CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

On March 25, the 21st century version of the Supreme Court of Canada delivered its much-hyped ruling about the multi-province challenge of the legality of the federal government’s national carbon tax.

In a split decision that went 6/3, the court relied on the Peace, Order and Good Government provision of the Constitution, concluding that Ottawa was within its legal rights to impose such a tax because it was in the public interest.

But as is increasingly the case when today’s Supreme Court interprets the Constitution, the written decision includes language more about political and social policy than the Constitution itself.

The 400-page document included the words, “This matter is critical to our response to an existential threat to human life in Canada and around the world. All parties to this proceeding agree that climate change is an existential challenge. It is a threat of the highest order to the country, and indeed to the world. The undisputed existence of a threat to the future of humanity cannot be ignored.”

There is, of course, no reference to protecting all humanity or the rest of the world in the Canadian Constitution, a law that applies to only 0.05% of the planet’s population.

Rulings outside of the letter of the law are not new.

In court challenges to federal approvals for the Northern Gateway and Trans Mountain pipelines undertaken by First Nations and environmentalists, the judges relied on Section 35 of the 1982 Constitution Act which affirms protection for existing Aboriginal rights and treaties.

In overturning the pipeline approvals, the courts’ written decisions included the words “duty to consult” even through they don’t appear in the Constitution. Further, the regulatory review and approval process had already included extensive consultation with everyone along the right-of-way. Otherwise, the National Energy Board and federal government could not have granted approval.

Whether or not the Supreme Court should be delving into politics and social justice is a serious concern, particularly for those on the wrong side of decisions like the foregoing.

But in the bigger picture, the oil and gas industry has been paying lots of taxes of one form or another for years. That Canadian carbon taxes will not actually change the chemical composition of the global atmosphere when giant emitters like China don’t participate is secondary to 21st century politics. Alberta and BC introduced carbon taxes which the industry has been paying since 2007.

Faced with the new environmental activist Joe Biden Democratic administration in the US, the American Petroleum Institute recently publicly endorsed some sort of carbon tax. Multiple big producers around the world are making pledges to “net zero by 2050” which will be driven by some manner of carbon taxes.

What is materially more important to oil and gas producers in the short term after six very challenging years is sufficient cash flow from existing production with which to pay carbon taxes and all the other costs of staying in business.

Fortunately, this critical aspect of the business looks greatly improved for 2021, at least on paper. Rising commodity prices, reduced costs and quick returns to higher production levels have made the macro-economic outlook for producers much better, particularly compared to last year.

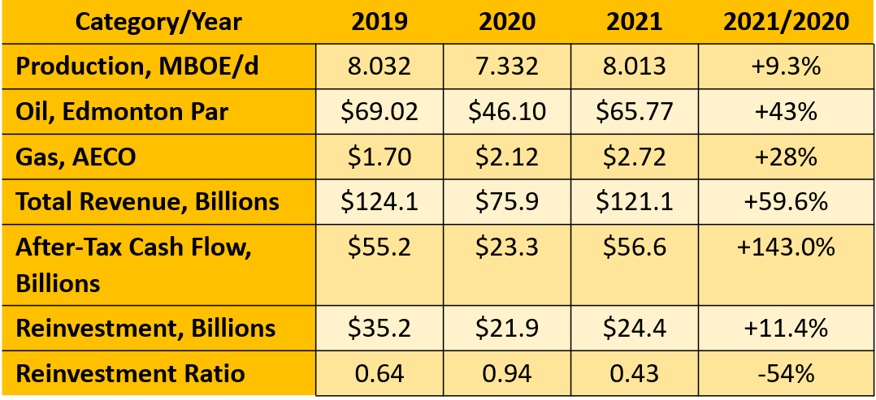

ARC Energy Research Institute publishes its weekly ARC Energy Charts, an overview of the upstream oil and gas producing sector. It includes trailing and forecast daily production, commodity prices, total revenue, after-tax cash flow (funds available for reinvestment once all costs and obligations are covered), reinvestment (capital) and the reinvestment ratio, how much of the cash flow is going back into the business in Canada. The following data is extracted from the March 22, 2021 edition.

The good news is that production volumes and prices have recovered. Estimated gas prices for 2021 are the highest since 2014, as is forecast after-tax cash flow.

This is a vast improvement for unemployed workers and underutilized oilfield service and supply companies. Because at least the producers have cash to spend. That wasn’t the case in 2020.

But that’s it for good news. The last major ingredient is confidence, and this remains under assault from multiple directions.

ARC’s data on reinvestment is determined primarily from disclosure by producers. At this stage just because they have more cash does not mean they intend to spend it. The reinvestment ratio, the lowest in 10 years of data by a large margin, shows that producers have different plans than picking up rigs and expanding their asset and production base. Right now is only at 0.43 for 2021. The average for the prior ten years was 1.18.

The confidence challenge is best demonstrated by the figures from 2014, the last really good year for everything. None of the cancelled pipelines – Keystone XL, Northern Gateway or Energy East – were dead yet. The Trans Mountain expansion was moving along as planned.

For that year, ARC data shows after-tax cash flow from production of $67 billion from only 6.530 MBOE/day. But the industry reinvested $80.7 billion, 135% of cash flow or a reinvestment ratio of 1.35. The extra capital came from debt, equity or inter-company transfers from domestic or international parent companies.

Investment capital was not leaving but pouring into Canada by the billions. It would be another year before Mark Carney and Michael Bloomberg invented the Task Force on Climate Disclosure, a foundation of today’s ESG investment movement.

Canada’s major exodus of capital began in 2016 and 2017 due to several factors. New climate focused governments were elected in BC, Alberta and Ottawa. Opposing new oil pipelines became a major force in all directions; west, south and east. The pipeline cancellations began in late 2015 with Keystone XL and continued through 2016 with Northern Gateway and 2017 for Energy East. International oil sands developers decided they wanted to do something else with their money and sold out.

Attractive new US corporate tax and depreciation rules under Donald Trump’s shameless pro-oil agenda made American investments look compelling by comparison. Bill C-69 made the approval of new pipelines appear daunting and unpredictable. Bill C-48 banned oil tankers from the nearest tidewater access to northern Alberta. Offshore exploration has been banned in various places around the world. Denying marine access for oil produced on land is unprecedented.

As the ESG phenomenon grew, so did significant pressure by capital providers to avoid investing in the fossil fuel sector entirely or put strict conditions of the acceptable behavior of the companies they chose to fund. Today, many of the bigger ESG-focused funds that hold E&P equities would rather see increased dividends than capital programs. On the debt side of the balance sheet, many producers are paying down debt after the near-death experience of negative or near-zero oil prices just under a year ago.

The collective impact of the foregoing has been a major decline in confidence that Canada is secure and a predictable place to invest.

The next big issue for producer confidence is the oil price itself. While the recovery in prices this year has been remarkable, it is propped up by significant supply management from the OPEC+ consortium. It was only a year ago that the biggest players – Saudi Arabia and Russia – were playing a very public game of chicken in what was certain to be wealth destroying race to the bottom of the barrel.

Common sense prevailed. Eleven months later the OPEC+ producers are still supporting oil prices by withholding over 7 million b/d from markets. US production is down 2 million b/d in the past year. The combination of the two is causing inventories to draw down globally as demand recovers.

After WTI peaked at US$66.02 on March 11, it began to soften because of delays in vaccinations and continued lockdowns and restrictions in many countries. Many borders remain closed and people are still forced to remain at home to the greatest degree possible. The temporary blockage of the Suez Canal caused prices to rise and perhaps reminded traders of the fragility of certain elements of the global oil supply chain.

It is totally reasonable for producers to be suspect about the foundations of current oil prices relative to the basics of supply and demand. There remains too much supply and demand has not fully recovered to 2019 levels. ARC’s cash flow forecast for 2021 is based on current oil prices and futures markets, both of which anticipate continued supply management by OPEC+. With three-quarters of the year ahead, this could be optimistic.

Data from the Energy Information Administration’s March 2021 short term oil outlook doesn’t see supply and demand coming into balance until the latter half of the year. Maybe longer depending on vaccinations and lockdowns.

The last confidence crusher is the May deadline to shut down Enbridge Line 5 which carries 540,000 b/d from Alberta to southern Ontario through the state of Michigan under the Mackinac Strait at the top of Lake Michigan. Michigan Governor Gretchen Whitmer warned Enbridge in November it had six months before the state would revoke its original permits granted in 1953 so this pipeline could take the shortest and lowest cost route from Alberta to Sarnia and southern Ontario.

In 1977 Alberta made the great horned owl its official bird. After the events of the last few years it should be changed to the black swan. Since 2010 the industry and the province have been forced to respond to multiple unplanned but significant events from a variety of sources.

Imagine how much things would improve if there was an outbreak of stability?

Website investopedia.com defines a black swan as, “….an unpredictable event that is beyond what is normally expected of a situation and has potentially severe consequences. Black swan events are characterized by their extreme rarity, severe impact, and the widespread insistence they were obvious in hindsight.”

The COVID-19 pandemic is a textbook example, a black swan event if there ever was one. Who put a global virus outbreak in their 2020 business plan? But after the pandemic lockdown, lots of voices emerged claiming to have warned somebody against such an event.

Shutting down an existing pipeline that would disrupt nearly 1/3 of Canada’s inter-provincial oil production after 68 years of safe and continuous oil production certainly falls into the black swan category. Who would have thought of that?

But for social or environmental reasons, shutting down flowing pipelines has now become a cause celebre; the ultimate act of decarbonizing 21st century civilization much more quickly and effectively than paying a few cents more for each liter of gasoline.

There were two black swan events in the US in 2010 which gave the American environmental movement a lot of ammunition, and impacted Canada much more than is commonly acknowledged. Michigan has not forgotten the regrettable rupture of Enbridge’s Line 6B pipeline which spilled a lot of heavy oil into the Kalamazoo River. Then there was BP’s massive Macondo offshore blowout in the Gulf of Mexico.

Should Michigan proceed, it will collapse the price of oil in Alberta and starve southern Ontario and Quebec of essential fuels and feedstock for transportation, chemical manufacturing and agriculture.

It used to require a war to disrupt supply chains in this order of magnitude. But it is a war of sorts among the most radical climate change activists and the rest of modern society.

The only good news about the Enbridge Line 5 threat is Ontario and Quebec have finally found a pipeline they love and aren’t prepared to live without.

The likelihood of this occurring is remote. But going back to 2010, all manner of major changes have occurred to the oil and gas industry that were considered highly improbable at the time. In 2011 Prime Minister Stephen Harper referred to the approval of Keystone XL as a “no brainer”.

If I were CEO of an E&P company on the western end of this pipeline in these unpredictable times, I might delay increasing the 2021 capital budget until well past Whitmer’s May deadline.

Nevertheless, the key ingredients of a meaningful recovery are in sight. Honest. Commodity prices and cash flow are higher. They just have to stay that way. Carbon taxes are a fact of life and the really high levies are years and multiple federal elections away. We’ll see how that unfolds as governments and citizens grapple with the aftermath of the huge public debt and economic devastation resulting from the pandemic.

Three pipelines that will improve everything are under construction: Trans Mountain, Enbridge Line 3 replacement and Coastal Gas Link. If completed they will significantly underpin many years of steady production, capital investment and growth.

For now, confidence is returning but more help is a required. A few simple broad public and government commitments are all that is necessary to put this industry on positive path forward.

More people should accept that fossil fuels will be with us for years and quit claiming otherwise. A little education and more intelligent public debate would be very helpful.

Canada is indeed an advanced and superior producer that is making major steps on emission reduction and ESG compliance.

As long as the rest of the world uses and needs oil and gas, the economic benefits of the domestic industry far outweigh the costs.

The country needs profitable resource-extraction industries and jobs to help pay its way out of the COVID debt disaster.

Add some confidence in the future along these lines, and the ‘patch could once again be an engaging and rewarding place to work.

David Yager is an oil service executive, energy policy analyst, oil writer and author of From Miracle to Menace – Alberta, A Carbon Story. More at www.miracletomenace.ca

Share This:

PERSPECTIVE: Why Youth Awareness and Education About Energy Are So Important to Canada