CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

As the first anniversary of Russia’s invasion of Ukraine on February 24, 2022 comes and goes, world oil markets are in complete disarray and still sorting themselves out.

And will be for some time.

The primary blame for oil market chaos falls on Russia, the world’s third largest producer.

And it’s more than petroleum. Russia is second to only the U.S. in natural gas production. Its output was triple that of Iran in the number three spot.

Plus coal, minerals, fertilizer, and many of the the other resource essentials of modern civilization. It even affected Ukrainian food exports.

The other causes of turmoil are the push for energy decarbonization at any cost, the fossil fuel divestment movement, low commodity prices leading to years of underinvestment in new supplies, the pandemic lockdown, and COVID-19s lingering effects.

The International Energy Agency (IEA) warned in 2021 about energy shortages or price spikes because of underinvestment. A BNN Bloomberg report October 13 wrote, “The pandemic, which led to a near-record low new oil and gas investment in 2020, has intensified the trend, the IEA said. ‘If demand remains at higher levels, this would result in tight supply in the years ahead, raising the risks of higher and more volatile prices.’”

Volatile it is, and that’s doesn’t mean high. The closing price of WTI on Friday February 17 was US$76.56. That’s ten dollars lower than the average price for the first 37 trading days of 2022 before the Russian tanks rolled in Ukraine, which was US$86.81.

The WTI average closing price for the first 38 trading days of 2023 was only US$77.81, also well below the pre-invasion average for the same period.

Having lower oil prices in this period of market disruption is not intuitive.

Here’s the Canadian perspective.

**********

Storage tanks at Hardisty, Alberta. Photo courtesy of Enbridge Inc.

On February 16, the Battle River Alliance for Economic Development invited me to Hardisty as their guest speaker. The title of my presentation was Alberta and the Future of Fossil Fuels.

Hardisty is the true Oil Capital of Canada. Just look around. In a relatively small area Hardisty is home to the third largest collection of oil storage tanks and caverns in North America, with a total capacity of 38 million barrels.

The largest is Cushing, Oklahoma, at 85 million barrels. Number two is the Louisiana Offshore Oil Port which holds 67 million barrels.

In the Q&A that followed, one of the questions was, “Do you think there will be further expansion of oil storage capacity at Hardisty?”

So began the longest answer to the shortest question of the evening.

What made it complicated is that it was asked in one of the major oil epicentres of our country. In the nation with the world’s third largest proven reserves. Home of the oil the world wants and needs.

If there is any place on the planet that should be increasing oil production and storage right now, it is Canada.

But we aren’t because of Canadian politics and unprecedented oil market turmoil.

**********

Daniel Yergin has been a thought leader on energy geopolitics since publishing his first book The Prize in 1991. Yergin, now 76, has been in high demand for the past year. He wrote the following in the Wall Street Journal three weeks after the U.S.-led group of countries introduced sanctions on Russian oil production December 5.

“Europe’s ban on Russian oil, combined with the U.S.-generated ‘cap’ on Russian oil prices, marks the end of the global oil market. It its place is a partitioned market whose borders are shaped not only by economics and logistics but also geopolitical strategy.”

Yergin continued, “The oil market became truly global only three decades ago with the collapse of both the Soviet Union and the barriers created during the Bolshevik Revolution a century earlier. That coincided with the economic rise of China, which turned an energy self-sufficient albeit poor country into the world’s largest importer of oil. While there have been some restrictions in the global market since then – notably sanctions on Iran and Venezuela – economic efficiency has largely determined how barrels flow around the world.”

The master plan was to starve Putin’s war machine of money. The price cap the west would try to enforce was US$60 a barrel. Yergin wrote, “The Kremlin has assembled a ‘shadow’ armada of 100 or more second hand tankers that will attempt to evade the ban on Western tankers. Chinese and Indian companies can provide some of the missing insurance, but that will all leave a significant gap.”

But in this chaotic market with previously unknown challenges and actions, forecasting is fraught with peril.

A Bloomberg article February 17 was titled, “Russia’s Shadow Oil Tanker Fleet Becomes Everyone Else’s Problem.” It turns out Russia has invested US$2.2 billion in a fleet of oil tankers that commodity giant Trafigura estimates could total 600 ships, 400 of which are oil tankers. It reads “’Dark Fleet’ purchases of tankers surged on Russia sanctions. Over 100 vessels were sold to undisclosed buyers in 2022.”

In December I wrote the following.

Analysts have concluded this price cap will have little impact on Russia’s oil revenues because Asian countries like India and China are thrilled to purchase more oil at lower prices. What Russia loses on price will be offset by volume.

Quoting unnamed US Treasury officials, Reuters wrote, “…the price cap is ‘institutionalizing’ current market discounts, arguing that plans for the cap were responsible for price declines over the past several months…”

The U.S. opposed a complete EU Russian oil boycott because it would drive up U.S. prices. The article states the “…true motivation after March (2022) has been primarily to preserve Russian oil flows…if there was an oil price spike, not only will it hurt us economically and politically, but it’ll damage Western support for Ukraine. As the G7 formed the plan, India and China have snapped up heavily discounted Russian oil, and are expected to continue big purchases outside the price cap, moves endorsed by Treasury Secretary Janet Yellen.”

At the G20 meetings in Asia last month, Yellen’s position was clear. An Arab News headline read, “Oil prices fall; Yellen says price cap on Russian oil will benefit China.”

Whatever is said or written about Russia and oil, the main thrust of western policy for the past year has been to keep the price down and leave the long-term consequences for another day.

Some European producing countries have introduced windfall profit taxes on oil producers to subsidize consumer prices. Although the windfall profits are gone at current prices, taxes are much easier to introduce than remove.

A big factor in capping oil prices has been the U.S. drawing down its Strategic Petroleum Reserve.

On January 7, 2021, the SPR held nearly 640 million barrels, a level that had been the same or greater for most of this century.

Just before the Russian invasion, the SPR was down to 582 million barrels. As of February 10, 2023, the SPR was at 372 million barrels, 213 million barrels lower than 12 months earlier or about an average of 587,000 barrels per day.

That’s a lot of oil. Considering how much global oil markets gyrate when 100,000 b/d enters or leaves the market, this has had a material dampening effect on prices.

U.S. energy policy under President Joe Biden has been confusing and contradictory. His first act when sworn into office in 2021 was to cancel the Keystone XL pipeline to prohibit more awful Canadian oil sands from entering the U.S.

His most recent move is to resume oil imports from Venezuela. Oilprice.com reported February 17 that, “U.S. To Receive 3 Million Barrels Of Venezuelan Crude Oil in February.” That’s about 100,000 b/d courtesy of Chevron. Other operators trying to get a similar exemption from previous embargoes include ConocoPhillips, Repsol and ENI.

In the past 18 months Biden has tried to get more oil from OPEC and negotiate a new deal with Iran. At the same time he has frequently berated U.S. producers like ExxonMobil for not investing enough in increased domestic production.

Oil market turmoil has not yet created a material change in policy in western countries. As Yergin noted, it was the emergence of China and other Asian countries that drove up world prices early this century resulting in the all-time high of US$146 in July of 2008. In the old, borderless, international market.

Today the largest markets for oil demand growth – China and Russia – are served at lower prices from a major dedicated supplier – Russia.

This is what the fracturing of global oil markets means, at least for now.

**********

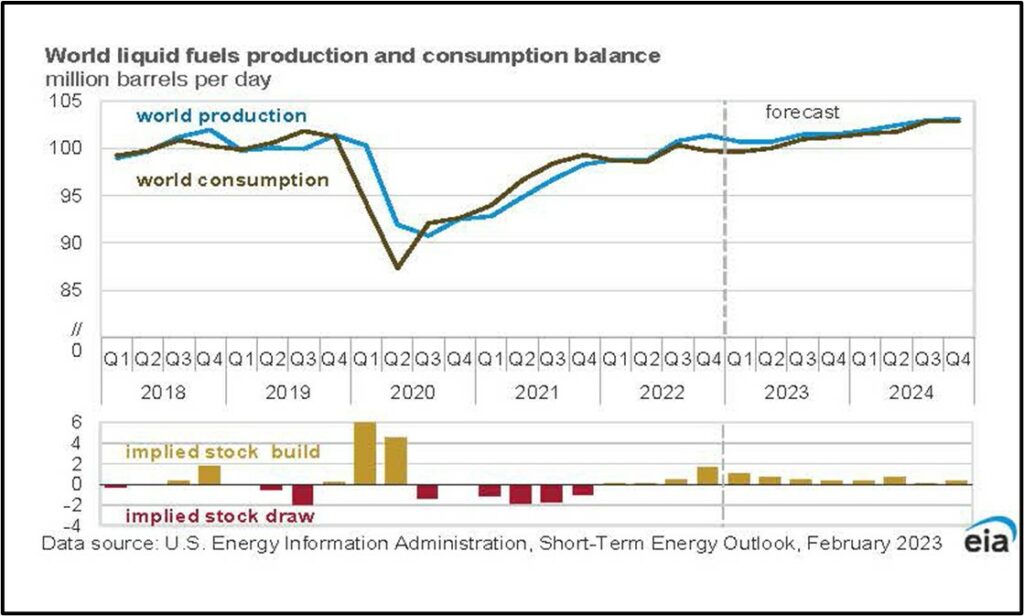

With China re-opening, how long will low prices last? The February 2023 report from the Energy Information Administration shows continued growth in oil demand from the next two years.

EIA sees the world exiting 2022 with supply outstripping demand, then increasing together through 2023 and 2024. Consumption will be 102 million b/d when 2023 ends, and 103 million b/d a year later. The yellow bars at the bottom show steady inventory builds.

But where will the supply to create the “stock builds” come from?

While OPEC+ claims to be withholding crude from markets, how much incremental production capacity actually exists?

Because the countries that have solved the world’s oil shortages the last two times prices skyrocketed are out of the game.

It was Canada and the U.S. adding 10 million b/d from American light tight oil and Canadian oil sands from 2008 to 2020 that collapsed world prices in 2015.

This was significant because in 2016 total consumption was only 96 million b/d.

Canadian oil production increased somewhat in 2022, primarily from increased capacity from existing oil sands facilities. While there will be some production growth associated with the completion of TMX in 2023, there will be no material increases so long as current federal policies stay in place.

Despite the belief that U.S. production would rise sharply again in 2022 because of higher prices and the historic quick response in light tight oil regions like the Permian Basin, growth was muted due to issues with supply chains, capital markets, and federal policies. Geology is also proving to be a factor after years of intensive drilling in the major American light tight oil basins.

The EIA reports America produced 11.6 million b/d in January of 2022 and exited December at 12.0 million b/d, well below 13 million b/d reached in early 2020.

Capital spending will increase in both countries in this year. But a lot of this is directed at natural gas and higher prices for goods and services to help the oil service sector rebuild its supply chain in terms of labor and equipment.

When oil prices spiked in the 1970s, it was also non-OPEC countries that saved the day and collapsed prices. The U.S. developed Alaska’s North Slope and the Trans Alaska pipeline which added 1.8 million b/d by 1988. An exploration and development boom in Europe’s North Sea added 3.7 million b/d between 1973 and 1988.

Remember, at that time world demand was only 60 million b/d. These two sources added over 9%.

The countries that cooperated to rebalance world oil markets twice in the past are now the leaders in the anti-fossil fuel movement.

Demand destruction was a factor in re-balancing oil markets in the 1970s because the price increased by a factor of 10 between 1972 and 1980. Fuel efficient cars emerged as part of the solution, as did significant investments in nuclear power.

The high prices of 2022 were supposed to cause demand destruction, but the lingering aspects of COVID and global supply disruptions had a much bigger impact than price.

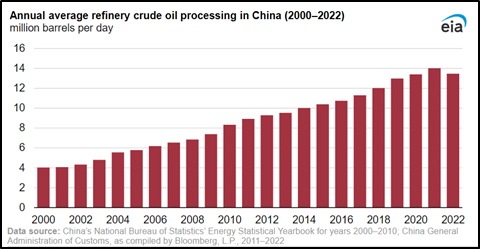

Source: EIA Today In Energy February 21, 2023

This chart shows China’s oil refinery output declining in 2022 for the first time this century. But the cause was pandemic lockdowns and reduced exports of refined products, not a fundamental change in Chinese consumption. Can’t use much gasoline if you’re confined to your apartment.

With the Chinese economy re-opening, all forecasts (OPEC, EIA, IEA) see oil demand rising in 2023 and again in 2024.

This is not intuitive either, based on the continuous news reports for the past ten years which assured the world that oil was a sunset industry. Labelling fossil fuels “stranded assets” was designed to reinforce this message among investors.

Although renewable energy and electric cars are intended to reduce fossil fuel demand, there is also population and income growth to deal with. While low-carbon energy is at the highest levels in history, so is world population and GDP.

This was reflected in OPEC’s oil demand forecast to 2045 last year, which saw continued growth in petroleum consumption for the next 22 years.

OPEC predicted no increase in oil demand in OECD countries. But the 6.7 billion people who don’t live in the world’s wealthiest nations will need more fuel.

The spread between what OPEC’s customers want and what the IEA tells the world it must do to prevent climate disaster is huge. The difference in 2050 is over 70 million b/d.

Somebody is dead wrong.

**********

With politics driving the bus, not economics, few in the privately owned producing sector know what to do next. “Wait and see” is currently a very sound strategy.

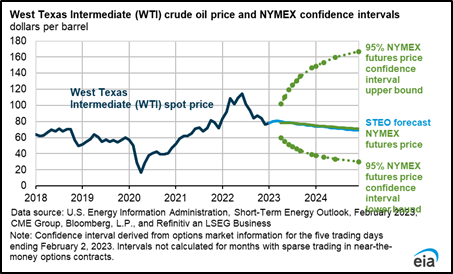

Source: EIA February Short-Term Energy Outlook February 2023

The EIA’s price spread for the next two years is illustrative. While the official forecast sees a decline in WTI to 2025, the range based on the “NYMEX futures price confidence interval” is US$130 a barrel. This is based on WTI options for the five-day period preceding the report.

Data like this causes investors and boards to study, not spend.

So in the short term, producers will increase output as cheaply as possible and pay down debt. Long term commitments for new supplies are out of the question until clarity and stability returns.

And until Canadian producers figure out what federal emissions reduction compliance will cost, and who is going to pay for it.

No, Hardisty. There will be no requirement to increase storage capacity anytime soon.

But the pre-COVID, climate-driven playbook won’t work either.

Whatever we’re told we’re supposed to do, demand for oil isn’t going anywhere anytime soon.

And if supply doesn’t increase, prices will rise. And the economic recovery will take longer because one of the most powerful forces affecting everything remains the cost of energy.

The cost of energy is a very powerful force. Ultimately oil market confusion will correct itself, even if politicians are reluctant to admit they were wrong and change course. Canada will be at the table because the world will demand it.

And Hardisty will again add storage tanks.

But not yet.

David Yager is an oil service executive, energy policy analyst, oil and gas writer, and author of From Miracle to Menace – Alberta, A Carbon Story. Learn more at www.miracletomenace.ca

Share This: