CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Gas is back in a big way

Follow CEC on Facebook CEC Facebook

Follow CEC on Twitter CEC Twitter

Rejoice.

The public discussion about Alberta’s oilpatch is all oil all the time. But for years gas paid the bills for producers, service companies and Alberta’s treasury.

Data by the Canadian Association of Petroleum Producers (CAPP) shows that from 1955 to 2020 (the last year available) 173,299 gas wells were drilled in Alberta. The total for oil is only 75 per cent of that number – 126,931 – split between 101,127 for conventional oil and 25,804 for bitumen.

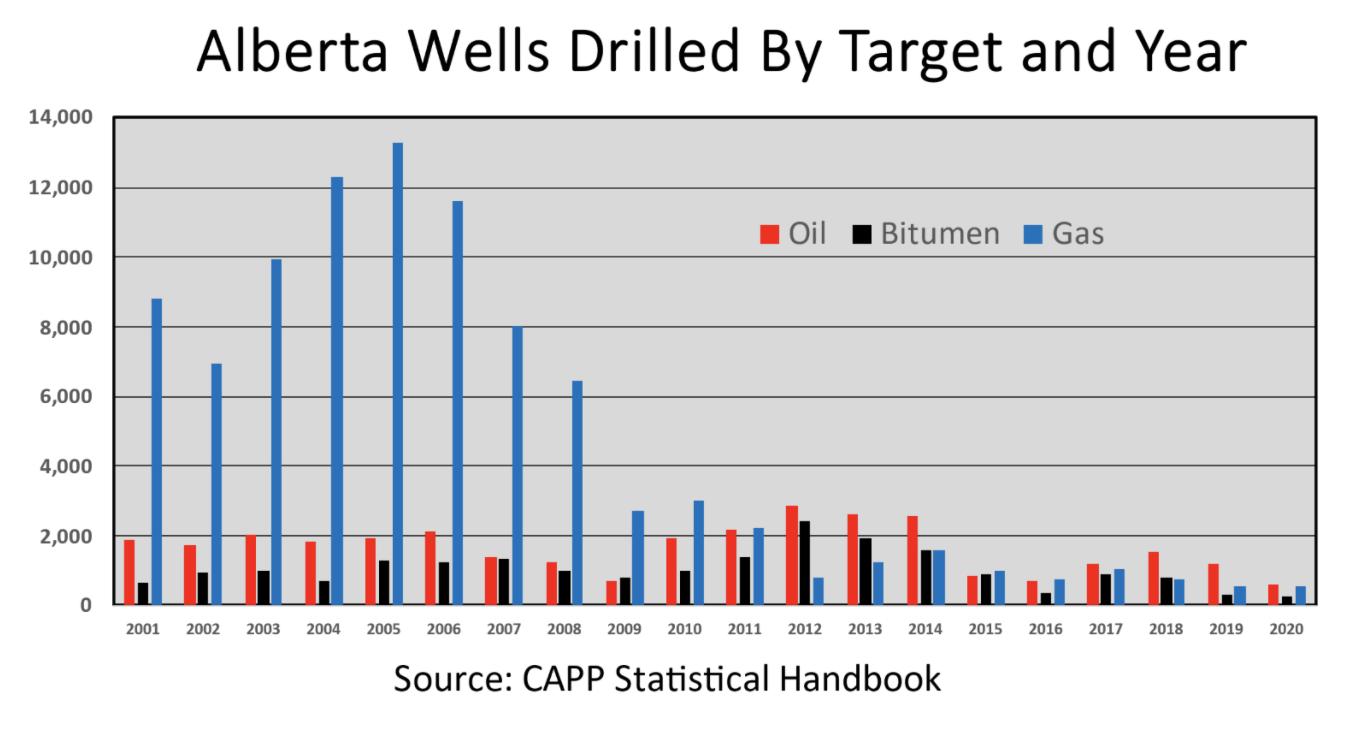

This century, gas dominated drilling until the shale gas boom in the U.S. completely altered North American gas markets starting with the Barnett Shale 20 years ago. This is how new drilling looked from 2001 to 2020.

Two major events occurred from 2005 to 2010. The U.S. shale gas revolution exploded and unlocked enormous resources much closer to markets, which hurt Alberta prices and export volumes. The biggest game-changer was the Marcellus shale play in the northeast U.S. This eventually eliminated the U.S. east coast as one of Alberta’s most valuable export markets.

The other was the oil sands boom, which commenced after oil prices began rising again in 2003. This attracted capital to massive oil sands mining and in situ recovery projects.

By 2012 conventional gas drilling had dropped to the lowest level in 20 years. Using horizontal drilling and hydraulic fracturing, prolific tight shale basins like the Montney looked more attractive. This caused a significant and costly retooling of the traditionally gas-driven services sector. Much of the equipment that once created employment for thousands was rendered obsolete.

Also overlooked is the impact of natural gas on the provincial treasury. After several years of surpluses, in 2009 Alberta returned to budget deficits. Except for 2014, the province hasn’t balanced its books until this year.

While Alberta’s finances are routinely linked to the price of oil, analysts must include natural gas. A 2021 Fraser Institute study examining Alberta’s revenue, spending and deficits back to 1966 never even mentioned it.

Big mistake. The Alberta government maintains a spreadsheet tracking non-renewable resource income since 1970. Here’s the data for past 51 years.

| Source | Current Dollars* | Per Cent |

| Natural Gas & By-Product Royalties | $98.3 Billion | 44% |

| Conventional Oil Royalty | $68.2 Billion | 31% |

| Oil Sands Royalty | $54.8 Billion | 25% |

| Total Production Royalties** | $221.3 Billion | 100% |

*Not corrected for inflation

**Not including coal royalties, bonuses from land sales, rental income and fees, less royalty credits

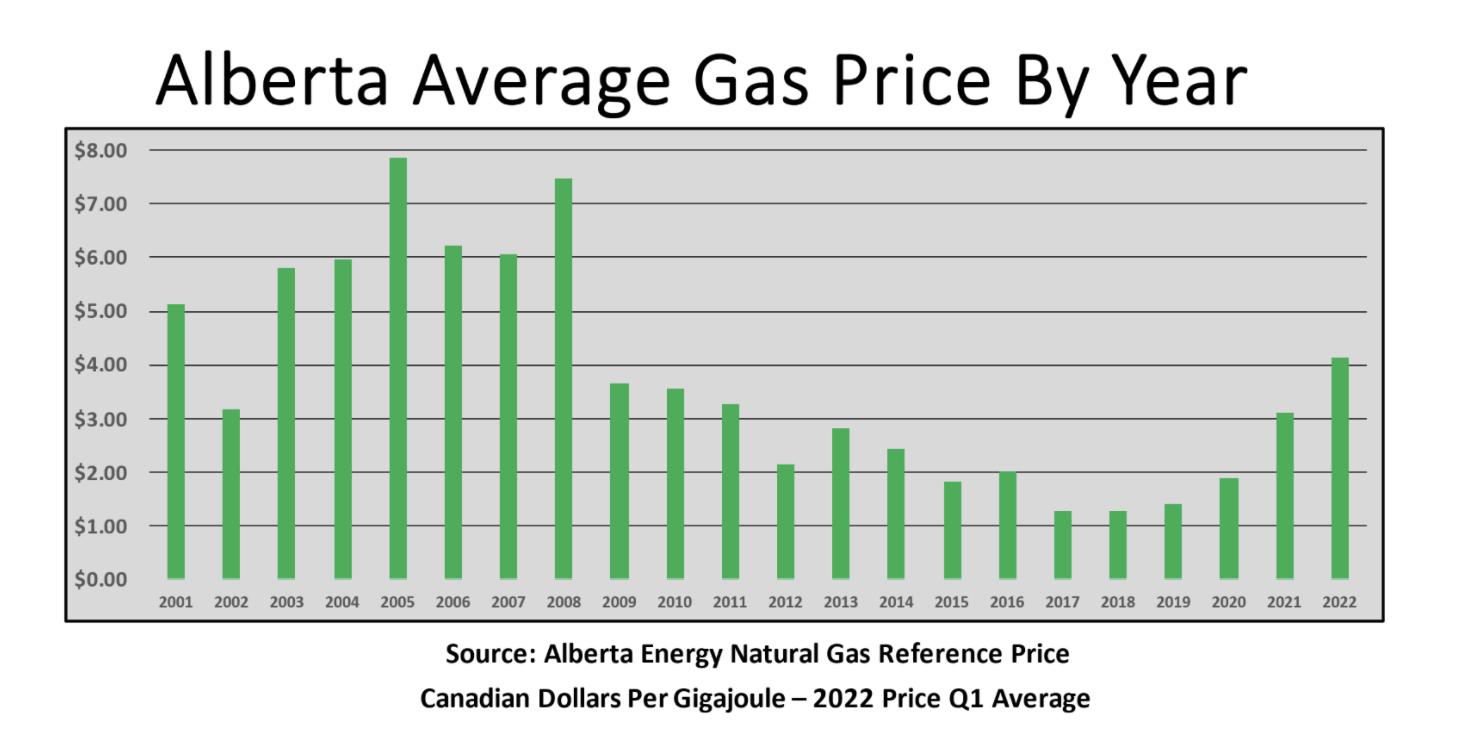

The best years for natural gas royalties occurred in the first decade of this century, when both prices and export volumes were up. This chart shows the average annual price of Alberta gas this century.

Once on production, natural gas has relatively low operating costs. But when prices collapsed, so did inflows to Alberta’s treasury. It was primarily natural gas royalties that allowed the government of Ralph Klein to pay off Alberta debt, put $17 billion in the newly created Sustainability Fund, and issue “Ralph Bucks” in 2005, $400 cash for every Albertan.

Of the total natural gas royalties collected by the province in 51 years, $55.2 billion or 56% came in the ten years from 2001 to 2010.

The challenging years were from 2012 to 2021 when gas revisited the “fuel of the future” prices of 1991. Total royalties for this ten-year period were only $7.4 billion, one billion less than in 2006 alone.

Thousands of wells were shut in, producers went broke, property taxes and surface leases went unpaid, and ownerless wells poured into the Orphan Well Association. Producers and regulators were routinely labelled as irresponsible. Critics seldom linked the problem to collapsed gas prices.

The great news is that gas is making a big comeback. The average price in 2021 exceeded $3 for the first time since 2011. For the first three months of 2022 it was $4.31, over three times the average price for all of 2018.

World events are reshaping global gas markets. Shortages in Europe and Asia have caused huge growth in U.S. LNG exports. In the same way that new shale gas production in Pennsylvania caused Alberta prices to fall, exporting gas off the continent is helping all gas prices rise.

Benchmark U.S. Henry Hub gas recently exceeded US$9 for the first time since 2008. In April Alberta gas averaged C$6 and above. On May 25, the closing spot price was C$7.91.

The impact on drilling and spending is already apparent. More rigs are drilling for gas. Fixing shut-in wells that were previously uneconomic is creating jobs in the services sector.

It should get better. Assuming Coastal GasLink pipeline opponents don’t succeed, LNG Canada will be exporting gas in 2025. Multiple new LNG projects are either pushing ahead or being revived. Even the emission-fixated federal government has blessed more LNG development in response to global events.

This is just the beginning. Natural gas is the feedstock for Alberta’s nascent blue hydrogen and planned ammonia expansions. Methane’s role in fertilizer and petrochemical manufacturing has been integral to Alberta’s economy since 1941.

Natural gas is back, and it’s big. Except for recently, it always has been.

David Yager is an oilfield service executive, oil and gas writer, and energy policy analyst. He is author of From Miracle to Menace – Alberta, A Carbon

Share This:

COMMENTARY: Mark Carney’s Rhetoric Doesn’t Match Reality: McTEAGUE