CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

January 18, 2021

The irony cannot go unnoticed, the misleading narrative unchallenged.

If the developed world could prosper on slogans alone, we’d all be rich. Build back better. The great reset. Resilient recovery. Energy transition. Green new deal. Peak oil. Sustainable development.

Since the coronavirus and governments combined to tank the economy last year, we’ve been repeatedly told why policy makers dare not miss this one-in-a-lifetime (hopefully) opportunity to fix everything wrong with modern civilization.

And borrow trillions to do it if necessary. No cost is too high when you’re repairing the world.

Fortunately, real world economics and predictable human behavior have quietly soldiered on providing real hope for Alberta’s financial recovery.

Certainly, people and businesses have taken advantage of whatever government financial assistance has been available to endure the most significant economic disruption since the Second World War. Most are thankful public economic support has been available.

But the powerful market fundamentals of supply and demand remain impossible to dislodge. This will be what ultimately provides the employment, wealth and opportunities the vast majority of people seek.

Modern civilization still runs on resources, not platitudes or recycled public debt.

Like petroleum and natural gas.

Oil prices have recovered nicely at levels we’ve been told we might never see again. LNG prices in some markets have gone through the roof because of supply challenges and a major cold snap. Average spot prices for gas are the highest in five years.

We’ve been advised so frequently and loudly about what we must do that too many have lost sight of what we still do.

The individual decisions of 7.8 billion consumers determined to live another day by whatever means necessary has overwhelmed the endless warnings and advice from the World Economic Forum, the United Nations, the legion of noisy and well-funded climate alarmists, and the Liberal Party of Canada.

**********

Robin Winkle runs an independent oil research and advisory practice in Houston called Glenloch Energy (www.glenlochenergy.com). Last fall he put several oil demand outlook forecasts on one graph, reproduced below with his permission.

Sources are the International Energy Agency (IEA), BP, Energy Information Administration (EIA) and OPEC. The peak for global oil demand was 100 million b/d in late 2019 which is where all the forecasts begin.

The only projections that see world oil consumption being materially below 100 million b/d in twenty or thirty years are “IEA Sustainable Development”, “BP Rapid”, and “BP Net Zero” (assuming the world actually achieves net zero carbon emissions by 2050). The rest predict either growth or sustained demand.

While renewable energy will continue to expand, so will total energy consumption because of GDP and population growth. Despite relentless pleas, warnings and prognostications to the contrary, fossil fuels will still be the largest component of the global energy mix for decades.

Of interest is OPEC’s GDP and population data. By 2045 OPEC sees the world holding 22% more people, 9.5 billion instead of 7.8 billion today. Growth will come in the Middle East, Africa, Asia and OPEC countries. While China’s population will level off, India’s expansion will continue. Annual GDP growth will average 3.3% from 2022 onward. Using 2011 as a benchmark, GDP will rise from US$121 trillion to US$258 trillion, a 213% gain. China and India will be 40% of GDP in 25 years while the OECD countries will comprise only 31% of world GDP compared to 50% today. Climate policy will mirror 2015’s Paris Agreement but compliance will vary by country and respond to changing conditions.

The public never sees these figures.

The only way that oil demand will decline is if governments force consumers to use less. Dan Tsubouchi at SAF Group in Calgary follows the world, not the local politics or political drama, and unearthed this nugget from the IEA last week transcribed from an interview.

IEA Executive Director Fatih Birol said, “this decline in (oil) demand triggered a lot of discussion in the energy and climate circles and many colleagues thought the oil demand had peaked. And we were not sure. We said at that time, and we still say, if the governments do not take structural measures…we may well go back to where we were before the crisis in the year 2019… and therefore there was a need (for)…new government policies…China, the pandemic under control, the economy rebounds… Chinese oil consumption today is larger than it was a year ago.”

In his January 17 research note Tsubouchi added, “IEA doesn’t see peak oil demand anytime soon, rather oil demand rising in 2020s.” Quoting an IEA official Tsubouchi wrote, “As things stand, with the pace of change we see on the structural side is not enough in our view to deliver a peak anytime soon. Growth in the economy, recovery in the economy will sooner or later bring oil demand back to 2019 levels.”

“Structural” is bureaucratic lingo for government intervention to reduce fossil fuel consumption by law or regulation or impair its competitiveness with huge taxes. Otherwise, world oil consumption will continue to recover steadily with the vaccine rollout and economic rebound currently underway.

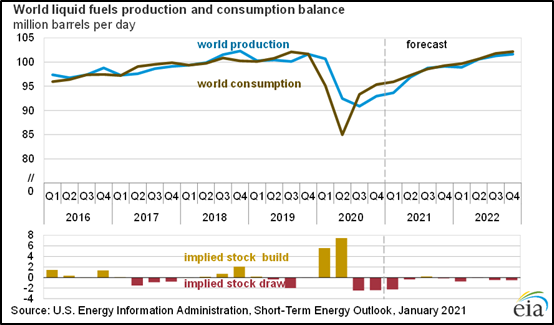

While the price quivers hourly depending on which country is restricting what, the trend is clear. Here’s January’s version of the next two years from the EIA.

The EIA figures oil consumption peaked at about 102 million b/d the third quarter of 2019 and will be back to that figure next year. We exited 2020 at about 95 million b/d, the same as total demand only five years ago. The red bars at the bottom show no inventory builds for the next two years.

This is obviously not what most folks have been reading or seeing on the daily news. Everybody has been focused on lockdowns, vaccinations, US politics, and how much money can be extracted from governments as you lose your job, your house, your business or your savings.

But capital markets track this data, as do oil producers. Thanks to the latest agreement by OPEC+ with its surprise announcement by Saudi Arabia that it would withdraw an additional 1 million b/d, WTI has again seen the sunny side of US$53 a barrel and WCS US$40.

More importantly, with demand becoming better understood, the focus is now on supply. This is where the anti-oil chattering classes and the climate alarmist industry have been considerably more successful. The oil price collapse, combined with the ESG and fossil fuel divestment movements, have starved the industry for sufficient cash and confidence to replace production and sustain future supply.

As a result, the numbers are very bullish for oil prices.

Goldman Sachs predicted last week that Brent crude could reach US$65 a barrel by mid-2021 thanks to OPEC+ and new US President Joe Biden’s commitment to at least throttle back American oil and gas development.

Even with much higher prices, nobody figures that US shale will grow like it has in the past when it acted as a cap on world prices for a decade. Remember, during the go-go years from 2009 to early 2020 US oil output grew by a staggering 8 million b/d.

A report by the International Energy Forum and Boston Consulting Group was released in early January and summarized by the Canadian Energy Centre on January 5. It read, “Without substantial new investment, world markets could be short 27 million barrels of oil equivalent per day by 2022 due to the sharp drop in spending by producers because of COVID-19…The report predicts the shortage could rise to 68 million boe/d by 2030 even if demand growth post-COVID continues at below the historical average. It warns that reduced supply could lead to greater market volatility and higher prices, slowing the global economic recovery and jeopardizing energy security and international goals like reducing greenhouse gas emissions and supporting social equity.”

In simple English this means that if oil prices go way up, this will have the same dampening effect on the global economy as in the past. Energy prices that are too high or rise quickly have always been recessionary.

If consumers have to spend way more money on oil and its myriad of products that currently have no alternatives, they will have less money to spend on everything else. This will have the exact opposite outcome on the post-COVID economy that we’ve promised by the “resilient recovery”, “build back better”, and “great reset” baloney we’ve all been subjected to for the past nine months.

That’s why these “transformative” initiatives must be bankrolled by governments. Because ordinary people can’t possibly afford them.

Will the developing and growing nations of Asia, Africa and South America compel their citizens to pay more for electricity and transportation fuel?

No.

Natural gas prices are also making a big comeback despite continuous efforts to label methane as too harmful to permit consumption growth. Gas demand is forecast to grow for years.

LNG prices were clobbered by the pandemic and because new export terminals were cancelled or postponed. But because of an exceptionally cold weather in Asia and other markets, LNG has gone through the roof, at least temporarily. Cargoes of LNG delivered to Japan and South Korea jumped to an all time record US$32/mmBtu in January, prices not seen since 2013 and 2014. Europe peaked at US$9.34 in the same period. Prices for natural gas in Britain hit highs not seen since 2018.

All these events, combined with the decline in gas development in the US, has caused Goldman Sachs to review its outlook for American gas prices. It has increased its price for mid-2021 to US$3.25/mmBtu from US2.80. At the January 15 close, the Henry Hub forward strip on CME saw gas rising steadily to US$3.16 a year from now. These are the best gas prices producers have seen in years.

This is also affecting Canadian markets. According to the Stifel/First Energy PSAC commodity report for January 13, the AECO 12-month average futures price was $2.77, 39% higher than the same figure a year ago. AECO average 2022 futures closed at $2.47, up 26% from the close last year. The AECO C closing spot price for January 2022 on January 15 was C2.91, way up from only the pre-COVID futures price of only $2.27 a year ago.

Even with the massive uncertainly associated with vaccines, ESG investing, restricted debt and equity capital and the Liberal pronouncements of skyrocketing carbon taxes and the new Clean Fuel Standard, the Canadian industry has announced its intention to continue reinvesting in its future.

CAPP reported January 13 that its members would be increasing capital spending for 2021. It’s good news, but regrettably the bar was set extremely low last year.

“…(CAPP) is forecasting a 14 per cent increase in upstream natural gas and oil investment in 2021. Capital spending in the sector is expected to be around $3.36 billion higher this year, reaching $27.3 billion, compared to an estimated total investment of $24 billion in 2020. The planned investment for 2021, while increasing from the lowest levels in more than a decade, would halt the dramatic decline seen since 2014, when investment sat at $81 billion. This year’s forecast represents a stabilizing of industry investment and the beginning of a longer-term economic recovery.”

What’s happening to oil and gas is part of a greater economic revolt by the real economy against the government-managed future we’re told is essential to save civilization. People are continuing to buy what they actually need, not what they are told they need. If current and planned massive government spending causes inflation – which is likely inevitable once the economy recovers – this will spill over into other commodities.

Iron ore bottomed out at US40.50 a tonne in 2015. By January 15 it was up to US$173.69, a 400% gain. This is the highest price since 2011. Australia’s miners are reopening shuttered mines as China pays whatever it must to meet steel demand.

More steel requires more high-quality thermal coal. On the eastern slopes of southern Alberta an Australian company wants to develop a steelmaking coal mine to serve export markets. The Grassy project is 7 km. north of the legacy Blairmore coal mining region on an abandoned surface coal mining site. It has the support of multiple Indigenous groups and local business.

Known economic luminaries like musicians Corb Lund and Paul Brandt have publicly stated their displeasure. Opponents make it sound like a nuclear waste dump, a regrettable position in a province built by coal with a $24 billion budget deficit and an 11% unemployment rate.

Copper hit a multiyear low of US$2.15 per pound in March of last year. Early this month it was up to US$3.66, a 70% gain only 10 months. Of course the world needs more copper with all the focus on electrification of everything.

Wheat is 50% higher than it was five years ago. But the cost of fuel to plant, grow, harvest and ship wheat and other grain crops is scheduled to increase significantly because of carbon taxes. Our country used to be world-renowned for growing and exporting wheat. Saskatchewan was coined “the breadbasket of Canada”.

At least it was. But we can’t do that anymore. You know. Paris. Net zero by 2050. Who cares what food costs when you’ve got all of humanity to protect?

**********

When I wrote my book about Alberta, fossil fuels and climate change two years ago, I could not fathom the vast gap between perception and reality; the public debate versus how the world actually works.

The best explanation I could come up with was the parallel universe phenomenon. This is where we all occupy the same planet but don’t see the same things.

Where you fuel up with gasoline to drive to a pipeline protest you learned about on your plastic handphone powered by coal or gas fired electricity.

Or you believe reducing Canadian emissions by any means possible without cooperation from the other 99.5% of the planet’s population will somehow mitigate global climate change. We can change the weather through virtue signalling and economic self-immolation.

Meanwhile, those without a microphone, soapbox or social media account are collectively roaring their unwavering demand for essential resources by continuing to purchase them.

Those dominating the public debate claim to speak for all of mankind. But they ignore the sound of the world’s cash registers ringing as the world’s billions buy whatever they need to survive at the lowest possible cost.

Because they can. And because they must.

This will serve Alberta resource producers well in 2021 and many years thereafter.

David Yager is an oil service executive, energy policy analyst, oil writer and author of From Miracle to Menace – Alberta, A Carbon Story. More at www.miracletomenace.ca

Share This:

COMMENTARY: The Green Movement Didn’t Stop Pipelines. It Nationalized Them.