CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Many thanks to the Petroleum Services Association of Canada (PSAC) for the visuals in this article. Each week, XI Technologies scans for industry data, trends, and insights that have value for professionals doing business in the WCSB. If you’d like to receive our Wednesday Word to the Wise in your inbox, subscribe here.

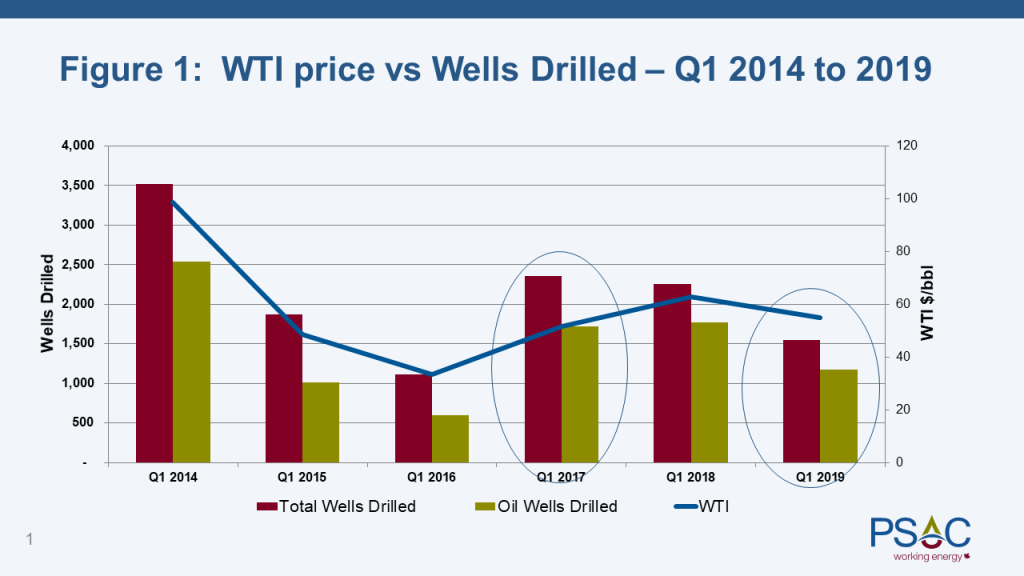

During last week’s PSAC Midyear Update Luncheon petroleum industry writer, energy policy analyst, and consultant, David Yager, presented recent PSAC (Petroleum Services Association of Canada) data and updated drilling activity forecast details for 2019. It came as no surprise to anyone present that drilling activity has been decreasing – PSAC’s updated 2019 forecast puts new drill activity a full 35 percent lower than Q1 2017.

This decrease in drilling activity comes despite higher WTI prices in 2019. As Figure 1 below shows, the growing disconnect between oil prices and wells drilled is proof that E&P companies are not prioritizing drilling programs.

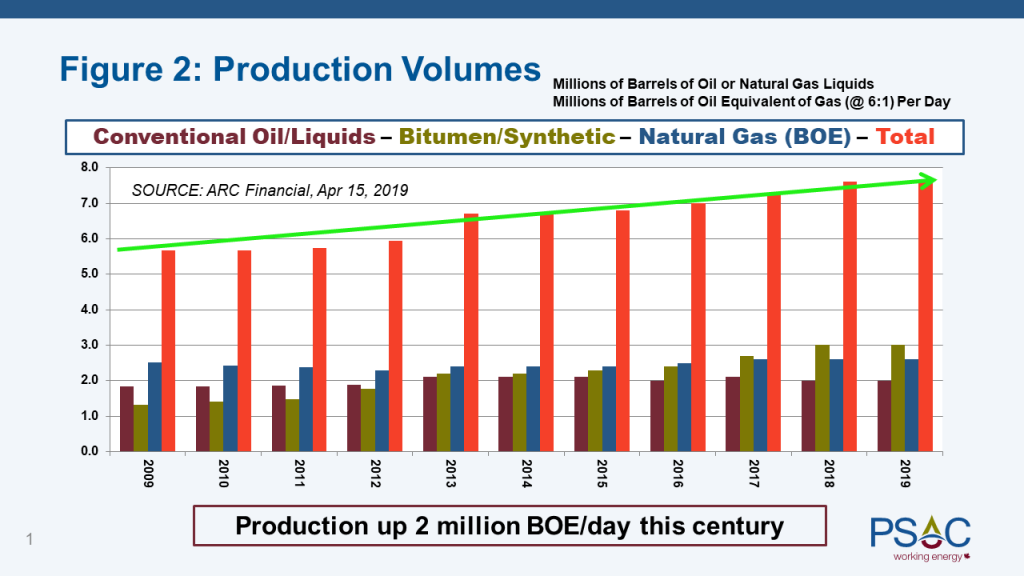

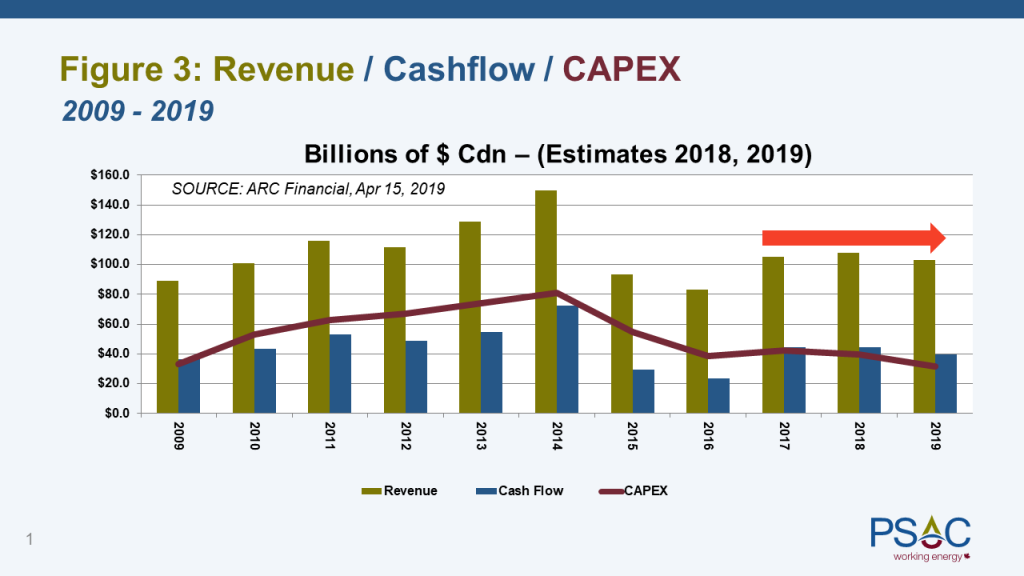

Certainly, western Canada’s lack of export pipeline capacity will continue to put downward pressure on new drilling activity. Even with the downward trend in drilling, Canadian production volumes have continued an upward trend (Figure 2), and industry-wide revenues and cashflow have also shown signs of recovery since 2017 (Figure 3).

So, in light of these hopeful positives (production, revenue, cashflow), could a shift in focus from drilling to decommissioning be an opportunity that would benefit both the petroleum services sector and the Canadian industry as a whole?

The Canadian petroleum services sector includes some of the world’s best technology, expertise, and skilled labour resources, all of which are currently under-utilized. Meanwhile, inactive and orphan well inventories in Canada are at their highest point ever and growing. The growth in inactive well liabilities has caused concern among the banking and financial community and, in the wake of the Supreme Court of Canada’s Redwater ruling earlier this year, lending redeterminations are becoming tougher and tougher.

While E&Ps are rightfully being cautious with their money, could this be an opportunity for them to invest some of the industry’s improving cashflow to address liability issues and clean up balance sheets? By shifting activity to decommissioning, abandonment, reclamation, and remediation, we could very well get inactive service sector equipment back in use, create employment for highly skilled western Canadian petroleum service workers, and spur economic activity that could help bridge the gap until new pipeline capacity is finally approved.

At XI’s April 18 roundtable on asset retirement obligations (ARO), senior executives from across the industry stated their commitment to addressing liability issues, but they need help from their banking and regulatory partners. As cashflows improve, finding a way to invest some of that into decommissioning would be a way for E&Ps to demonstrate their commitment. In exchange for proactively removing liabilities from their books and slowing the growth of inactive/orphan well inventories, companies should expect to be rewarded with more favorable liability ratios, timely and simplified licensing approvals, and a loosening of the lending constrictions imposed by banks in the wake of Redwater.

If pipeline capacity is the number one challenge facing our industry, asset retirement obligations are certainly number two. Unlike pipeline approvals, addressing the liability issue is completely within our own control. If we can resolve the latter by reducing inactive/orphan well inventories, solidifying E&P company balance sheets, and removing bank and investor uncertainty around ARO, just think how strong a position we might be in once Canada’s pipeline issue is resolved.

XI Technologies Inc. has been working extensively in the petroleum liability management field since 2013. We were the first to introduce LLR Analysis software to the Canadian industry. In 2018, we introduced the industry’s first ARO Management software, including a WCSB-wide standardized liability cost model, that allows you to evaluate, track, manage, and report on your company’s asset retirement obligations complete with audit trail. ARO Manager also allows you to perform scenario analysis to compare the impact of different asset retirement actions.

To learn more about the methodology behind XI’s ARO Manager download a presentation on Streamlining Your Corporate ARO Process. To see the AssetBook ARO Manager in action and compare your company’s ARO numbers with XI’s ARO calculation, request a personalized demo.

Share This: