CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager

July 25, 2022

Continuous volatility in oil prices is now part of the business.

This year WTI has ranged from US$75.99 to US$123.64 on March 8. The closing price July 22 was US$95.09, down nearly 25% from its highest price since 2008 reached shortly after Russia invaded Ukraine.

With the exception of one day in mid-March, this is the lowest closing price since the war in Eastern Europe began.

There are endless moving parts in today’s financial markets. Ellen R. Wald., Ph.D. is an author and energy analyst who writes a weekly column for investing.com. Wald’s summaries on oil are topical and succinct.

After oil fell US$20 a barrel from June highs, the July 7 title was “Oil: Possible Global Recession And Its Effect On Demand Is Key.”

- Fears of recession which would impact demand. This was assisted by a Citibank forecast that saw oil headed for US$65 a barrel if there was a global recession.

- High demand for Russian oil and how the western sanctions that tried to take 3 million b/d of Russian oil taken off markets won’t materialize thanks to India and China.

- Discounts on sanctioned oil because the Russians were selling their oil below market prices to keep volumes up.

A week later WTI was on the wrong side of US$100 for the first time since April. On July 14 Wald’s commentary opened, “3 Uncertainties Driving Volatility In Oil Markets And How To Trade Them.”

- Bullish demand growth projections from OPEC see crude consumption exiting 2023 at 105.4 million b/d with an average of 103.9 million b/d for the year. The more conservative EIA forecast 101.7 million b/d for next year, the IEA 101.3 million b/d.

- Saudi Arabia’s actual oil production capability has been in question for some time. After President Biden’s visit that country stated it could only increase output to 13 million b/d and that would take five years.

- US oil production growth would continue with the EIA seeing domestic output reaching 12.2 million b/d in the back half of 2022. American output peaked at 13 million b/d in early 2020 then fell to below 10 million b/d a year later.

On July 21 Wald wrote about Russia. “Energy Markets Didn’t React As Expected To Russian Sanctions.”

- Re-routing of oil and gas flows. As Wald predicted two weeks earlier, Russian oil is still reaching markets, just going to different places.

- Russia’s oil and gas revenues are up. What may be lost on volume has been gained on price.

- Europe’s need for Russian energy trumps politics. Although Europe had originally vowed to quit buying Russian hydrocarbons by the end of 2022, this was easier to say than do. Wald wrote, “Expect that Europe’s desire for energy will continue to outweigh politics.”

But what oil’s daily drama doesn’t cover is the big picture.

**********

Demand

The most frequently overlooked factor affecting oil demand is its lack of elasticity. While most products and commodities are price sensitive, crude oil is not one of them. There are no substitutes for most petroleum fuels and by-products.

OPEC’s comprehensive crude oil supply/demand forecast to 2045 was released last fall. OPEC focuses on the non-OECD world, where 83.5% of the population lives. Of today’s 7.9 billion earthlings, only 1.3 billion live in the wealthiest countries. The primary political activism in the climate change movement – and all the major policies, programs and subsidies to accelerate decarbonization – take place among only 16.5% of the population.

Looking ahead to 2045, OPEC estimated the world’s population would grow by 1.7 billion to 9.6 billion. But 96% of this growth would occur outside of OECD countries.

OPEC figured that by 2045 oil consumption would be 108.2 million b/d, or 8.2% higher than 2019 levels.

Transportation consumption will increase by 4.9 million b/d dominated by aviation at 2.8 million b/d. Road transportation is up 1.6 million b/d, and marine 0.4 million b/d.

Industrial use will rise by 3.9 million, primarily petrochemicals.

The only material decline – 1 million b/d – will come from using less petroleum for electricity generation.

It’s a big world but the modern media is focused on local issues.

To understand what everyone else is thinking, pollster IPSOS does a monthly study titled “What Worries The World” which surveys over 20,000 people in 27 countries.

The COVID-19 pandemic dominated responses for the past two years, but now the trends are returning to normal. In July’s report the five biggest issues were inflation at 38%, poverty and social inequality at 33%, crime/violence and unemployment tied at 26%, and financial/political corruption at 23%.

Nearly two-thirds believed their countries and governments were on the wrong track. Fifty-nine per cent of Canadians agreed.

Climate change is an issue for only 16% of total respondents. This varies tremendously. The only non-OECD countries above this level were Saudi Arabia and India at 18%. Countries at 10% or less were Mexico, Hungary, Colombia, South Africa, Malaysia, Chile, Turkey, Israel, Peru, Brazil and Argentina. Israel was at 5%, Brazil 3%.

A common message has been that EV adoption will eventually crush the biggest market for refined crude, which is gasoline. But this is proving to be more aspirational than practical due to supply chain issues ranging from rare metals for motors and batteries and the capacity of automobile manufacturers.

This doesn’t factor in the enormity of the expansion and restructuring of the electricity grid to keep these EVs powered. The significant value of petroleum’s existing transportation, refining and distribution network – and the cost of replacing it – is frequently overlooked in the mission to replace oil.

ExxonMobil CEO Darren Woods recently said that by 2040, all new cars could be electric. In the current market remarks like this causes oil prices to flutter.

But this is 18 years away. 21st century capital markets have an attention span that rarely lasts 18 minutes.

How much a global recession will temper oil demand depends on price. The 2008/2009 financial crisis caused consumption to fall by 1.5 million b/d after oil reached hit US$146 in July 2008. Corrected for inflation that was US$169 a barrel.

By 2011 oil was back over US$100 and oil demand rose to 3.2 million b/d above 2008 levels.

The sheer might of 7.9 billion people making their own decisions on how to survive another day is a powerful force. This makes incumbent fossil fuels impossible to easily dislodge or replace. For billions of people, paying more for low carbon energy for the greater good is a non-starter.

**********

Drilling

How oil prices can do down without drilling going way up is the most illogical characteristic of current oil markets.

