand, not supply.”

With the oil industry being the top stock market performer this year, it’s appropriate to review the ESG investment phenomenon. We’ve been assured this is a powerful tool to use money and capital markets to force oil, gas, and coal producers to change their behavior or do something else.

ESG started with the fossil fuel divestment movement when it became morally reprehensible to invest in coal, oil or gas companies. The early advocates were on university campuses where students tried to force university endowment funds to dump fossil fuel stocks.

Public and private sector pension funds were next, and the pressure is relentless. Corporate Knights, a website that promotes “Clean Capitalism”, continued on June 24, 2021, with an article titled, “Why are Canadian pensions risking our future by funding fossil fuel expansion?” which will surely result in “…catastrophic climate change. “

Then the financial sector got involved by introducing climate risk into investment decisions. In 2017 Michael Bloomberg and Mark Carney were the driving forces behind the Task Force on Climate-Related Financial Disclosures (TCFC). The right thing to do for responsible corporate governance was to acknowledge that large scale decarbonization of the future energy complex or severe weather events could have a material impact on a company’s prospects. This should be included in corporate planning and disclosure. TCFC was quickly endorsed by many institutional investors.

This morphed into today’s ESG investing; Environmental, Social and Governance. ESG covers climate change and all the other things that things modern corporations should pursue such as diversity and gender equity. While profits remain important, companies must do good or be seen as doing good.

And fossil fuels are bad. Starting with climate activists then expanding to ordinary investors, there has been growing pressure to support ESG investing. Because fossil fuels have joined tobacco, alcohol, gambling, sex, and defense contractors as the business sectors that the morally enlightened should either avoid or thoroughly explore before investing.

I have spent decades as a senior executive with TSX-listed oil service companies travelling to the financial centers of North America trying to persuade banks and institutional investors to provide us with expansion capital. Vancouver, Montreal, Toronto, New York, Boston, Chicago, San Francisco, Houston. I have two lasting observations.

The first is that none of the people I dealt with appeared to have chosen a career in financial services as an outlet for their inherent social altruism. It seemed to be more about making a lot of money.

The second is that the senior executives leading these firms were the best salespeople I have ever met. Big bucks attract the best and brightest.

In the past few years there have been many headlines about banks and institutional investors declaring they would no longer provide financial support for certain fossil fuel developments. It started with big European banks announcing that they would quit funding new coal or oil sands projects. This has expanded to include a growing array of institutional investors that say they will decline providing financial support for fossil fuel developers that are not adjusting their business and behavior to the climate change challenge.

In the last year, many of the bigger oil producers have changed their public disclosures and corporate strategies. Legacy global supermajors Shell and BP led the way in 2020 with restated mandates to move from oil into other forms of energy. Many large producers have publicly endorsed the net zero by 2050 pledge, although the honest ones admit they have no idea how they will achieve it.

Recent events affecting Shell in Dutch courts and the annual shareholder meetings of ExxonMobil and Chevron in the US could leave many with the impression that public concerns about climate change and ESG investing is accelerating the energy transition away from fossil fuels.

But for capital markets, it is still primarily about money. The Globe and Mail publishes the performance of major TSX indexes at https://www.theglobeandmail.com/investing/markets/indices/. Following are a few selected TSX indexes for the past ten years, and how they have performed.

TSCX TSX Composite Index

The broader market has delivered consistent, but choppy, growth for the past 10 years. The inclusion of Canada’s large oil and gas industry dragged this index down in 2015 and 2016. But $1,000 invested in the TSX composite index in July of 2011 would be worth $1,563 today. Even at the depths of the pandemic market correction last year, your original investment was still in the black.

TXOE Oil & Gas EW Index

Woof woof. The oil and gas sector has been a dog by any measure since late 2014 when oil prices collapsed and the North American shale gas boom tanked natural gas prices. Using this data, $1,000 invested in the stocks in this index ten years ago would be worth only $582 today, and that’s after a big recovery. As recently as last October your $1,000 had fallen to only $317. Lectures by investors about poor management are just noise. The real problem has been commodity prices. In 2014 WTI peaked at US$105.79 for the month of June and the AECO gas averaged C$5.20/GJ in February. Similar figures for April 2020 for WTI were US$16.55 and $0.55 for AECO gas in June 2019. Ouch. And this index only contains the four largest producers (Suncor, Imperial, CNRL, Cenovus) plus the four biggest pipeline operators (Pembina, TC, Enbridge, Inter Pipeline). Their valuations have held up well compared to the smaller E&P companies and the oil service sector. When I wrote my book (referenced at the end of this article) I looked at the market value of 20 independent E&P companies with annual revenues exceeding $300 million from their peak in 2014 to January 2019. As a group they were down 76% with a total market cap loss of $160 billion.

TXBA TSX Composite Bank Index

The banks have been a steady source of equity growth and dividends. While this index only goes back to October of 2012, $1,000 invested then would be worth $2,002 today. One of the ways banks have been able to sustain earnings and investment returns is to loan less money to sectors like oil and gas when they are financially challenged. The banks in this index are included in the TSX Composite Index.

TXCT TSX Renewables & Clean Tech Index

The companies in this sector took a long time to gain traction. But since late 2019 the “renewables” and “clean tech” space has performed well. $1,000 invested in 2011 would be valued at $2,160 today. But this is down 11% from January of this year, the ten-year peak.

TTTK TSX Information Tech Capped Index

The steady money maker thanks to the IT revolution of the last decade. $1,000 invested in the companies that comprise this index in July of 2011 would be worth $7,137 in June of 2021. Looking back, avoiding oil stocks and following this rapidly growing sector for the past ten years instead would have investing genius.

Much lower and highly volatile commodity prices since 2014 have made it much easier for banks and institutional investors to publicly adopt ESG principles, avoid the oil and gas industry, attract capital from climate-concerned investors and shareholders, and continue to deliver growing profits and returns. For broad-based funds and banks (which by nature are multi-sector generalists), not investing in oil and gas for the past five years has had much more to do with economic necessity than moral persuasion.

Along the way, the marketing wizards concluded that signaling their ESG credentials was a good way to keep new capital coming in and/or maintain current shareholders or investors.

There are two elements of the ESG investing story that run contrary to what is often reported.

The first is that oil and gas prices are not only out of the dumpster, but many years of low capital investment and continued demand growth have completely changed global energy markets. Now people are talking about $100 oil, not $20.

If ESG investing has had any impact at all, restricting capital has ensured companies have had less to spend on reserve development which has helped contribute to what many believe is a pending supply shortage. While is seems unlikely, is it possible fund managers were smart enough to predict or influence this outcome?

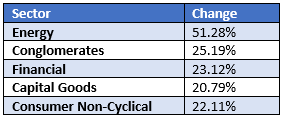

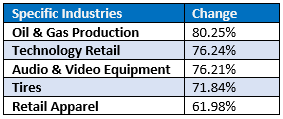

Website https://csimarket.com/ publishes reports on the best and worst performing major economic sectors and specific industries. As of June 27, 2021, here is the year-to-date performance.

Equity markets are enjoying steady growth this year thanks to the end of pandemic lockdowns, pent up consumer demand, reopening of businesses, and massive stimulus spending by western governments.

The other is the quest for sustained yield or dividends. One thing oil and gas has proven when commodity prices are higher is that well managed producers are cash machines.

Research firm Rystad Energy released a report on June 23 titled with press release titled, “A record cash flow is brewing for the world’s public E&Ps in 2021 as US shale delvers super-profits”. Rystad reports, “Their combined FCF (Free Cash Flow before financing or hedging) is expected to surge to US$348 billion this year, with the previous high being US$311 billion back in 2008.”

If you read the fine print in the public pronouncements on both sides of the ESG trade, the common term is “capital discipline”. This means producers are no longer pursuing their historic goal of growing production to meet future demand growth.

In fact, the question is being raised if enough capital has been invested in the past five years to offset future reservoir decline rates. If demand doesn’t decline, a shortage is inevitable.

And whatever the long-term goal of ESG investors is, those who hold oil stocks want to see sustained or increased dividends as much as reserve growth or an entirely new business model. At least for now.

Recent events with ExxonMobil and Chevron reveal that 2021 ESG investing includes owning oil and gas stocks so long as management says and does the right things. Right now, E&P equities are becoming increasingly attractive as both the yield and the underlying share value are increasing.

Everyone should decide where they want to invest when the world returns to normal. Normal includes government stimulative spending being replaced by tax increases, the end of pent-up consumer demand after a year of pandemic lockups, and the developing world continuing to grow its population, GDP, and energy consumption.

The performance of the western economy has been supported by years of uber-low interest rates and “quantitative easing”. Markets shuddered only a week ago when the US Federal Reserve publicly speculated about tapering quantitative easing sooner than previously announced because of rising inflation.

Equity markets love it when governments print and spend money. At least in the short term, which is the 21st century investment time horizon.

What stocks do you want to own when the party ends? The stuff people can’t live without, like resources. If fossil fuels remain profitable while other sectors of the economy flatten or contract, will banks and equity investors remain as ESG focused as they have been in the past few years? Can they afford to be?

As for oil, whatever we’re told we’re supposed to do about decarbonization, the reality is that non-OECD producers from Eastern Europe, the Middle East, Africa, Asia and South America have the capability of filling any supply shortages incurred by the influence of ESG investing on E&Ps headquartered in the EU or North America.

What does ESG investing mean for the Canadian oilpatch in the short and medium term?

Thanks to higher prices it is evolving into neutral or positive.

Producers that are saying and doing the right things are again able to raise money. With positive cash flow from existing production, doors to new debt and equity will surely open. While the public narrative is that investors have been avoiding the sector, the reality is that the industry was a lousy investment for many years. Companies without free positive cash flow can’t borrow money no matter what business they are in.

ESG capital for energy alternatives and decarbonization of the existing oil and gas supply chain is fantastic if that’s what investors and policy makers want. This is a source capital than never used to exist. This funding will be much more predictable and easier to access for entrepreneurs with good ideas than more government programs.

The long term, however, looks murkier.

The quest for yield and reduced capital spending will create problems. Reserve replacement is a key component of staying in the oil business. Looking to the future, before the recent board changes ExxonMobil was planning to increase production. While the new direction as reflected by new board members is said to be good for mankind from an emissions perspective – and higher prices and dividends are certainly good for shareholders – really high oil prices have proven to negatively affect humanity in many other ways. Like the cost of food.

The elephant in the room remains Asset Retirement Obligations, or ARO. This is rarely mentioned in the media except to repeat somebody’s complaints. But ARO is becoming more important as investors select the companies they choose to support. The oil and gas industry is expected to clean up after itself. All producers carry ARO liabilities on their balance sheets. Even if oil is ultimately doomed in the long term, the world will be a better place if E&P companies are left with enough cash to ensure cleaning up their “stranded assets” doesn’t become somebody else’s problem.

Will the current crop of ESG shareholders still be around when the time comes to properly shutter expired or worthless fossil fuel assets? If E&P companies switch to renewables, can they develop new clean energy sources and still generate enough cash flow to pay dividends and decommission their legacy assets? Under the environmental rules of 10, 20 and 30 years from now?

This is yet another reason to include oil and gas producers in the energy transition, not squeeze them out.

As the first generation of wind and solar renewable electricity assets reaches the end of their practical service life, the ARO issue is emerging in this sector. Hopefully, the playing field will be level as that industry matures. Developing renewables properly on a full cycle basis including ARO will increase the cost. Can we be confident ESG investors will be equally rigorous in their expectations of renewable energy producers?

ESG investing and the future of oil. As with all aspects of climate change, the real issues are much more complex than politics, virtue signaling and the daily news.

David Yager is an oil service executive, energy policy analyst, oil writer and author of From Miracle to Menace – Alberta, A Carbon Story. More at www.miracletomenace.ca

Share This: