CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

Oilfield Services Executive Advisory – Energy Policy Analyst

February 15, 2018

The prosperity, progress and prospects of the upstream oil and gas industry is inversely proportional to how often this business is in the news. Comparing what we read with what we do, it is clear our critics live in an alternative universe where facts are disconnected from reality.

The oil industry toils away producing essential hydrocarbons for a modern and mobile society that would not otherwise exist; spends billions on goods and services; hires tens of thousands of workers; and pays billions more in corporate taxes, payroll taxes and production royalties.

Meanwhile, external events that make this simple task more difficult increasingly verge on the absurd. The stupid B.C./Alberta political pipeline war. The lowest prices in the world for heavy oil and natural gas thanks to years of market access obstruction. A replacement for the NEB that appears as complex and unpredictable as the one it is alleged to improve.

These are the easy issues. Then there’s the end of life on earth and as we know it due to climate change blamed almost entirely on fossil fuels. An endless stream of news about all the things that are warming, melting, dying, drowning or changing because of carbon fuels. This is augmented by claims of the pending obsolescence of oil, coal and gas due to the mass adoption of environmentally benign energy sources.

Besides the fading morale of people who work in oil and gas, the collective impact of the foregoing is damaging investment patterns, at least in Canada. Rising taxes, low commodity prices and lack of market access have clobbered Canadian share values. Not investing in carbon-based energy is becoming a badge of honor among more investment institutions and pools of capital.

Then there’s politics. Except for Donald Trump, the political agenda in industrialized countries is increasingly dominated by those convinced saving the planet can only be achieved through enlightened legislation and more government. OECD countries, where environmental politics is most prevalent, comprise only 1.3 billion people or 17% of the earth’s 7.6 billion population. The other 83% is primarily concerned about access to cheap energy and, ideally, owning their first internal combustion engine.

With crude oil prices vastly improved, world oil demand growing and long-term supply in question, those who study oil markets are realizing the value of a barrel is far more likely to go way higher than lower in short to medium term. There should be well-founded reason for optimism.

But the relentless onslaught of negative news brought about by those who obviously live in a parallel universe where their primary source of energy doesn’t – or shouldn’t – exist, is taking its toll on confidence and optimism, historically as important as geology, drilling rigs and capital.

The rest of this article is dedicated to facts and questioning negative hysteria.

- Millions of barrels of oil equivalent per day including conventional oil and natural gas liquids, raw and synthetic bitumen, and natural gas converted to liquids at 6:1

- Revenue from production, billions of dollars

- After-tax cash flow available for reinvestment defined as revenue from production less direct operating costs including field operating, field processing, administration, royalties and taxes

- Change in after-tax cash flow from the prior year

- Estimates for 2017 and 2018

Compared to the dark days of 2016 the outlook for 2018 is positively glowing. Production is estimated to rise by 560,000 boe/day and revenue from all the oil, gas and liquids produced will be up $23.6 billion, nearly 29% higher than two years ago. Based on an average Edmonton oil price of $C67.05 per barrel and AECO spot gas of $C2.33 per GJ, after tax cash flow could be $16.1 billion higher than the dark days of 2016, a 61% increase. While this has not yet translated into major increases in drilling or capital expenditures, it will provide producers improved financial flexibility. While getting higher prices for goods and services will remain challenging, there will be more constructive negotiations about fair ways to share the pie than destructive struggles over the future of the customer or supplier.

The current pressure on heavy oil and gas prices is raising justifiable concerns. But 10.5 months or 88% of 2018 lies ahead. A bit early to panic.

Oil Supply And Demand In Balance For 2018 – International Energy Agency, February 13, 2018

Despite recent price softness the fundamentals look solid for 2018 and probably beyond. The IEA’s chart explains why oil collapsed in 2015 and why it will be more stable in the future.

Supply is the green line, demand the yellow line and the blue bars are the amounts by which “stock” or inventories rise or fall by quarter. Looking back to the fourth quarter of 2014 and the next two years, supply sharply exceeded demand resulting in steady inventory builds. Prices dropped sharply. But in Q4 2016 OPEC et al agreed to shut in 1.8 million b/d, demand kept rising and the rate of supply increases declined due to lower investment. With the exception of the current quarter, the trend will continue for the rest of the year. This graph depicts a level of stability absent for over three years.

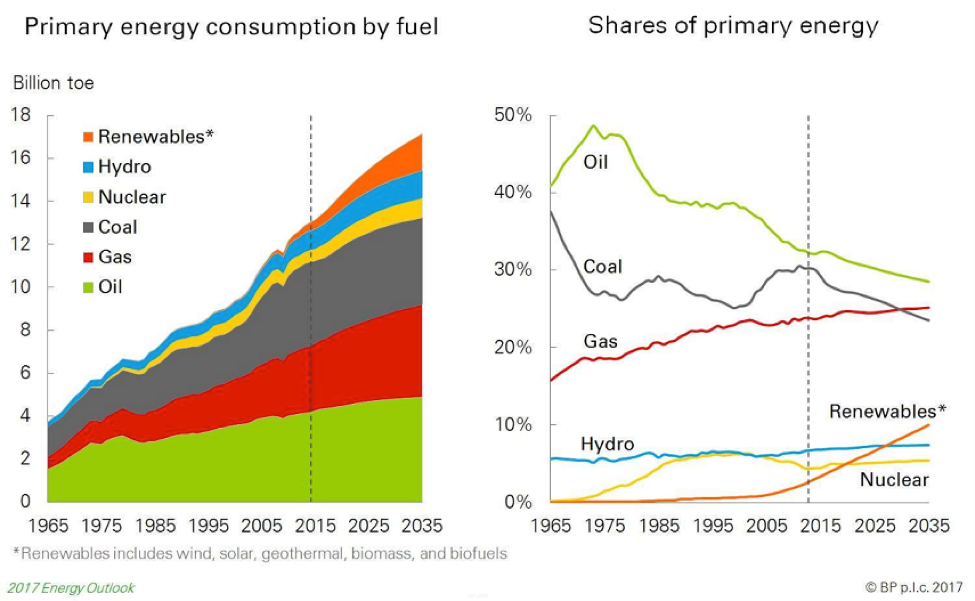

No End Of Oil Soon – BP World Energy Outlook 2017

British Petroleum publishes an annual review and forecast for global energy supply and consumption.

“toe” = “tonne of oil equivalent” or 7.33 boe, barrels of oil equivalent

BP sees no imminent threat to the future of fossil fuels for the 17 years to 2035 in the forecast period. Coal, oil and natural gas comprised 85% of the energy mix in 2015 but will only fall to 75% by 2035 as renewables grow. While the consumption of oil and coal will fall on a percentage basis, crude consumption is estimated by BP to be 111 million b/d in 2035, 16 million b/d higher than in 2015. Natural gas consumption will grow.

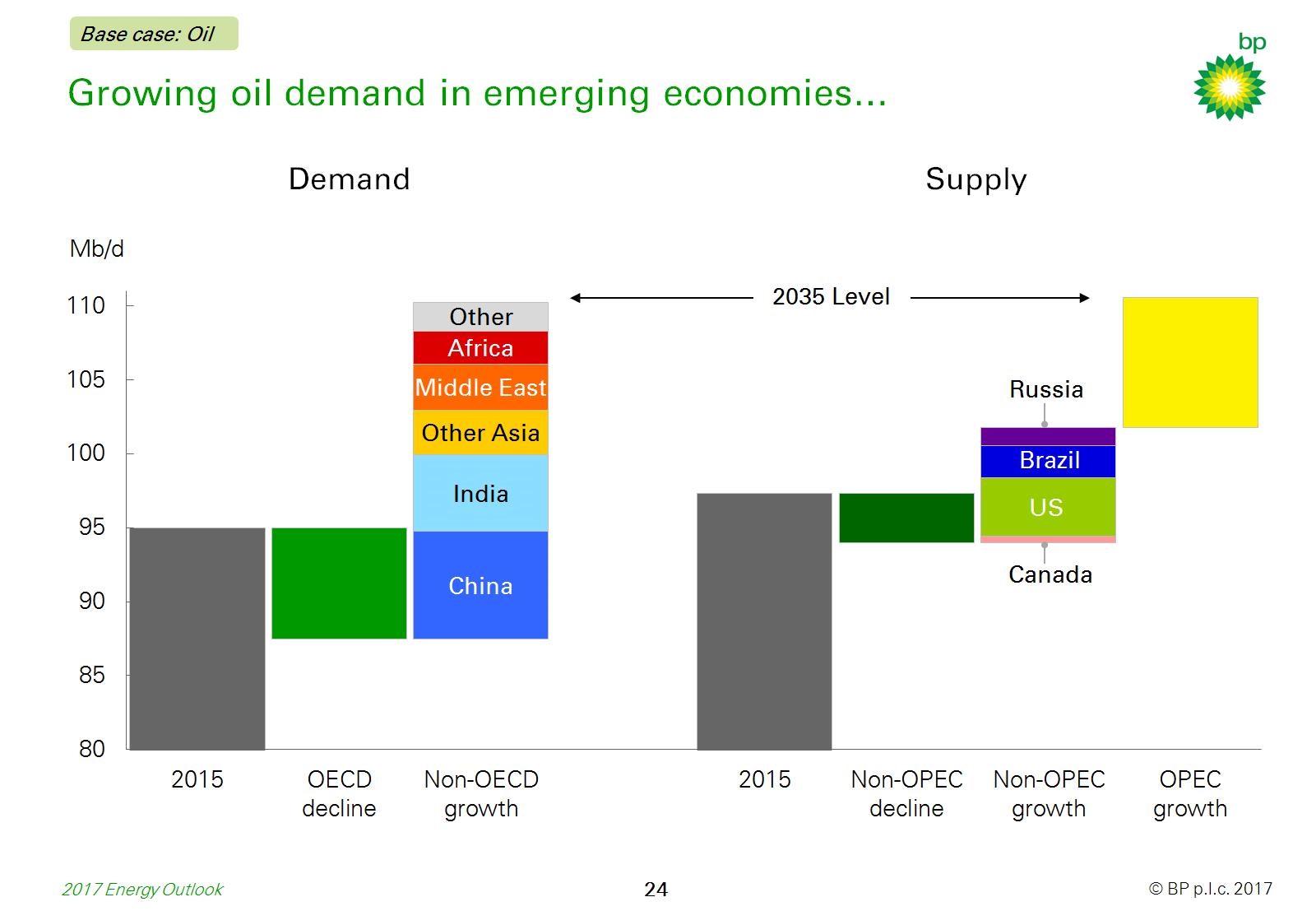

Of interest is where the growth in oil demand and supply will take place. Consumption will increase only in non-OECD countries. The increased supply will be split among Canada, the U.S., Brazil and Russia and OPEC. As OECD governments opine about and engineer a new world without carbon energy, the rest of the planet will need and buy more.

BP warns about the continued increase in carbon emissions stating, “The base case implies that carbon emissions from energy use grow throughout the Outlook rising by about 13%. This is far in excess of, for example, the IEA’s 450 Scenario which suggests carbon emissions need to fall by around 30% by 2035 to have a good chance of achieving the goals set out in Paris.”

BP also sees this oil growth continuing despite an explosion in demand for Electric Vehicles, rising from only 1.2 million on the road in 2015 to over 100 million in 2035. However, the total number of personal vehicles in service is forecast to double from about 900 million to 1.8 billion over the same period. EVs will most certainly have an impact.

But based on BP’s estimates, the current media and political frenzy over the obsolescence of the internal combustion engine and petroleum as a transportation fuel is dramatically overstated without major and currently unknown advancements in battery storage and non-carbon electricity generation technologies.