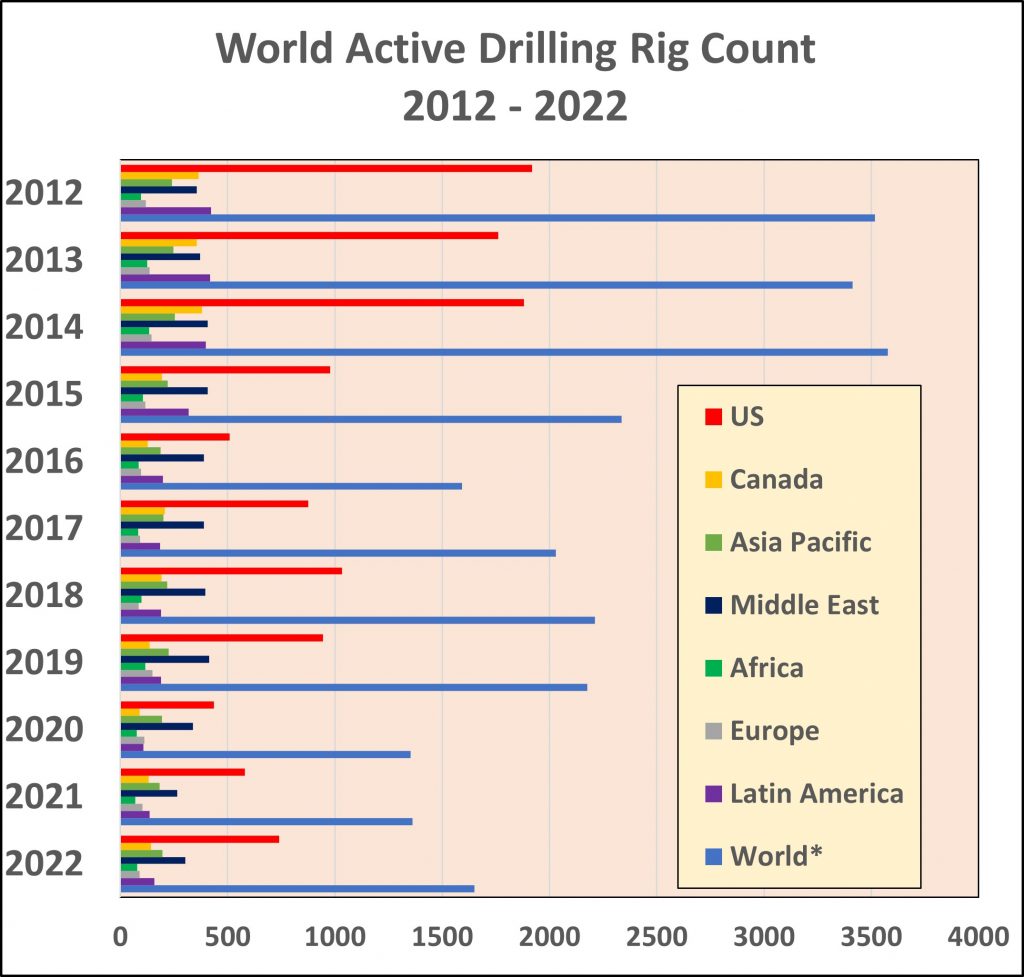

The above chart from Baker Hughes represents average annual world active drilling rig counts since 2012.

The average in the first six months of 2022 was 1,650, 46% of the 3,578 active rig average in 2014. The regions where drilling has declined the least are the Middle East and Asia Pacific, at 75% and 77% of 2014 activity respectively.

While the US appears to be making a comeback, the first half of 2022 only averaged 739 rigs, 39% of 2014 levels. Canada is at 38%. Outperforming the US and Canada using this measurement are Latin America 40%, Europe 62% and Africa 58%.

Capital budgets remain a fraction of what they were. ARC Energy Research Institute reports that in 2014, capital investment for Canadian producers was 121% of after-tax cash flow. This year the current estimate is only 29%.

The countries that moved the needle to help collapse oil prices in 2015 were Canada and the US. From 2009 to 2020 they added 10 million b/d to world output. This made them victims of their own success.

These countries have since elected governments committed to ensuring this won’t happen again.

Regardless, oil service giants Halliburton and Schlumberger see better times ahead for drilling.

In its outlook comments following the release of its second quarter financial results Halliburton said, “As we look at the second half 2022, Halliburton remains sold out (of frac capacity)” CEO Jeff Miller believes North American spending will grow 35% this year, and “…equipment capacity for 2023 will be tight.”

“Longer term, we believe the international markets will experience multiple years of growth. In short, this cycle has been nothing like prior cycles. This means any economic slowdown will not solve the structural oil undersupply problem.”

Schlumberger concurred when it released its Q2 numbers. “Despite near-term concerns over a global economic slowdown, the combination of energy security, favorable break-even prices, and the urgency to grow oil and gas production capacity is expected to continue to support strong upstream E&P spending growth. Consequently, we are witnessing a decoupling of upstream spending from near-term demand volatility, resulting in oil and gas activity growth in 2022 and beyond.”

Daily vacillations in oil prices are not related to the big picture fundamentals which are based on strong cash flow from production and limited reinvestment due to lingering capital market issues, obstructive politics in key markets, and internal and service sector capacity challenges.

Producers are no longer dependent on external debt and equity capital. Government policy challenges remain, but many countries and administrations have changed course significantly in the past year compared to the prior five.

Drilling will continue to ramp up as industry capacity improves and as more governments accept that the current energy crisis won’t be solved with windmills and solar panels.

**********

Declines

Too much is written about oil without referencing decline rates and reserve replacement. There’s only so much recoverable petroleum in any reservoir. Production starts high then declines continuously until the well or pool is no longer economic.

Average decline rates for conventional reservoirs is about 8% compounded annually. Light tight oil reservoirs unlocked with hydraulic fracturing commonly have decline rates of 30% or higher.

The only major producing area that enjoys what could be classified as zero decline rates is oil sands mining and, to a lesser degree, oil sands in-situ thermal recovery. In both cases the reserve base is so massive the producers keep “stepping out” a bit further and effectively never run out of oil.

Paradoxically, in recent years the most dependable source of future petroleum is the one the world has grown to despise.

Creating the current energy crisis wasn’t easy. A lot of now-questionable decisions were made by a lot of people.

In late 2019 ExxonMobil did an investor presentation in New York looking at decline rates and reserve replacement out to 2040. The company indicated that without continued investment, in 20 years the world be short about 80% of its estimated oil requirements and 70% of its natural gas.

Quoting the 20C warming scenario from the International Energy Agency, maintaining oil and gas output for the next twenty years would cost US$21 trillion.

That’s US$1 trillion a year. According to the IEA, the highest investment year ever was 2014 at US$780 billion. By 2019, the figure was below US$500 million. In 2020 it was only US$328 billion, the lowest in recent history.

Whatever markets are attempting to tell us in 2022 about the future of oil, unless there is some quick miracle substitute for petroleum or the economy collapses entirely, a continued shortage of oil is assured without significant increases in investment in new supplies.

The IEA and OPEC have been warning about this for years. The political classification of Russian oil as worse than other sources – if only for western consumers – makes all the world’s petroleum supply challenges more difficult to manage.

Natural gas also faces decline issues. In its first quarter commentary released May 18, the report from Leigh R. Goehring and Adam A. Rozencwajg was titled, “The Gas Crisis is Coming to North America.”

As gas markets become increasingly globalized thanks to LNG, the authors point out that the shale gas miracle that the US has enjoyed is increasingly mature and subject to the same laws of nature as oil.

The Barnett Shale is now 20 years old, Fayetteville 17. These were followed by Marcellus and Haynesville. Significant contributions of associated gas came from the major light tight oil plays in the Bakken, Eagleford, DJ, Permian and Anadarko basins. The last major gas play was the Utica shale.

The impact was incredible with US gas output almost doubling. They wrote, “In 2000, US dry gas production was 52.6 bcf/d and the shales produced little. Today, production is 94 bcf/d with nearly 73 bcf/d, or 80%, coming from the shales.”

But high decline rates are unavoidable. While the Marcellus and Haynesville are holding their own, Barnett and Fayetteville are two-thirds below their peak 2012 production rates.

The authors conclude, “The world has enjoyed a decade of cheap, abundant energy and nowhere has that been truer than in US natural gas. We consume nearly as much energy via natural gas as we do via crude oil, although it is usually an afterthought. The rest of the world is in the midst of an acute gas shortage that has grabbed everyone’s attention. We believe the same is about to happen in the US — much faster than anyone realizes.”

An S&P Global news report July 21 was titled, “Faltering US gas production growth defies build in rig counts, drilling activity.” While US gas prices fell when the Freeport LNG export facility went down in June, the recent gain in US gas prices has been based on supply concerns.

It was thought that US gas production would rise to 97 bcf/day by Q4, but S&P wrote, “The growth anticipated by many analysts and market observers, though, has failed to materialize.” This has caused US gas futures to rise 20% in recent days.

In 2011, half of America’s 1,775 active drilling rigs targeted gas. Since 2013 only 20% of the active rigs on average have drilled for gas.

**********

There are two oil industries in 2022.

There is the one in the news every day, where commodities and share prices gyrate with every utterance of a vast array of market forces and players.

Then there’s the other, which supplies the energy and by-products the world cannot live without.

Fortunately, most readers of this article work in the latter.

David Yager is an oil service executive, oil and gas writer, energy policy analyst, and author of From Miracle to Menace – Alberta, A Carbon Story. Find the book to www.miracletomenace.ca. He is President and CEO of Winterhawk Well Abandonment Ltd. which has commercialized a new casing expansion technology for improving annular wellbore integrity.

Share This: