CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By: Tegan Hill and Nathaniel Li

Alberta’s Lost Tax Advantage

- As recently as 2014, Alberta had the lowest top statutory combined (federal and provincial/state) personal income tax rate and business income tax rate in North America. Paired with no provincial sales tax, the “Alberta Tax Advantage” made the province an incredibly attractive place to start a business, work, and invest.

- In 2015, however, the NDP provincial government raised taxes. Tax changes at the federal level in both Canada and the United States further impacted Alberta’s tax competitiveness.

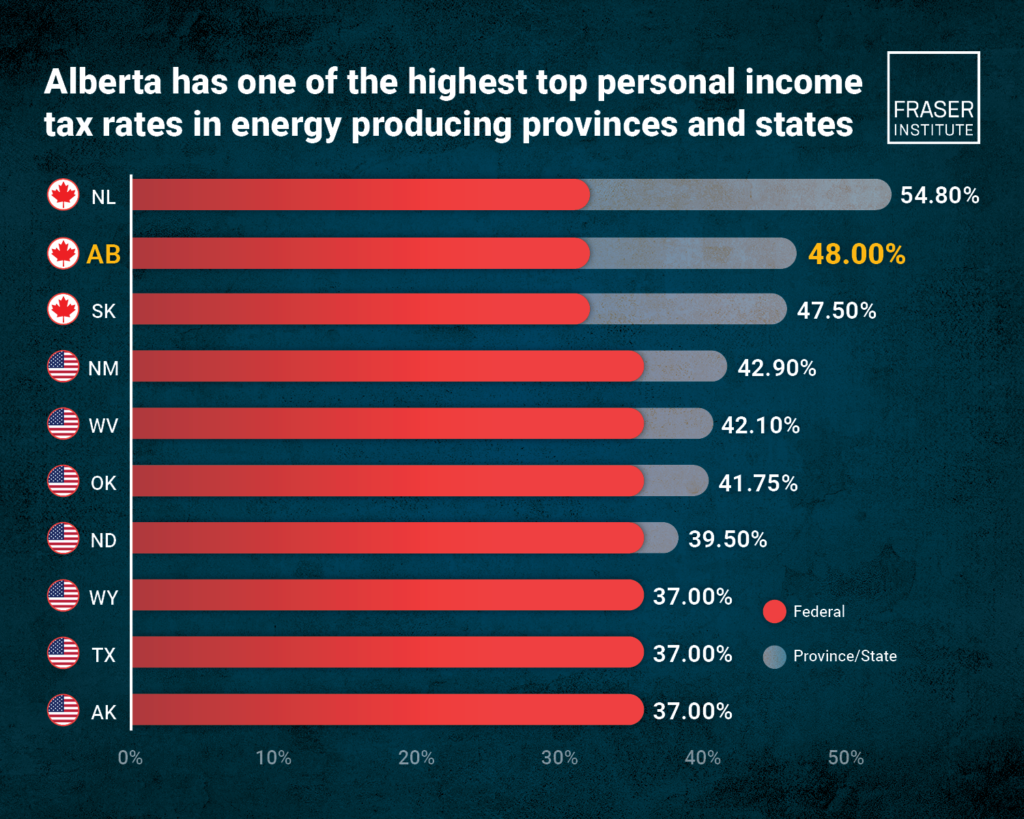

- This bulletin assesses Alberta’s current tax competitiveness, focusing on key pillars of its previous advantage compared to 60 jurisdictions across Canada and the United States, with particular focus on energy jurisdictions.

- Alberta now has the 10th-highest top personal income tax (PIT) rate in North America at 48.00 percent. This is significantly higher than the energy-driven US states for which Alberta competes for investment and talent, including Alaska, Texas, Wyoming, North Dakota, Oklahoma, West Virginia, and New Mexico. Assuming the capital gains inclusion rate is increased to 66.7 percent, Alberta’s 32.00 percent top combined capital gains tax rate is also significantly higher than that of US energy states.

- Alberta’s general top combined corporate income tax (CIT) rate is the 7th lowest among 61 peer jurisdictions and the lowest of any province at 23.0 percent. Alberta holds the third-lowest combined sales tax in North America at 5.00 percent.

- To improve Alberta’s tax competitiveness, the Smith government should prioritize reducing provincial PIT rates, which would also lower capital gains tax rates.

Share This:

COMMENTARY: Carney’s Command of Canada’s Projects: What Gets Built, What Gets Blocked, and Who Decides – Ron Wallace