CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Dina Khrennikova and Olga Tanas

“Russian companies can ensure sustainable production until oil hits $15 to $20 per barrel,” Karen Kostanian, BofA’s Moscow-based oil and gas analyst, said.

Saudi Arabia has escalated a battle for industry dominance after the collapse of the OPEC+ alliance last week. The kingdom has slashed prices and announced a massive production increase. Russia’s Energy Minister Alexander Novak said his country’s industry will remain competitive “at any forecast price level.”

Novak is set to meet with key oil producers later on Thursday at the energy ministry to discuss the situation on the global market and their output plans.

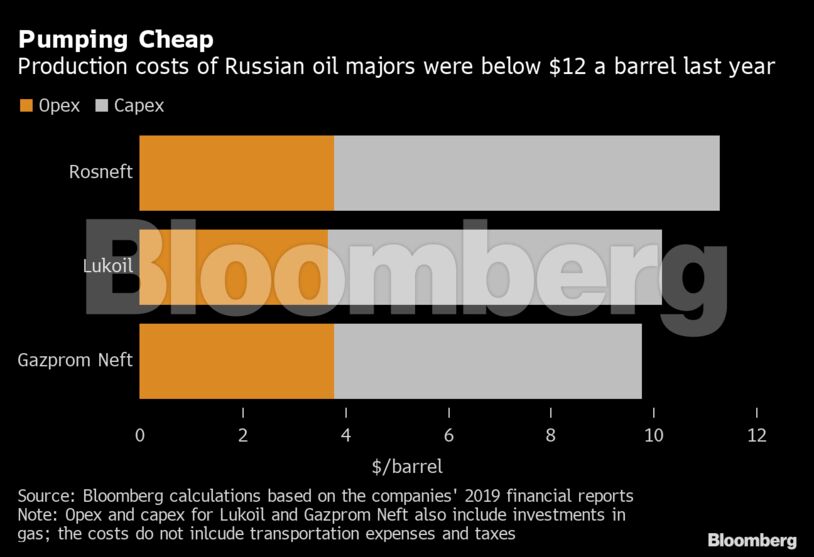

Three-Way Defense

It is the well-developed field infrastructure, as well as efficient railway and pipelines that enables Russian oil majors to operate at low costs. Last year, state-run Rosneft PJSC, Gazprom Neft PJSC and the top private producer Lukoil PJSC spent less than $4 to extract a barrel of oil, according to Bloomberg calculations based on the companies’ financial reports. Add to this around $5 to ship the barrel and $6-8 per barrel of capital spending, and you still get a barrel of oil for under $20.

The country’s fiscal system offers more protection. Last year, government levies formed the bulk of the remaining expenses for the Russian producers: the companies paid $34-$42 per barrel to the state in extraction tax and export duty, Bloomberg calculations show. However, Russia has a flexible fiscal system, which means as oil prices fall, taxes drop with them, said Dmitry Marinchenko, senior director at Fitch Ratings.

“Under the current tax regime, it is the Russian state that shoulders most of the risks associated with low oil prices,” Marinchenko said. With crude at $50 Russian producers pay more than 40% of their revenues in taxes, his calculations show. If the price falls to $25 the share of taxes declines to just around 20%, and in the $15-$20 scenario, the fiscal burden nearly disappears, Marinchenko said.

Finally, Russian producers, which earn part of their revenues in U.S. dollars and spend almost exclusively in rubles, are shielded by a flexible exchange rate. The ruble’s weakening to the dollar helped support the companies’ capital expenditures during the market’s previous plunge. As the ruble depreciated to 67.03 per $1 in 2016 from 31.85 in 2013, Russia’s top producer Rosneft grew its capex in rubles about 66%, investing in future production while its global competitors had to cut spending.

Familiar Threat

These factors help Russian companies through a short-lived price war, but they would start to feel some strain in a long battle.

The oil and gas industry is the single largest source of revenue for the Russian budget, generating around 40% of the total inflows and feeding Vladimir Putin’s multi-billion social-spending programs. The state budget envisions that all the costs over the next several years will be covered at oil slightly above $40. As a result, “oil falling below $45-50 almost inevitably leads to conversations about a higher tax load on crude producers,” Fitch’s Marinchenko said.

Back in 2016, when the government needed extra funds amid a bear market, it tweaked the oil-extraction tax formula to raise revenues, Evgenia Dyshlyuk, oil and gas analyst at Gazprombank PJSC, said. “If the state budget sees potential for a deficit, there is a risk of a similar move now,” she said.

The windfall-tax risks may emerge only if the bear market lasts for three to five years, Andrey Polischuk, Moscow-based analyst for Raiffeisenbank, argued. Price shocks lasting for several months will likely have no impact on the tax burden for producers, he said.

The industry’s resilience to pricing pressure won’t come without costs. With oil at $15-$20 a barrel, producers will need to cut their investment programs, undermining future output potential, and modify dividend policies, Kostanian said.

For now, the nation’s producers are staying positive. “It’s not the first time that crude falls,” Lukoil President Vagit Alekperov, who in the span of his 52-year oil career saw price levels of some $2 to $146, told investors this week. “We are used to operating in a volatile environment.”

Share This:

COMMENTARY: Carney’s Command of Canada’s Projects: What Gets Built, What Gets Blocked, and Who Decides – Ron Wallace