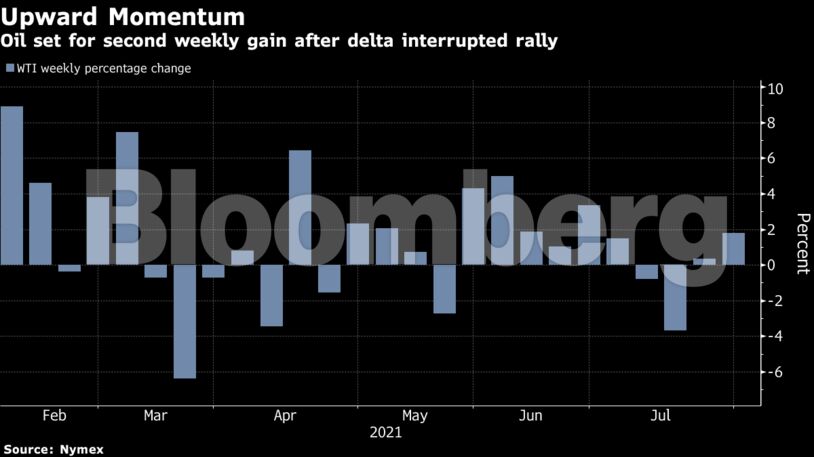

(Bloomberg) Oil headed for a second weekly gain as signs of tighter supplies helped assuage fears over the resurgent pandemic’s threat to demand.Futures held above $73 a barrel in New York, up 1.9% this week even as some countries renewed curbs on movement amid a spike in Covid-19, most notably in Southeast Asia. Prices were supported by a further plunge in U.S. crude inventories — the ninth in 10 weeks — and signals that the Federal Reserve will continue measures to support the economy.There’s confidence the oil market will continue to strengthen, with Royal Dutch Shell Plc chief Ben van Beurden predicting “a strong recovery in demand” as economic activity picks up again.

With prices ending the month little changed, crude’s gains since the start of the year stand at more than 50%. Other commodities have hit their highest levels in a decade.

“Despite the numbers of new cases remaining at a high level, the oil market no longer appears to be viewing the issue of the delta variant with quite the same alarm as it was at the beginning of last week,” said Carsten Fritsch, an analyst at Commerzbank AG in Frankfurt. “The oil market has learnt to live with the virus.”

Get the Latest Canadian Focused Energy News Delivered to You! It's FREE: Quick Sign-Up Here

Prices

West Texas Intermediate for September delivery lost 0.3% to $73.43 a barrel on the New York Mercantile Exchange at 10:09 a.m. London time, after climbing 1.7% on Thursday.

Prices are up 1.9% this week.

Brent for September, which expires Friday, slipped 0.2% to $75.91 on the ICE Futures Europe exchange, after rising 1.8% on Thursday.

The grade is up 1% in July, a fourth monthly increase.

Its prompt timespread was 97 cents in backwardation.

Traffic data shows deserted streets in Thailand and snarls of vehicles in India.

Japan Petroleum Exploration Co. has become the latest foreign investor to exit the oil sands with the sale of its Hangingstone site to Trafigura-backed Greenfire Acquisitions Corp.

CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

INSIGHT: $312.4 BILLION REASONS Why Albertans Deserve a New Deal to Reform Federal-Provincial Fiscal Relations – Lennie Kaplan