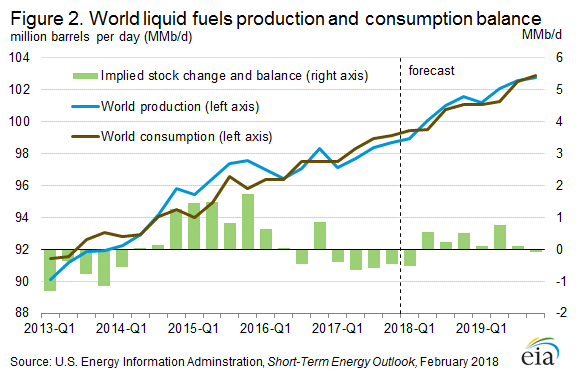

Demand to Exceed 100 Million B/D This Year – Energy Information Administration January 2018

World oil demand growth appears relentless this year and next. Washington’s EIA sees oil demand busting through 100 million b/d later this year and exiting 2019 at 103 million b/d. EIA inventory changes differ from IEA figures (above) primarily because of a more optimistic outlook for U.S. oil output.

When Liberal Prime Minister Jean Chretien signed the Kyoto Accord to great fanfare in 1997, world oil consumption was only 74 million b/d. As the anti-carbon movement has grown in the past 20 years, world oil consumption will be 35% higher later this year. Never let the facts ruin a good story.

Shipping Oil By Tanker Is Big And Has Never Been Safer – Clearseas.org.

In the period 1970 through 2014, the amount of oil shipped by tanker (light blue line, left axis) peaked in 1978, declined sharply through to 1985, then rose back to historic highs over the next 30 years. Simultaneously, due to advancements in tanker construction and navigation technologies, the number of large oil spills (shaded area) declined from over 100 in 1976 to zero in 2014.

The crux of B.C. opposition to Trans Mountain is increased oil tanker traffic which may contaminate the shoreline of the lower mainland. That oil tankers are a hot political issue is highlighted by Prime Minister Trudeau’s northern B.C. coast tanker ban as a 2015 election promise. This was restated when the federal government terminated the Northern Gateway pipeline in late 2016.

You can’t blame B.C. voters for questioning the wisdom of increasing tanker traffic in southern B.C. when the current Prime Minister banned tanker traffic in northern B.C. to protect the environment. Federal policy and pronouncements on this subject are inconsistent and unpredictable.

The world transports about 40 million b/d of crude oil by tanker and another 23 million b/d of refined products. The common measure for annual tanker loadings is MT or millions of metric tonnes. This equates to 7.3 million barrels of oil.

Clearseas.org was created by Clear Seas Centre for Responsible Marine Shipping, an independent research centre that promotes safe and sustainable marine shipping. It tracks petroleum and products currently shipped by tanker in Canada. At present 4.6 million b/d oil travels into, through or near Canada by tanker, 16% on the Pacific coast. Most of the Pacific oil travels from Alaska to the U.S. On the Atlantic coast the figure is 3.9 million b/d which includes oil imports for central and eastern Canada and production from the east coast offshore. About 1.8 million b/d travels down the St. Lawrence River and through the Great Lakes.

Of the 300,000 b/d currently being shipped by Trans Mountain, most is consumed domestically. About 1/3 is exported by tanker. The Trans Mountain expansion will increase tanker traffic from the western terminus by about 590,000 b/d or 13% of the current Canadian total.

B.C. Has Long Opposed Resource Development

Problems with resource development in B.C. are not new. Forestry and mining has been under attack for decades. B.C. has been fiddling with or obstructing all attempts to ship any form of hydrocarbons from Canada’s west coast since the first proposals were made late last decade.

A 1996 collection of essays titled Policy, Politics and Government in British Columbia carried the following in the first chapter Value Conflicts in Lotusland – British Columbia Political Culture; “…lifestyle images have come to predominate. B.C. is ‘lotusland’, where workplaces close early on Fridays and open late on Mondays to accommodate skiing, hiking and the other activities of fitness fanatics. The province has spawned the most vigorous environmental movement in the country, the activities of which have led to dramatic confrontations with loggers and miners”.

Remember, environmental “activists” in B.C. were spiking trees to protest logging near Clayoquot Sound on Vancouver Island 25 years before Premier Horgan cooked up yet another way to fulfill last year’s election promise to delay and obstruct Trans Mountain.

The enormous quantities of gas unlocked by horizontal drilling and hydraulic fracturing in northeast B.C., combined with growing production from aggressive expansion of Alberta’s oil sands, created great interest in exporting LNG and oil from Canada’s west coast. Northern Gateway was conceived from 2002 to 2006 and an application for development was filed in 2008. The Trans Mountain expansion plan was filed four years later.

In 2012, then B.C. Premier and Liberal Leader Christie Clark, had already outlined that province’s “five main conditions” for accepting the construction of the Northern Gateway link from Edmonton to Kitimat, a project approved by the NEB in 2013 and the federal government a year later. This project was officially terminated by Prime Minister Justin Trudeau in late 2016.

In February 2013, in the Liberal government’s throne speech, there were so many LNG projects on the books the government confidently predicted a windfall for the provincial treasury. The Vancouver Sun reported, “Projections for the fund rely on the introduction of a new LNG tax to be applied in addition to existing royalties. With all these measures in place, the government is projecting the fund will collect a minimum of $100 billion over 30 years.”

At one point there were 18 proposed LNG export projects or related pipelines. The province created a special department to wisely manage and distribute the wealth. But at the same time it was plotting how to spend all the money, the government demanded unrealistic if not impossible ceilings on carbon emissions. While always sounding supportive, the seemingly endless list of taxes, regulations, delays and political posturing has all but paralyzed this once-promising resource.

The current low natural gas price in western Canada can be directly linked to B.C.’s mismanagement of the LNG export file which resulted in the inability of industry to complete or even start construction on a single project before commodity prices collapsed in late 2014.

Today only one of the smaller projects is active conducting what it calls “Pre-Notice To Proceed” activities, Woodfibre LNG on the site of an old pulp mill at Squamish. Meanwhile, U.S. LNG exports commenced in 2016 and continue to grow.

The Trans Mountain battle is hardly the biggest problem. Low bitumen prices have more to do with TransCanada’s Keystone pipeline leak in November and restricted access to rail transportation on short notice.

But as the old saying goes, all politics is local. Nobody in B.C. cares what happens because of the massive tanker traffic by comparison on the opposite end of the country.

Strength Amid Confusion and Chaos

While there are problems galore, this is not new. The industry is fundamentally stronger than two years ago. Climate change policies and alternative energy sources will have no impact on global hydrocarbon demand or prices in the short to medium term. All the problems the Canadian industry faces are self-inflicted by our fellow citizens and the politicians we elect.

Perhaps this is because the industry cannot fathom how carbon-fuel haters can fuel up with refined bitumen to drive to an oil-sands protest while ignoring the hypocrisy of their behavior. Or use electricity created by burning coal or natural gas to go on-line and support anti-carbon politicians and initiatives.

Oil’s critics live in an alternative universe. We share the same planet but not the same grasp of reality. Regrettable, but not in any way the end of our industry.

About David Yager – Yager Management Ltd.

Based in Calgary, Alberta, Canada, David Yager is a former oilfield services executive and the principal of Yager Management Ltd. Yager Management provides management consultancy services to the oilfield services industry in a number of areas including M&A, Strategic Planning, Restructuring and Marketing. He has been writing about the upstream oil and gas industry and energy policy and issues since 1979.

See David Yager’s Corporate CV

List of David Yager’s Consulting Services

David Yager can be reached at Ph: 403.850.6088 Email: [email protected]

Share This:

COMMENTARY: Hot Air and Fires in Ontario Mean its Climate Panic Time in Central Canada: That’s Never Good News for Supporters of Conventional Energy Production – Jim Warren