CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Charles St. Arnaud

Chief Economist at Servus Credit Union

Key takeaways:

- The MoU between Canada and Alberta aims to position the country as an energy superpower while achieving net-zero emissions by 2050.

- In its current form, the strategy rests on three pillars: new pipeline access, increased production, and decarbonization, requiring roughly $90bn in upfront investment. All three pillars must proceed simultaneously, and failure in one undermines the entire framework, adding to the overall risk of the individual projects.

- The industry has matured over the past decade, from acting like a “startup” to behaving like a “utility company”. Despite strong revenues and profitability, the oil sector has shifted away from reinvestment and growth toward efficiency and returning cash to shareholders; a behaviour seen globally, not just in Canada.

- The economics of Canadian oil mean that the capital costs are front-loaded, creating a significant hurdle to investment. However, once the capital has been spent, the economics flips from profit maximization to loss minimization. As a result, the breakeven oil prices required fall drastically, currently likely below $40 a barrel, making these projects economically viable for decades and unlikely to become stranded assets.

- A decade of strong dividend payout may have changed the composition of the shareholders in the industry and reduced their tolerance to risk. This makes them more reluctant to commit capital to large, long-term projects and sacrifice their dividend income.

- To ensure the investment goes ahead, governments will likely need to de-risk these projects. While increased certainty regarding approvals, permitting, and timelines will be essential, it will not be enough. Financial support from governments, of at least $19bn to as much as $60bn, will likely be required.

- This will raise challenges to get public acceptance, especially given the high profitability of the oil industry, ongoing household affordability concerns, and continued struggles of industries affected by the US tariffs

- The economic benefits of expanding oil production and exports are generally positive, generating wealth and prosperity and a strong tailwind for the economy; the experience with TMX proves it (see Year one of TMX: Increased export diversification, disappearing oil discount, and C$13bn in extra revenues).

- However, it must be understood that the economic multiplier and benefits are the highest during the investment phase of the projects. Once the project reaches maturity, the economic multiplier tends to fall, and the economic benefits will depend on whether and how the project’s revenues are returned to the economy.

- The experience of the past decades also shows that these gains have not been broad-based and have had mixed impact on the broader economy (see The Lost Decade(s): or how the oil boom masked Canada’s economic mediocrity and Where’s the boom? And the rise and fall of the Alberta Advantage). This suggests that, while beneficial, the industry may not be the economic saviour some of its proponents are suggesting, as it will depend on how these new revenues are ultimately spent.

Transforming Canada into an “energy superpower” has been the federal government’s catchphrase since it was elected last year. This ambition is also set out in the memorandum of understanding (MoU) signed with the government of Alberta. These developments have brought some hope that we will see a new wave of capital investment in the sector, boosting the economies of Canada and Alberta. However, many hurdles need to be passed before we start to see capital being committed and shovels in the ground.

The changes to the oil industry over the past decade and the behaviour of the sector over the past decade suggest that one of these hurdles may be the willingness to commit a huge amount of capital, in the hundreds of billions, despite the economic potential for the decades to come.

The 3-legged stool of the MoU

The memorandum of understanding (MoU), signed in late 2025, between the Government of Canada and the Government of Alberta aims to grow Canada’s energy sector and make the country an “energy superpower” while still aiming for net-zero emissions by 2050.

At the core of the MoU, in its current form, is the investment required in the oil and gas industry. Here, there are three pillars: 1) enhanced market access via a new pipeline to the Pacific Ocean, 2) increased production to ensure the pipeline is fully utilized, and 3) decarbonize the operations through carbon capture and sequestration.

It is important to note that, in its current form, all three pillars are mutually dependent. Without decarbonization, there will be no new pipeline. Without a new pipeline, there will be no new production projects. Hence, without decarbonization, there won’t be new production projects.

As a result, all three pillars need to be pushed and built simultaneously; otherwise, the three-legged stool will lose its balance and collapse.

Such an undertaking will require coordination, but most importantly, significant upfront capital investment. A quick estimate would put the cost of the pipeline to the West Coast at about $35bn (as a reference, the TMX expansion cost was $34bn). A new oil sand mine would likely require about $30bn of investment. The Pathways carbon capture project is expected to cost about $25bn. In total, at least $90bn in investment will be required before even producing and selling the first barrel of oil.

With upfront costs so high, it raises the question of whether the industry is ready to commit such a large sum of capital.

The Canadian oil sector: significant changes over the past decade

The oil sector has changed dramatically over the past decade.

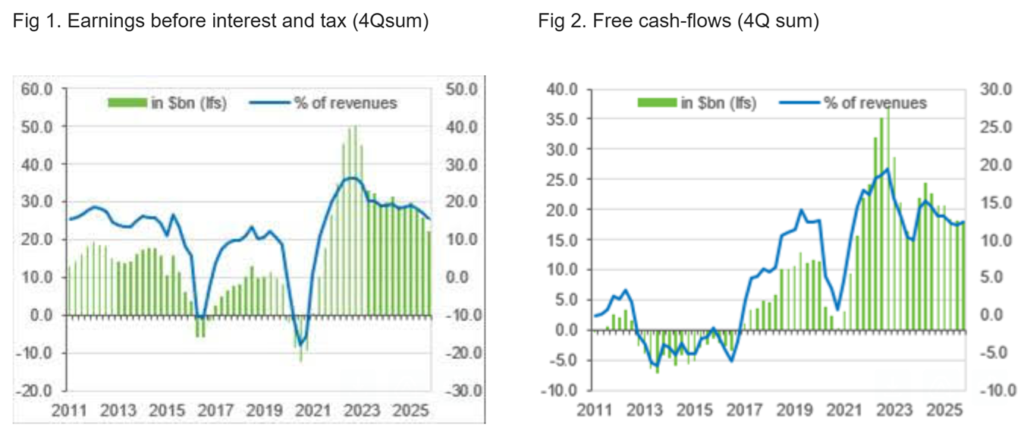

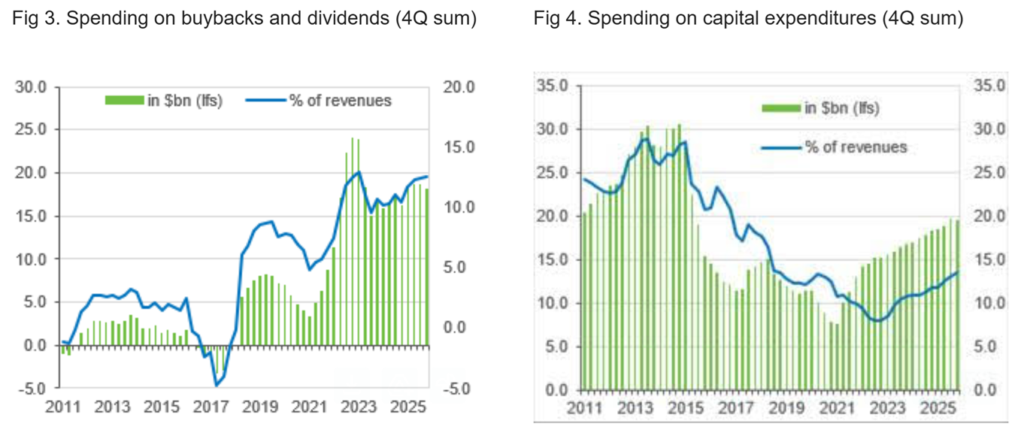

Revenues in the sector are close to record highs, thanks to a continued increase in production volume. As such, revenues are roughly 50% higher than they were in the mid-2010s, before the drop in oil prices. In addition to elevated revenues, we have seen an improvement in the sector’s profitability.

Free cash flows have been significantly positive in recent years, reaching approximately 12% of revenue over the past year. As a comparison, free cash flows were negative in the early 2010s. Similarly, earnings before interest and tax have remained elevated, representing about 15% of revenues over the past year, down from more than 25% in 2022, when oil prices were high following Russia’s invasion of Ukraine.

Source: Bloomberg, Servus Credit Union

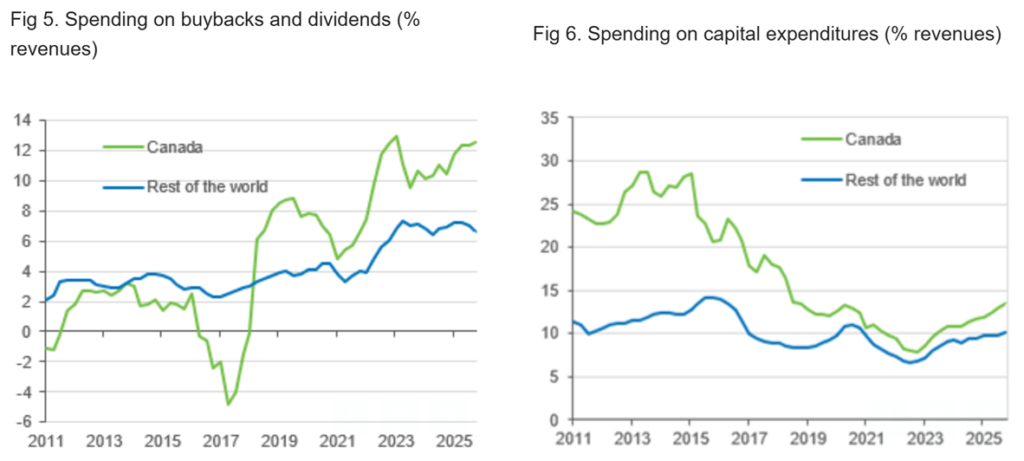

One of the changes over the past decade is how the industry is using these high revenues and profits. As we have shown on numerous occasions, since the 2014 oil price crash, the industry has been reinvesting a much smaller share of its revenues in the Canadian and Alberta economies. As a result, the elevated and likely record revenues are not as positive for the economy as the terms-of-trade would suggest (see The Lost Decade(s): or how the oil boom masked Canada’s economic mediocrity and The positive terms-of-trade from higher oil prices is not as positive as it used to be and for a recent discussion).

- A greater share of revenues is being returned to shareholders. We estimate that about 12% of revenue has been returned to shareholders through share buybacks and dividends in recent years. In comparison, that proportion was about 2.5% of revenues back in 2014. Moreover, it is estimated that about 75% of these shareholders are non-Canadian, compared to 62% in 2014. This means that most of the flows back to shareholders are not an inflow into Canada.

- A smaller share of revenues is invested back into operations. We estimate that they reinvested about 12% of their revenues (about $19bn) over the past year. This compares to almost 30% of revenues in 2014 (about $30bn).

Source: Bloomberg, Servus Credit Union

Canada’s industry is not special, and behaves like its global peers

There is a lot of talk in Canada that domestic factors are holding the industry back. However, when the Canadian sector is compared to its global peers, some very interesting observations can be made:

- The share of revenues being returned to shareholders by the global industry has also increased in recent years. As such, non-Canadian oil companies are returning about 7% of their revenues to shareholders, compared to 12% in Canada. Interestingly, the higher proportion of revenues flowing back to shareholders in Canada can be traced to higher profitability, with free cash flow as a share of revenues and earnings before interest and taxes (EBIT) as a share of revenues both higher for Canadian producers than for their peers elsewhere.

- Both Canadian and non-Canadian producers are reinvesting a similar share of their revenues back into their operations; 12% in Canada vs 10% globally. If Canadian-specific factors were holding back investment in the Canadian sector, we would have expected capital expenditures by Canadian firms to be lower.

These observations regarding the current situation are important. It shows that the lack of rebound in oil and gas investment over the past 10 years is not unique to Canada. It shows a global shift in shareholders’ preferences, with a preference for receiving a constant dividend and returns from operations rather than investing in operations. Moreover, low oil prices, averaging about $64 a barrel since 2015, were also a contributing factor. This trend also suggests that Canadian regulations, although arguably unhelpful, may not be the only reason for the sector’s lack of investment.

When we compare the Canadian sector to its international peers, the pre-2015 period looks exceptional, not the past 10 years. During that period, Canadian producers were investing almost 30% of their revenue into their operations, significantly above the 12% share for non-Canadian producers.

Source: Bloomberg, Servus Credit Union

From startups to utility companies

The strong investment between 2002 and 2015 was the result of a rush to develop the oil sands. After years of research and development, coupled with high oil prices supported by rising global demand, oil extraction from the oil sands became economically viable and profitable.

This newfound opportunity drove massive investments across the sector to adopt the new technology, with little consideration of short-term profitability, as companies rushed to be first to capitalize on it. This is very similar to what is observed with startups in the technology sector, where, in the early days, growth and scaling up are the main strategies.

However, the sharp drop in oil prices in late 2014-early 2015, with prices declining by $60 in about six months, put an end to the investment boom.

