CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

![]()

Research and development-related tax strategies can provide flexibility now, when you need it most

BY MICHAEL BOSDET

The current economic climate is a catalyst for M&A activity in the oil patch. But with the sheer volume of complex tax-related issues to be dealt with in such transactions, it’s easy to understand how the government’s Scientific Research and Experimental Development (SR&ED) tax credits could be overlooked. The benefits of claiming SR&ED go beyond the 23.5 to 41.5 percent combined Canada-Alberta tax credit. Instead, the benefits could—and should—be strategically integrated with a company’s overall M&A strategy.

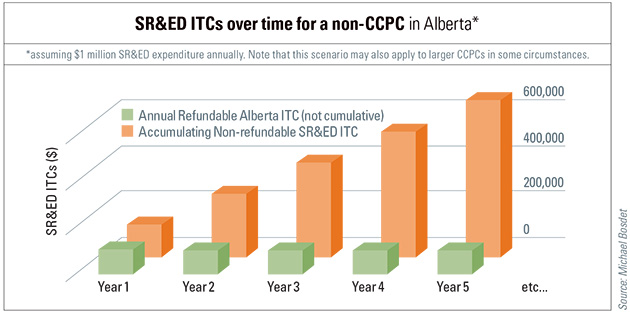

SR&ED is an incentive program intended to foster the advancement of science and technology in Canadian business. Federal SR&ED investment tax credits (ITCs) earned in a fiscal year can be either refundable (cash), or non-refundable (tax credit). In the case of the latter, the benefit may be carried back three years, or forward up to 20 years and applied against taxes payable. SR&ED ITCs from Alberta are refundable for all for-profit corporations.

Why, then, are some public companies quick to dismiss SR&ED, believing that they have no use for non-refundable tax credits? This perspective overlooks the universally refundable tax credits from Alberta (10 percent of qualified expenditures up to a maximum of $400,000 in ITCs), and is an overly simplistic opinion that could significantly impact corporate valuation.

This is because, for mergers and acquisitions, the SR&ED ITCs can be used after the change of ownership, provided the acquirer is a for-profit entity in the same or similar business. The SR&ED ITCs have real value as they can be directly applied to the acquirer’s taxes payable, or carried forward to a future year. The deemed yearend resulting from the acquisition of control burns one of the carry-forward years so, for example, if there are 15 years remaining on the acquired company’s SR&ED ITCs at the time of acquisition, the acquirer can carry these forward for up to 14 years. Thus, for companies that are or could be a potential acquisition target, the benefits of claiming SR&ED go beyond the current cash infusion from refundable ITCs; any non-refundable ITCs will increase valuation. Depending on the level of SR&ED occurring in the company, the impact can be significant.

An additional benefit of filing a SR&ED claim is that it can generate a “SR&ED qualified expenditure pool,” as long as the expenses are not needed to immediately reduce taxable income. This pool can be applied in much the same way as a non-capital loss pool. The key difference is that the amounts captured in the SR&ED pool can be carried forward indefinitely. Like the SR&ED ITCs, the SR&ED pool can also be used after the acquisition, providing additional value.

Notably, the SR&ED ITCs and SR&ED tax pool are in play only where the company itself is acquired. Asset acquisitions do not allow the acquirer to benefit from the accumulated ITCs or SR&ED pools; where there is SR&ED associated with a divested asset, any accumulated SR&ED ITCs remain with the original company. That said, if the acquiring company continues to perform SR&ED on its newly acquired asset, it would be entitled to claim the associated expenditures from the time of acquisition.

Companies poised to acquire another can apply ITCs directly against taxes payable—immediately or in the future—or can use non-capital loss pools ahead of the newly-acquired, non-expiring SR&ED pool. Current market conditions make the risk of expiring loss pools a more pressing concern in the near term. But having a backstop such as the SR&ED pool can prove prudent in the long run.

About TSGI Corporation

TSGI is a SR&ED consultancy dedicated exclusively to assisting organizations headquartered or operating in Western Canada to fund their research and development (R&D) activities. We do this by ensuring that our clients receive their full entitlements under the SR&ED (Scientific Research and Experimental Development) tax credit program and also by connecting them with other sources of technology funding.

Contact TSGI Corporation

TSGI Corporation Headquarters

400, 1122 4th St SW | Calgary, AB

www.tsgi.ca

Michael Bosdet

403.451.3373

[email protected]

For information on how to subscribe to Alberta Oil Magazine CLICK HERE

Share This: