CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Donald Trump didn’t miss a beat, unlike the Kansas City Chiefs who missed the game. Aboard Air Force One, or was it TrumpForce One…I forget, he announced that all imports of Steel and Aluminum would be subject to a tariff of 25%. As curiosity always gets the better of me, I wondered what exactly the composition of these imports looked like.

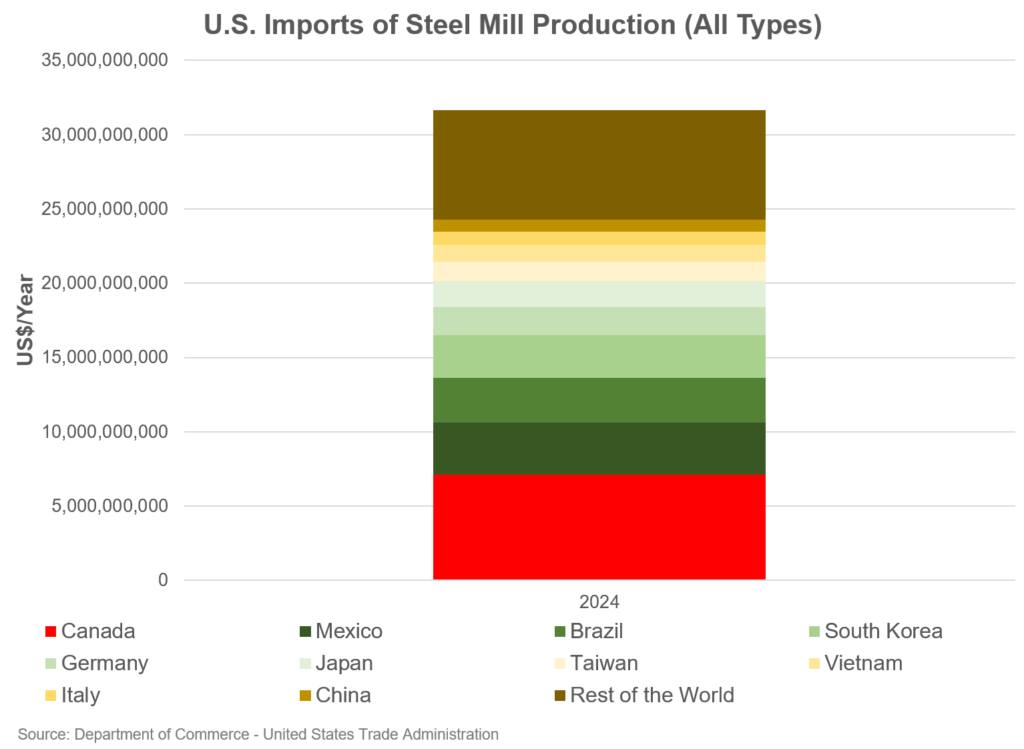

According to the Department of Commerce, imports of steel from steel mills (all types – flat, semi-finished, pipe and tube, long, stainless and other) by the United States accounted for almost US$32 billion and Canada was the single largest exporter to the U.S. at US$7.1 Billion or 23% of all imports. The top 10 exporters represented US$24.3 billion of imports or 77% of all imports.

According to the USGS, United States steel consumption has been trending around 93 million tonnes per year, and when factoring the ins (consumption) and outs (exports) of the U.S. economy, it appears as though the country relies on ~12 million tonnes, net, of steel imports a year versus the ~26 million tonnes it imported in 2024. To frame this, the United States has been on a fairly flat trajectory of producing ~81 million tonnes of steel per year, so the imports are critical to their overall economy.

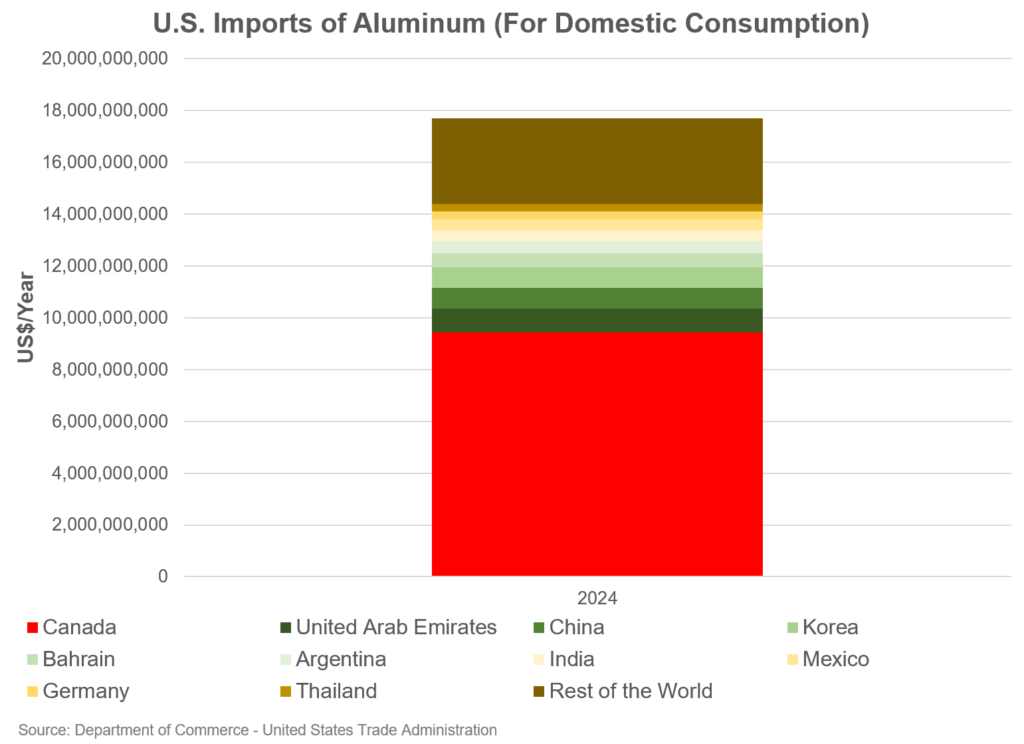

For aluminum, in 2024 the United States imported US$17.7 billion of product, with Canada representing the lions share of that at US$9.4 billion, and the top 10 importers represent US$14.4 billion or 81% of all imports.

Steel production is focused primarily in Ontario and Quebec, while aluminum production is essentially all from Quebec, with the one exception being a smelter in Kitimat, British Columbia.

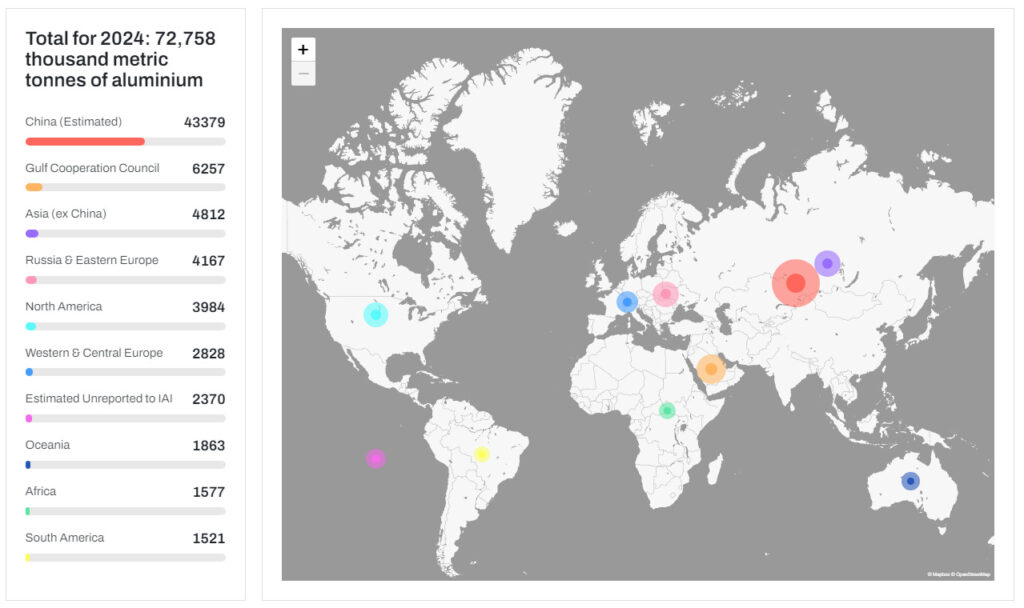

If you are curious where global Aluminum production comes from, the chart from the International Aluminum Institute is quite helpful. In short, China is the elephant in the room, accounting for 60% of global production in 2024. Zooming in, you can see that North America accounted for 3,984 thousand metric tonnes in 2024.

What is interesting is that Canada produces materially more aluminum than the United States (~4x) so I am not exactly sure why the U.S. would put a tariff on aluminum when there is no obvious domestic source to replace it. Moreover, the U.S. has been in a pattern of retiring facilities and current operational domestic nameplate capacity is 1.36 million tonnes per annum, though the country only producers at ~50% of that. In terms of options, it seems as though the only option that is apparent to U.S. consumers is to pay more for something you cannot source locally. Moreover, the supply chain will see inflationary effects as these tariffs get passed along on value added goods.

As I hope you can see, the latest salvo of tariffs that Donald Trump has no basis of truth, despite what he may post on Truth Social. The truth is, this will be a continual weapon that the President of the United States will use in order to achieve his domestic policy goals, whatever those may be. As I said in a prior post (War Footing or Surrender Monkeys? The Trump Tariff Threats Should Be Our Economic Call To Arms) no longer can the United States be viewed as a trusted partner and we have a limited time to change course.

Thanks for reading William’s Substack! Subscribe for free to receive new posts and support my work.

Share This:

COMMENTARY Joe Oliver: Fool Me Once, Shame on You. Carney and the Liberals Trying to Fool Me Four Times? Seriously?