CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

January 26, 2022

The major contributor to the seven-year oil price collapse from 2015 to 2021 was North America.

Growth in US light tight oil production was meteoric. When Barack Obama won the US presidency in late 2008, production was 5 million b/d. When he left eight years later it was up 74% to 8.7 million b/d. Production growth continued under Donald Trump. American oil output peaked at 13 million b/d in early 2020.

Canada’s contribution is often overlooked, but quite significant. Combined liquids production (conventional, oil sands, natural gas liquids) in 2008 was 3.2 million b/d. By 2019 it was over 5.3 million b/d, a 66% increase.

Combined, the US and Canada added over 10 million b/d over this period. World oil demand from 2008 to 2019 rose by 13.9 million b/d. Nearly three-quarters of that demand growth was supplied from North America. This was aided by seemingly unlimited support from capital markets.

You can’t be over-levered without first borrowing a lot of money, and that was easy for many years.

This is the largest oil producing region in the world currently governed by politicians who won elections on climate change platforms. Part of their policy commitments is that one way or another, what happened between 2008 and 2019 won’t happen again.

The big question asked by many oil analysts is: with oil demand and prices rising, will North America raise oil production enough to return oil markets to equilibrium? Armed with record cash flow from production, will the producers that helped collapse and cap world oil prices in 2015 and keep them there for six years do it again?

No. And it won’t be for the reasons most commonly cited in the trade press.

The official position from the EIA is that US oil production will resume growing. After averaging 11.2 million b/d last year, the latest forecast see this rising to 11.8 million b/d in 2022 and 12.4 million b/d in 2023.

If that occurs, 2023 output will be slightly higher than the last record average of 12.3 million b/d in 2019.

On December 9, the Canadian Energy Regulator forecast oil and liquids production would continue to rise to 5.8 million b/d by 2032. For 2023 the figure is estimated at 5.5 million b/d, up 4% from 2019. In 2021 Canadian output already reached record levels.

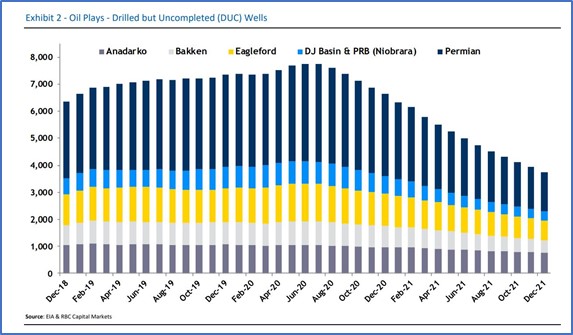

Stateside, the closely watched “DUC” or Drilled and Uncompleted wells continue to decline. Since US drilling tanked in the second quarter of 2020 because of COVID – and because of storms that clobbered the Gulf of Mexico last year – American output has declined. With drilling down for two years, output has been sustained by bringing the inventory of DUCs on stream.

According to the following chart from EIA and RBC, since June of 2020 to the end of last year the DUC count had declined by about 50%.

Creating this DUC inventory took a lot of drilling. Using Baker Hughes data, the number of active drilling rigs targeting oil required to keep DUCs in the average range of 7,000 in 2018 and 2019 was 807.

In 2021 the average was only 380. Obviously, the declining number of DUCs has helped sustain production as drilling slowly recovers. Since October, the average number of active rigs drilling for oil has risen to 462. But because only the most efficient rigs are working, there has been a productivity gain measured by wells per rig per year.

Capital budgets for 2022 are rising in Canada and the US, leaving many with the impression that more money should lead to increased production.

But historical behavior does not factor in the realities of the battered oilfield services sector and supply chain.

**********

There is lots of chatter about “capital discipline” in the E&P sector. The pandemic exposed weak balance sheets and poor returns. When cash flow recovered sharply last year, the percentage of free cash reinvested in capital expenditures was the lowest in history. It is expected to stay reserved in 2022 even if commodity prices rise.

Analysts looking at projected cash flow versus capital investment commonly cite capital discipline as a factor. But the financing requirements of the E&P sector has a supply chain issue of its own. Call it capital rationing, or ESG. While the concerted, coordinated and well-publicized efforts to restrict debt and equity capital for the fossil fuel sector is likely not as rigid as advertised, executives would be reckless to assume they can fund production growth like they have in the past. Nor do they want to undertake a major, multi-year capital commitment under the assumption external capital will be available in the future.

Paying down debt – and recent announcements by junior and intermediate operators that they intend to become debt-free – reflects the reality that financing production growth is much different today. Even if oil prices continue to rise and it becomes obvious a global petroleum shortage of is creating ever-higher energy prices, the ESG phenomenon that took years to create will not reverse itself quickly.

This could change. But the pre-pandemic decarbonization playbook is still in place in the minds of many in government, public policy and capital markets. As producers navigate a period when access to capital is difficult and increasingly restricted, nobody should be surprised if they behave differently.

Fortunately for producers, the term “capital discipline” is foreign to the service and supply sector. These companies have invested billions in new capacity to meet client needs, particularly high-performance drilling rigs, giant coiled tubing units and hydraulic fracturing capacity.

Unfortunately, in too many cases the service sector has put expertise and innovation before conservative financial management and the risks created by macro-economic cycles, commodity prices and punitive government policy.

Looking back at years of capacity additions and activity cycles, producers have often enjoyed OFS overcapacity which has created very competitive pricing.

However, what appears to a surplus of underutilized equipment does not fully explain the situation or the state of OFS.

There is a fundamental difference between OFS and E&P that is not well understood.

For producers, oil and gas can stay in the ground until the developer is ready to bring it to surface. These hydrocarbons have waited hundreds of millions of years. Another month, year or decade doesn’t matter. It does not deteriorate and lose its energy value. Or, as we’re reminded yet again, its long-term economic value.

The surface assets E&P companies own are to produce, process, transport and distribute oil and gas. Except for extraordinary events like Q2 2020, utilization rarely goes to zero. If it does in most cases it is only because the resources to which they are dedicated are exhausted or no longer economic.

For the service sector, unless business is steady and profitable, asset values deteriorate. Essential workers to turn machines into money go elsewhere out of necessity. Assets working at cost suffer from wear and tear without adequate maintenance. Major repairs and upgrades are unaffordable. Parts are cannibalized from idle equipment, further reducing capacity and company value.

And don’t forget rust which eventually destroys anything made out of steel.

Worse, the service sector’s massive supply chain also shuts down. Behind all the vendors and service companies at the wellhead, construction operation or production facility are an army of providers of everything from steel to engines to pumps to O-rings. When their business dries up, they suffer the same fate. Their staff leaves and their equipment and plants sit underutilized. This contraction cascades down the supply chain right to the source of the raw materials.

Everybody knows about the post-lockdown supply chain challenges and price inflation when they try to purchase food and the other necessities of life. It is no different for the oil industry.

Research shop IHS Markit released a report early this month titled, “The Great Supply Chain Disruption: Why It Continues in 2022”. In the introduction Vice-Chairman and noted oil writer and thought leader Daniel Yergin wrote,” There is no recent historical precedent for the current disruption in the modern highly integrated global supply chain system that has developed over the last three decades…Delays and disruptions for manufacturers and deliveries on a scale never recorded in our 30 years of PMIs (Purchasing Managers’ Index).”

What it means to oil specifically was released by petroleum industry research specialist Rystad Energy on December 1 in a news released titled, “US shale spending set to shake off uncertainty and jump 19% in 2022, topping $83 billion.” The headline looks promising. Spending for 2022 would be the highest since 2019, which looks like a strong recovery.

And it is, but not all that investment will result in increased production. Of the US$13.6 billion in higher investment, “service price inflation alone is set to add $9.2 billion.” While there will be some recovery due to operational efficiency gains, this is still US$30 billion lower than was expected for 2022 when Rystad did a multi-year forecast in late 2019.

What is the state of the oilfield service and supply sector in early 2022?

**********

The most frequently cited challenge for OFS is labor, and it is serious.

The oilpatch has long been challenged to attract workers because of seasonality, remote operations, camp life, and the expectation that you will continue working 24/7/365 regardless of the weather.

It compensated with high wages, interesting and challenging work, and endless opportunities for advancement in a growing industry.

But that’s ancient folklore in 2022. The only part remaining is the working conditions. The young generation that the industry has always managed to attract is increasingly urban, coddled and protected like no other, and has grown up in a society that has been told repeatedly that fossil fuels are bad and produced by an industry with no future.

You want me to do what? Where? Why?

The senior people will come back but are nearing or at retirement age.

Eventually, the industry will pay what it must. The clients have the cash if they want to get the work done. The problem for service and supply is much of the price increases being negotiated are just a flow through. The sector is back spending a lot of time and money looking under rocks for personnel and training new hands. But if they don’t like the work when they get to the field, the investment in recruitment and orientation is lost.

The equipment itself – drilling rigs and frac spreads – is reasonably new with much of it having been built in the past 10 years. The US fleet is in decent condition because it was running hard up until two years ago. In Canada, the downturn has been longer and more protracted. A lot of excess Canadian iron moved south years ago.

There is no equipment shortage as measured by existing capacity. Activity dropped so much so quickly two years ago that a large portion of the assets were parked, not worn out.

Keeping it going is another matter. Major components like drill pipe, engines and top drives for rigs are subject to long waiting lists. The cannibalization of mothballed equipment to keep working equipment functioning is more likely to take place this year than last as demand increases and spares and replacement parts take longer to secure.

But the sector’s supply chain has the same problem. Manufacturers of key components downsized their operations to demand to stay afloat, as did fabrication, repair and certification shops.

Anything made out of steel, which is pretty well everything, is a challenge.

One popular steel grade for ERW casing – US Midwest HRC (hot rolled coil) – has skyrocketed. From Q2 2016 to Q3 2020 the price ranged from a low of US$482 per short ton to a high of US$926 with an average of about US$700.

HRC peaked at US$1,932 on July 31, 2021. The January 22 close was US$1,438, twice what it averaged for several years pre-pandemic. Casing mills compete with the automobile industry for steel, but fortunately that sector is slow because of a shortage of microchips. This has given casing some relief on steel prices.

The outlook improves later in the year and in 2023 as supply chains stabilize, but higher prices for iron or and energy remain.

According to World Bank commodity data, iron ore averaged US$63.95/mtu (metric ton unit) from 2015 to 2019. The average price for the past 12 months has been US$161.71/mtu, although there have been some price reductions since August.

Then there’s metallurgical coal which is still a major component of the steel making process. Even if the world figured out and accepted where this coal fits in the essential commodity supply chain and quit persecuting it, will there be price relief? From 2012 to early 2021 this coal averaged US$85 a ton, ranging from a low of about US$48 and a high if US$119. It last traded at US$225, off a peak of US$240 last fall.

So the price of casing and tubing – some 20% of the cost of a well depending on measured depth and steel grade required – is up about 50% in Canada and 35% in the US from a year ago. Canada’s price increases are higher because they started at lower levels. The order time for new casing is about three months in the US, which isn’t too bad compared to previous years like 2014.

Fortunately, the oil service sector’s equipment fleet won’t need that that much steel for new capital assets for now. But the metal component of wells, processing facilities and pipelines will cost more than at any time in recent history.

What the full impact of the rising cost of the total E&P supply chain will have on the capital programs of producers is as yet unknown. Be assured a 2022 CAPEX dollar will not go as far as it has in the past in terms of production growth.

This will, of course, sort itself out. Eventually, supply and demand will equalize and dampen oil prices. Until then, higher prices have provided producers the cash they need to pay more everything. This will eventually trickle through to suppliers and the labor force.

But the new twist to the historical – and now exaggerated – oilpatch cycles is decarbonization and its capital markets face, ESG investing. Finding and producing oil and gas is all about carbon, including the supply chain. What will this mean? How much different will that make the current recovery compared to those in the past?

Inflation, rising interest rates and central banks cutting back the extraordinary amount of liquidity pumped into the economy since 2009 will negatively impact the greater economy. So by default, an industry that runs on cash flow from commodities the world cannot live without looks pretty good. Even if it never returns to the frothy activity levels of years past.

North America, and US shale oil in particular, will not be materially increasing production thus negatively impacting the price of oil anytime soon.

E&P companies will, out of necessity, rediscover great respect for their suppliers.

And the service sector will enjoy the rewards it deserves for surviving the past seven years. Perhaps not bigger, but certainly much better.

David Yager is an oil service executive, oil and gas writer, energy policy analyst, and author of From Miracle to Menace – Alberta, A Carbon Story. Find the book to www.miracletomenace.ca.

Share This:

COMMENTARY: Hot Air and Fires in Ontario Mean its Climate Panic Time in Central Canada: That’s Never Good News for Supporters of Conventional Energy Production – Jim Warren