CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

“On top of the strong demand growth, similar to what we have seen in the past, new lithium supply outside of SQM has been delayed and slow to come online,” it said. That will keep the market tight and means “this high-priced environment could continue for the remainder of 2022 and into 2023.”

Lithium has more than tripled in price over the past year, and it’s rallied more than 1,200% since 2020. The extraordinary surge has been driven by tight supplies for electric-vehicle manufacturers, one of the bright spots in China’s struggling economy, but cracks in near-term consumption may now be starting to surface.

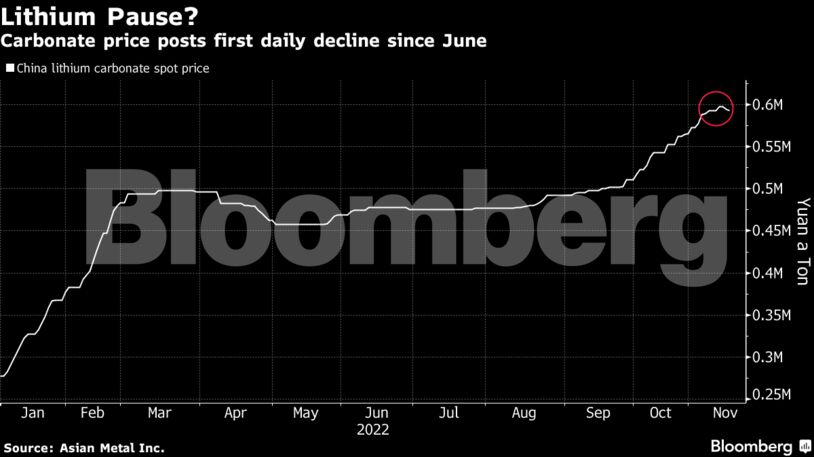

Spot prices for lithium carbonate in China edged lower this week to register their first drop since June, according to data tracked by Asian Metal Inc. Speculation that demand for the battery material may soften triggered a slump in some leading lithium stocks, with top producers Albemarle Corp. and SQM tumbling this week.

While the EV market and its supply chain are heading for substantial long-term growth, there are some headwinds for the pace of expansion in China. Subsidies for EVs that encouraged rapid expansion over the past decade are due to be phased out next month, despite speculation they may be extended.

The slump in lithium equities came after a sharp fall in lithium futures on China’s Wuxi Stainless Steel Electronic Trading Center, where prices are prone to bouts of severe volatility. Analysts including Yettie Yi, head of new energy research at Shanghai Metals Market, said signs of weaker EV demand growth, and purchasing cutbacks by battery cathode producers, had triggered a downturn in sentiment.

SQM’s net income for the third quarter beat analyst estimates, rising by more than ten times to $1.1 billion.

Despite possible short-term headwinds, JPMorgan recently reiterated SQM at overweight and raised its price target, citing lithium prices that are “still chasing the peak” and resilient markets ahead.

Share This:

COMMENTARY: Hot Air and Fires in Ontario Mean its Climate Panic Time in Central Canada: That’s Never Good News for Supporters of Conventional Energy Production – Jim Warren