Nevertheless, investments made in the 2010s are now reaching maturity and generating significant revenues and profits. In addition, there has been a shift in focus, with profitability through efficiency gains as the priority rather than growth.

As such, oil companies now look more like utility companies, where the model is to produce, sell, and return profits to shareholders.

Lower economic multiplier

Another important aspect of the maturation of the oil industry is that the economic multiplier associated with activity and capital expenditure in the sector is also lower during the “mature phase” than during the “startup phase”.

As we have shown (see Where’s the boom? And the rise and fall of the Alberta Advantage), there is a strong link between investment and income. As the share of investment in GDP increased in Alberta between the early 2000s and the mid-2010s, we saw Alberta’s income outperform the rest of the country. Since the drop in oil prices in 2014 and the resulting investment bust in 2015, we have seen Alberta’s income underperform and gradually converge toward the national average, while remaining above it.

In addition, as we have shown (see Where’s the boom? How the impact of oil on Alberta may have permanently weakened), the type of capital expenditure matters when assessing its economic impact.

Back in the investment boom years, capital expenditures had a much bigger impact on the broader economy. Workers needed to be hired to prepare the land, build roads, and other infrastructure, thereby increasing activity in the construction sector. As some of the building materials, machinery, and equipment are produced in the province, this increases activity in the manufacturing, wholesale, and retail sectors. The development, planning, and design of the project require expertise from engineering and other specialized firms, thereby boosting the professional, scientific, and technical sector.

Currently, in addition to being reduced in size, capital expenditures have a significantly lower economic multiplier. The focus on efficiency gains means that spending is more capital-intensive, requiring fewer workers. Moreover, much of the capital is likely imported, meaning more spending is going outside of the province.

Overall, this means that for each dollar currently spent on capex, a smaller share stays in the province.

The economics of oil production: legacy projects vs new projects

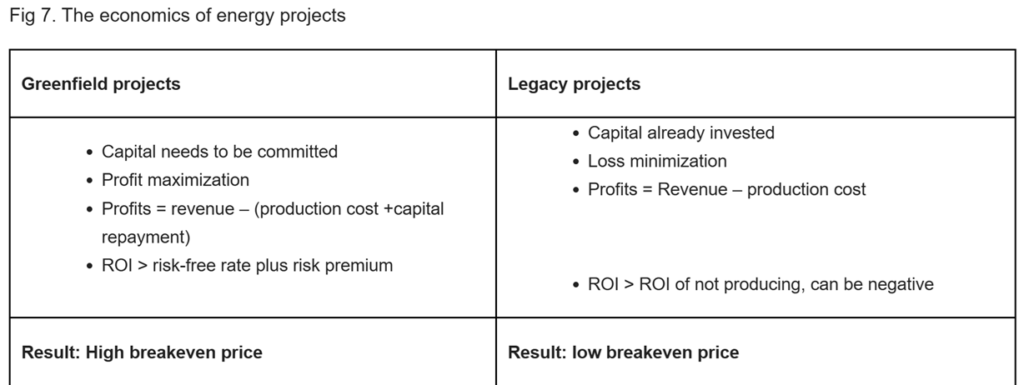

Oil projects in Canada are often viewed as having a high breakeven point, meaning that they require elevated oil prices to turn a profit.

However, the reality is quite different, and the legacy projects, those built during the mid-2000s to mid-2010s boom, are proving to have low break-even points, depending on the project.

What makes Canadian oil sands projects different is that capital investment is front-loaded. In other words, these projects require a huge amount of capital at the initial stage, even before producing their first barrel of oil.

This creates two different frameworks to judge the profitability of projects: 1) new projects, where the capital needs to be committed, and 2) legacy projects, where the capital has already been spent. Both types of projects have different economics.

The economics of new projects is usually what most observers have in mind when thinking about investment in the sector. A decision needs to be made on whether the project will be profitable and whether to deploy the capital. This means that the return on investment needs to be positive and above the risk-free rate, including reimbursing the committed capital. The result is a higher break-even price and a longer timeline to profitability.

For legacy projects, the initial capital is already committed and spent. This dramatically changes the analysis. The main change is that the objective switches from profit maximization to loss minimization. This means that, as long as it is less costly to produce than not to, the project will remain active. The reason is that by producing, the company can repay even a small part of the initial capital, reduce overall losses, and even return a profit over the long term. In other words, as long as the ROI of producing is higher than the ROI of not producing, the project will remain active.

This means that legacy projects have a significantly lower break-even point than new projects; the price only needs to exceed the variable cost. A CD Howe Institute paper pegged the breakeven price below $40 a barrel[1], but continued investment in efficiency in recent years may have pushed it even lower. For this reason, current oil projects will continue to produce and be profitable for decades to come and are unlikely to become stranded assets.

Hence, once capital is committed, even new greenfield projects will remain productive for decades and are highly likely to generate profits. With this in mind, how can we ensure the capital is committed in the first place?

Source: Servus Credit Union

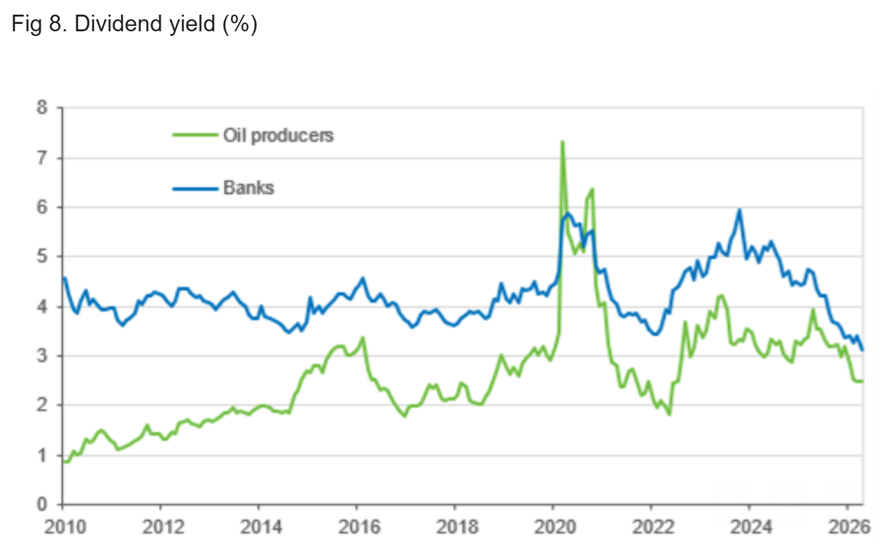

Are shareholders willing to sacrifice their dividend income?

As we have shown earlier, the industry has returned a greater share of its revenues to shareholders through dividends and share buybacks over the past decade. One has to wonder whether this has changed the types of shareholders in the industry and lowered their risk tolerance.

In the 2000s and early 2010s, when dividend payments and dividend yields were low, these shareholders likely invested in the sector seeking growth prospects, i.e., rising share prices.

However, with dividend yields currently only marginally below those of Canadian bank stocks, a larger proportion of shareholders likely hold stocks in the industry for steady dividend income rather than for potential capital appreciation.

This raises an important question: if the shareholders are primarily after a steady revenue stream from dividend payments, are they willing to risk capital to grow operations and ensure the MoU goes forward? Put differently, are shareholders more risk-averse now than a decade ago?

Ultimately, shareholders decide whether capital will be deployed for new projects, not the company’s executives. They will need to decide whether the expansion of operations is a “nice to have” or “a must have”.

Source: Bloomberg, Servus Credit Union

Investing capital comes with risks and will likely result in smaller dividend distributions to finance the investment. In the case of the MoU alone, we are talking about almost $100bn in upfront investment from the industry before even producing the first barrel of oil.

While the normal risks associated with these types of projects are well known (regulation, court challenges, uncertainty, long recoupment period, etc.), there are additional risks with the MoU: execution and coordination risks.

As explained, the MoU is based on three pillars, and all three need to proceed simultaneously. If one fails, the other two fail. This means that the risk of each project is not only specific to the project itself but also depends on the likelihood that the other projects will go ahead. As a result, the risks are compounded.

Governments will need to de-risk the investment.

What are the hurdles to the investment that will need to be addressed to ensure a successful MoU?

- Regulations, permitting and court challenges are major risks that have plagued most major projects. Hence, providing certainty regarding approvals, permitting, and timelines will be important. However, it may not be enough.

- The front-loaded nature of the costs and capital commitments for new projects means the hurdle to proceeding with new investments is very steep.

- The behaviour of shareholders in the industry suggests they are more risk-averse now than a decade ago and may need more financial certainty before deploying capital and risking their dividend payments.

- Each part of the MoU (pipeline, new production, and decarbonization) depends on the success of the others, adding considerable uncertainty.

As a result, when the sector’s economics and behaviour are considered, it becomes clear that these projects will require some form of financial derisking or government support to proceed.

Already, about 75% of the capital cost for carbon capture and sequestration projects is covered by various tax credits. In the case of Pathways, this means that the government is already committing to cover almost $19bn out of the current $25bn price tag. Yet, despite this support, there is no firm commitment to the project. However, the companies in the sector are only acting rationally, since decarbonization is viewed mostly as a cost, with little benefit, at least in the short run.

Similarly, there is yet to be an official private proponent for a new pipeline to reach the West Coast, and the question may well be whether the required capital is justified, given the project’s risks, especially in light of the experience with TMX: cost overruns and delays.

The question is how much support will be required and what type of support? What is certain is that we are talking about support that will amount to multiple tens of billions of dollars. In the best-case scenario, where it’s only the tax credit for carbon capture, $19 bn. In the worst case, the government may need to fully pay for decarbonization ($25bn) and the pipeline to the West Coast ($35bn), for a total of roughly $60bn. But these estimates could prove too conservative, and the actual costs may be higher.

Are voters on board with massive financial support for the most profitable industry in Canada?

This will be a tough question for politicians and the industry to answer.

Voters will need to be convinced that spending tens of billions of dollars to support an industry that is highly profitable and has the financial capacity to commit the capital required for these investments is warranted. The experience of the federal government’s purchase of TMX suggests that the general population will need to be convinced that such support is not “corporate welfare”.

This is particularly true when households remain concerned about affordability and the cost of living. Similarly, workers in industries that have been deeply affected by US tariffs may wonder why support is not being directed to vulnerable industries to protect their jobs.

It will require significant, coordinated effort from the government and industry to make a strong case for government participation. This will make a strong case for how a successful MoU will benefit the broader economy, not just oil-producing regions and the industry. Similarly, governments will need to ensure that they get a return on their investment.

Investment in the energy sector can generate enormous wealth and prosperity and can be a strong tailwind for the economy. For example, the expansion of the TMX pipeline is estimated to have generated about $30bn in extra revenues for the oil industry since its opening, thanks to the narrowing oil differential. To put this in perspective, this is equivalent to adding three extra months of production at no cost (see Year one of TMX: Increased export diversification, disappearing oil discount, and C$13bn in extra revenues).

Similarly, as we have shown (see Where’s the boom? And the rise and fall of the Alberta Advantage), the strong capital expenditure between the mid-2000s and mid-2010s led to broad-based wage outperformance in Alberta across all industries compared to the rest of Canada.

However, as we have shown (see The Lost Decade(s): or how the oil boom masked Canada’s economic mediocrity), evidence from the past two decades suggests that investment in oil and gas between the mid-2000s and the mid-2010s had a mixed effect on the Canadian economy. As such, the investment boom led to strong aggregate economic growth but had little spillover to the non-resource side of the economy. In fact, as we conclude, the oil boom only masked deep economic issues in the rest of the economy. This meant that when oil prices and investment collapsed in the mid-2010s, the other sectors of the economy were ill-equipped to take the lead in pushing the economy forward. In addition, as we have seen in recent years, if revenues and profits are not staying in the country and reinvested in the economy, the spillover to the rest of the economy remains minimal.

Conclusion

The MoU between Alberta and Ottawa will require significant capital investment to be successful. While regulation and permitting challenges are often cited as hindrances to these projects, considering the economics of these projects and the behaviour of the oil and gas sector in recent years makes it clear that the various levels of government may need to step in to de-risk them financially. Considering the size of the investment required, close to $100bn, it will mean tens of billions of dollars in support from governments. Such substantial financial support for one of the most profitable industries in Canada will likely draw heavy criticism, especially at a time when households continue to face significant affordability issues and other sectors of the economy are bearing heavy consequences from US tariffs. Governments and the industry will need to convince the public of the economic benefits of such heavy support.

The economic benefits of expanding oil production and exports are generally positive, and the economics of Canadian oil suggest that the industry will remain viable for decades. However, the experience of the past decades also shows that these gains have not been broad-based and have had mixed impact on the broader economy. This suggests that, while beneficial, the industry may not be the economic saviour some of its proponents are suggesting, as it will depend on how these new revenues are ultimately spent.

Share This: