CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

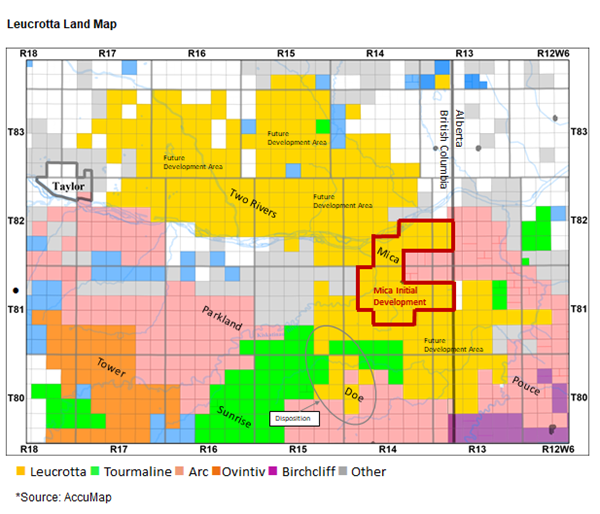

Leucrotta Land Map

THIS PRESS RELEASE IS NOT FOR PUBLICATION OR DISSEMINATION IN THE UNITED STATES. FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF UNITED STATES SECURITIES LAW.

CALGARY, Alberta, March 15, 2021 (GLOBE NEWSWIRE) — Leucrotta Exploration Inc. (“Leucrotta” or the “Company”) (TSXV – LXE) is pleased to announce that it has entered into an agreement with a syndicate of underwriters for a $20.0 million bought deal financing (the “Financing“) by way of a short form prospectus offering. The Company will be conducting a concurrent non-brokered private placement of $2.0 million flow-through units of the Company. The Company has also entered into a definitive agreement with an Alberta based publicly traded oil and gas company in connection with disposition of its non-strategic lands (the “Asset Sale“) comprising 5% of Leucrotta’s Montney land base for an aggregate consideration of $30.0 million. The Company intends to use a portion of the combined proceeds from the Financing and the Asset Sale to advance the initiation of a Pad Development program in the High GOR (gas to oil ratio) Light Oil Window of the Lower Montney at Mica (the “Mica Project“). The acceleration of the Mica Project will transform Leucrotta into a high-growth pure play Montney entity with one of the largest contiguous positions in the Montney light oil window. The funding and expected debt capacity on successful drilling of the Mica Project is expected to create cash flow sustainability, and management estimates that the Mica Project could increase Leucrotta’s production to 15,000 – 20,000 boepd within three years.

Leucrotta Land Map:

https://www.globenewswire.com/NewsRoom/AttachmentNg/c65e7e88-0197-40e9-a261-448b8261122b

*Source: AccuMap

Rob Zakresky, Chief Executive Officer and President of Leucrotta comments, “We are excited to kick-off our Mica Pad Development drilling program with years of drilling ahead of us. Leucrotta has captured and delineated an enormous resource in the Montney and are thrilled to be in the financial position to surface that value for our shareholders.”

Strategic Rationale

The New Funding Kickstarts the Mica Development while Minimizing Dilution

- The Asset Sale helps minimize dilution while only disposing of approximately 5% of the Company’s Montney acreage;

- Added equity allows Leucrotta to be debt-free well into 2022 when production is estimated by management to be materially higher;

- Exit 2021 production is expected to exceed 4,500 boepd (27% oil and condensate) with approximately $20.0 million cash remaining; and

- Future capital can be accessed by adding a prudent amount of debt as cash flow grows.

Shareholders Remain Exposed to Large Resource in Place while Generating Cash Flow

The Mica Project is planned to ramp production to over 30,000 boepd exploiting only 30 sections of land in only 1 of 3 Montney zones. However, Leucrotta owns over 240 net sections of land where the Montney averages 300 metres thick with numerous potential benches and has 17.8 billion bbls of OOIP and 17.2 tcf of OGIP. Value for shareholders can be realized well beyond the Mica Project as:

- Additional Montney benches in the Basal and Upper at Mica (not included in initial Mica Project) to be production tested over next 12 months;

- Two Rivers Montney acreage north of the Peace River (140 net sections) located within the Light Oil Window have had encouraging initial results; and

- Technology continues to enhance economics of large resources such as the Montney High GOR Light Oil Window through longer wells (2400+m) and improved extreme limited entry completion technology resulting in increased recoveries.

Highly Economic Drilling Inventory in the Mica High GOR Light Oil Window

- On full pad development, new wells are expected to generate an IRR of greater than 100% and a payout of approximately one year based on commodity pricing of WTI USD$50.00/bbl; AECO CAD$2.25/GJ; FX 1.28 CAD/USD; and

- The production from the Mica Project is estimated to increase to over 30,000 boepd within 5-year time frame utilizing only 30 of the 100 sections of delineated lands (over 240 total Montney sections).

Mica Pad Development

The Mica Project is anticipated to start with an initial 3-4 well pad in 2021 using modern technology that will incorporate 2,400 metre horizontal laterals, the latest frac designs, and increased frac intensity. Wells will be produced through existing infrastructure and will be the basis for an accelerated development from 2022 forward. The Mica Project was modeled solely on the Lower Montney horizon, however, Leucrotta will production test both the Basal and Upper Montney horizons at Mica in 2021 to determine if the Company can enhance economics even further through a stacked development program.

The accelerated development (expanded Pad Development) is expected to take production to over 30,000 boepd and incorporate existing Leucrotta infrastructure, expanding current infrastructure and utilizing available third-party infrastructure where appropriate. Leucrotta estimates it will take approximately five years to reach its production targets.

The Mica Project has the following characteristics that will enhance economics and allow for ease of development:

- Initial Target (Lower Montney) contains light sweet oil (39-42 API) and sweet liquids-rich natural gas;

- Low water rates and high GORs limit artificial lift requirements;

- Egress in area is excellent with access to various competing pipelines for oil, gas and liquids;

- Proximity allows for access to various markets for gas and liquids including potential markets in Asia for LNG and NGLs;

- Surface access is excellent with lands being predominantly farm land with an established road system;

- Access to services is also very good given proximity to Dawson Creek, Fort St. John and Grand Prairie; and

- A significant portion of the initial infrastructure and field gathering system is already in place which will reduce infrastructure capital required.

Financing

Leucrotta has entered into an agreement with a syndicate of underwriters (the “Agreement“), co-led by Haywood Securities Inc., as sole bookrunner, and Echelon Wealth Partners Inc. (collectively, the “Underwriters“), pursuant to which the Underwriters have agreed to purchase for resale to the public, on a bought deal basis: (i) up to approximately 27.4 million units of the Company (“Units“) consisting of one common share in the capital of the Company (a “Common Share“) and 0.5 Common Share purchase warrants (each whole warrant, a “Warrant“) at a price of $0.73 (the “Offering Price“) per Unit for gross proceeds of approximately $20.0 million. The Warrants have an exercise price of $1.00 per Common Share and a term of two years from the closing date of the Financing (the “Financing Closing Date“).

The Underwriters have also been granted an unassignable option (the “Over-Allotment Option“), exercisable in whole or in part and from time to time, at any time until 30 days after the Financing Closing Date, to purchase from Leucrotta up to approximately 4.1 million additional Units at the Offering Price for additional gross proceeds of up to approximately $3.0 million. If the Over-Allotment Option is exercised by the Underwriters in full, aggregate gross proceeds of the Offering (including the Over-Allotment Option) will be approximately $23.0 million.

The Common Shares to be issued under the Financing will be distributed by way of a short form prospectus in each of the Provinces of Canada, other than Québec. A portion of the Financing will be conducted on a private placement basis in the United States via Rule 144A to Qualified Institutional Buyers only under the U.S. Securities Act of 1933, as amended and certain other jurisdictions outside of Canada as the Company and the Underwriters may agree on a private placement basis. No prospectus will be required to be filed in any jurisdiction other than the Canadian jurisdictions.

The Company will be conducting a concurrent non-brokered management private placement of up to 2.0 million units of the Company (“Flow-Through Units“) consisting of one Common Share to be issued on a flow-through basis in respect of Canadian Development Expenses (“CDE“) under the Income Tax Act (Canada) (a “Flow-Through Share“) and one Flow-Through Share purchase warrant (a “Flow-Through Warrant“) at a price of $0.75 per Flow-Through Unit for gross proceeds of up to $1.5 million. The Flow-Through Warrants have an exercise price of $1.00 per Flow-Through Share and a term of three years from the date of issuance.

The Financing is expected to close on or about March 31, 2021 and is subject to certain conditions including, but not limited to, the receipt of all necessary approvals, including the approval of the TSX Venture Exchange.

Grant of Stock Options

The board of directors of the Company has approved the granting of incentive stock options (“Options“) under its stock option plan to certain of its directors and officers to acquire up to an aggregate of 4.0 million Common Shares of the Company. The Options are exercisable for a period of five years at a price of $0.78 per Common Share and vest over three years.

Following the grant of the Options, Leucrotta will have a total of 17.6 million Options outstanding. Leucrotta’s share based incentive plans limit the total number of Common Shares underlying the outstanding stock options and performance warrants to no more than 10% of the issued and outstanding Common Shares. As of the date of this press release, the total number of Common Shares underlying the outstanding stock options represents about 8.8% of the issued and outstanding Common Shares.

Asset Sale

Leucrotta signed a definitive agreement to sell 10.25 sections of Montney lands including approximately 375 boepd of production for a purchase price of $30.0 million. The Asset Sale is scheduled to close on or around April 1, 2021. For Leucrotta, the lands were assessed to be non-strategic as they:

- were not conducive to long well development given proximity to other companies;

- are located in the wet gas window with Leucrotta focusing on the High GOR Light Oil Window;

- only comprise approximately 5% of Leucrotta’s Montney land base;

- have a small production base (approximately 375 boepd) with a net cash flow to Leucrotta of $0.7 million in 2020; and

- had only 0.9 MMboe of reserves on a PDP basis assigned by GLJ Ltd. (“GLJ“), independent qualified reserves evaluator of the Company, as at December 31, 2019. Undeveloped reserves of 21.2 MMboe were also assigned by GLJ with corresponding $79.8 million of future development costs (FDC).

Additional Transactions Could Augment and Pull Forward Asset and Share Value

There is tremendous potential to augment shareholder value given initial Mica Project develops only 30 of over 240 net sections of total Montney lands and only one of three potential Montney zones. Such transactions may include, among other things:

- Selling additional lands to accelerate drilling;

- Executing Joint Venture arrangements on portions of the land base other than the Mica Project; and

- Other capital arrangements to accelerate capital development and bring value forward.

Financial and Guidance

On completion of the Financing and Asset Sale, Leucrotta will have no debt and approximately $45 million cash. Based on a 2021 capital program of approximately $30 million, Leucrotta estimates it will have cash on hand at year-end of approximately $20 million and no debt.

Leucrotta anticipates that the 2021 Exit Production Rate will be approximately 4,500 boepd (27% light oil and condensate).

Advisors

RBC Capital Markets acted as Financial Advisor with respect to the Asset Sale and Haywood Securities Inc. acted as Strategic Advisor with respect to the Asset Sale and Financing.

Oil and Gas Metrics and Disclaimer

This news release contains metrics commonly used in the oil and gas industry, such as “IRR”, “OGIP” and OOIP. These terms do not have standardized meanings or standardized methods of calculation and therefore may not be comparable to similar measures presented by other companies. Readers are cautioned that the information provided by these metrics, or that can be derived from the metrics presented in this presentation should not be unduly relied upon. The following oil and gas metrics have the following meanings as used in this news release:

IRR – Internal Rate of Return. IRR is the discount rate required to arrive at a NPV equal to zero. Rates of return set forth in this news release are for illustrative purposes. There is no guarantee that such rates of return will be achieved in the future.

NPV – Net Present Value is defined as “the present value of future cash flows minus the initial capital”.

PV – Present Value is defined as “the present value of future cash flows”.

Boe – Barrel of Oil Equivalent. All boe conversions in the report are derived by converting gas to oil at the ratio of six thousand cubic feet of natural gas to one barrel of oil equivalent. A boe conversion rate of 1 Boe: 6 Mcf is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Readers are cautioned that Boe may be misleading, particularly if used in isolation.

OGIP (Original Gas in Place) and OOIP (Original Oil in Place) are equivalent to Total Petroleum Initially In Place (“TPIIP“) for the purposes of this news release.

TPIIP, as defined in the Canadian Oil and Gas Evaluations Handbook (“COGEH“), is that quantity of petroleum that is estimated to exist originally in naturally occurring accumulations. It includes that quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations, prior to production, plus those estimated quantities in accumulations yet to be discovered (equivalent to “total resources“). There is no certainty that any portion of the resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the resources.

The OGIP and OOIP estimates quoted in this news release are unaudited internal estimates effective December 31, 2020 prepared by a qualified reserves evaluator in accordance with the COGEH Handbook. “Internal estimate” means an estimate that is derived by the Company’s internal APEGA certified engineer(s), and geologist(s) and prepared in accordance with National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities. Product type for the OOIP number is “tight oil” and product type for the OGIP number is “shale gas”. The location of the resource is the lands depicted in orange on the map on page 1 of this news release excluding the sections labelled “disposition”. Of the 246 net sections, Leucrotta has an average ownership working interest of 95% (258 gross sections). The key variables relevant to the evaluation are porosity, reservoir thickness, pressure, water saturation and gas composition which have increasing uncertainty, both positive and negative, with distance from existing wells.

Mica Project

The “Mica Project” referenced in this press release is a conceptual development study of Leucrotta’s resources (Prospective and Contingent Resources) of tight oil and shale gas in the Lower Montney formations on 30 net sections (30 gross) of land in the Mica Area. Leucrotta’s average working interest in the lands is 100%. The evaluation is an unrisked full development of the resource with multi-stage frac’ed horizontal wells using best-estimate type curves scheduled over a 5-year time period, effective January 2021. A total of $543 million of capital (undiscounted) is required for the project with an initial cash outlay of $112 million before payout is anticipated (5.5 years). The assumed commodity price is a flat WTI USD$50.00/bbl; AECO CAD$2.25/GJ; FX 1.28 CAD/USD forecast. There is no assurance that the forecast price and cost assumptions used in the evaluation will be attained and variances could be material. The actual scope of the project will be dependent upon the availability of funding, regulatory approvals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results, additional reservoir information that is obtained, and other factors. There is uncertainty that it will be commercially viable to produce any portion of the resources. For the prospective resources there is no certainty that any portion of the resources will be discovered and if discovered, there is no certainty that it will be commercially viable to produce any of those resources. The evaluation is an internal estimate prepared in accordance with the COGE handbook by a qualified reserves evaluator.

Reserves Data

There are numerous uncertainties inherent in estimating quantities of light and medium oil, tight oil, shale gas, conventional natural gas and NGL reserves and the future cash flows attributed to such reserves. The reserve and associated cash flow information set forth above are estimates only. In general, estimates of economically recoverable light and medium oil, tight oil, shale gas, conventional natural gas and NGL reserves and the future net cash flows therefrom are based upon a number of variable factors and assumptions, such as historical production from the properties, production rates, ultimate reserve recovery, timing and amount of capital expenditures, marketability of oil and natural gas, royalty rates, the assumed effects of regulation by governmental agencies and future operating costs, all of which may vary materially.

Individual properties may not reflect the same confidence level as estimates of reserves for all properties due to the effects of aggregation. This news release contains estimates of reserves and FDCs of the Company’s individual properties contained in the Asset Sale.

The reserves data contained in this news release has been prepared in accordance with NI 51-101. The reserve data provided in this news release presents only a portion of the disclosure required under National Instrument 51-101. All of the required information will be contained in the Company’s Annual Information Form for the year ended December 31, 2019, available on SEDAR at www.sedar.com.

Reserves are estimated remaining quantities of oil and natural gas and related substance anticipated to be recoverable from known accumulations, as of a given date, based on the analysis of drilling, geological, geophysical and engineering data; the use of established technology, and specified economic conditions, which are generally accepted as being reasonable. Reserves are classified according to the degree of certainty associated with the estimates as follows:

Proved Reserves are those reserves that can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves.

Probable Reserves are those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less than the sum of the estimated proved plus probable reserves.

This news release discloses reserves information for the Asset Sale in two categories: (i) proved developed producing (PDP); (ii) proved plus probable undeveloped locations. The evaluation was part of the year-end corporate reserves evaluation effective December 31 2019 and was prepared by an independent qualified reserves evaluator.

The PDP reserves pertain to three producing gas wells.

The proved plus probable undeveloped reserves pertain to 21 locations on the Asset Sale lands of which 10 are proved undeveloped and 11 are probable undeveloped.

Certain information provided in this news release may constitute “analogous information” under applicable securities legislation, such as reserve and resource estimates or the reserves and resources present on the Company’s lands, and nearby lands, total production and production-rates from wells drilled by the Company or other industry participants located in geographical proximity to lands held by the Company. This information is derived from publicly available information sources (as at the date of this news release) that the Company believes are predominantly independent in nature. The Company believes this information is relevant as it helps to define the reservoir characteristics in which the Company may have an interest. The Company is unable to confirm that the analogous information was prepared by a qualified reserves evaluator or auditor or in accordance with the Canadian Oil and Gas Evaluation Handbook and therefore, the reader is cautioned that the data relied upon by the Company may be in error, may not be analogous to the Company’s land holdings and/or may not be representative of actual results of wells anticipated to be drilled or completed by the Company in the future.

Forward-Looking Information

This news release contains forward-looking statements and forward-looking information within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “should”, “believe”, “intends”, “forecast”, “plans”, “guidance” and similar expressions are intended to identify forward-looking statements or information.

More particularly and without limitation, this document contains forward-looking statements and information relating to the Company’s capital programs, timing of the completion of the Asset Sale, management estimated 2021 Exit Production Rate, management estimated debt and cash as at year end and management estimate on anticipated future sources of capital. The forward-looking statements and information are based on certain key expectations and assumptions made by the Company, including expectations and assumptions relating to prevailing commodity prices and exchange rates, applicable royalty rates and tax laws, future well production rates, the performance of existing wells, the success of drilling new wells, the availability of capital to undertake planned activities, the availability and cost of labour and services, the exercise of the Over-Allotment Option, the use of proceeds of the Financing; the closing of the Financing and the receipt of all necessary approvals, including the approval of the TSX Venture Exchange.

Although the Company believes that the expectations reflected in such forward-looking statements and information are reasonable, it can give no assurance that such expectations will prove to be correct. Since forward-looking statements and information address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated due to a number of factors and risks. These include, but are not limited to, the risks associated with the oil and gas industry in general such as operational risks in development, exploration and production, delays or changes in plans with respect to exploration or development projects or capital expenditures, the uncertainty of estimates and projections relating to production rates, costs and expenses, commodity price and exchange rate fluctuations, marketing and transportation, environmental risks, competition, the ability to access sufficient capital from internal and external sources and changes in tax, royalty and environmental legislation. The forward-looking statements and information contained in this document are made as of the date hereof for the purpose of providing the readers with the Company’s expectations for the coming year. The forward-looking statements and information may not be appropriate for other purposes. The Company undertakes no obligation to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

The forward-looking statements regarding the Company’s expected 2021 cash flow and debt are included herein to provide readers with an understanding of the Company’s anticipated cash flow and the Company’s ability to fund its expenditures based on the assumptions described herein. Readers are cautioned that this information may not be appropriate for other purposes.

For further information, please contact:

LEUCROTTA EXPLORATION INC.

700, 639 –5th Ave SW

Calgary, Alberta T2P 0M9

Phone: (403) 705-4525

www.leucrotta.ca

Robert Zakresky

President and Chief Executive Officer

Nolan Chicoine

Vice President, Finance and Chief Financial Officer

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Share This: