CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Saket Sundria and Alex Longley

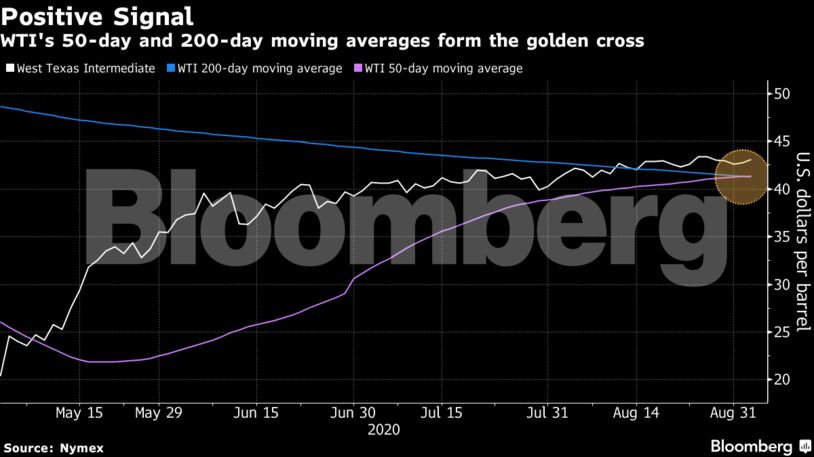

Oil rose for a fourth month in August but has struggled to sustain a rally above $43 a barrel as major economies continue efforts to contain the coronavirus outbreak. While a weaker dollar, sliding U.S. stockpiles and a surge in equity markets have supported crude, there are still concerns that a slow demand recovery is going to limit further gains.

“The positive tone is being sustained amid hints of a bigger-than-expected drawdown in U.S. oil inventories,” said Stephen Brennock, an analyst at brokerage PVM Oil Associates. “Market players are currently riding a wave of optimism though it could come crashing down at any moment.”

| Prices |

|---|

|

American crude inventories — a key metric used to gauge global supply — have slipped from near record highs in June, helped partly by Saudi Arabia limiting shipments to the country. Cargo data show that deliveries in the week ended Aug. 28 dropped to what could be the lowest in decades.

See also: OPEC Supply Boost Tempered by Quota Cheats’ Extra Cuts

The longer-term outlook remains more uncertain. Demand may take a hit over September and October as Chinese imports ease with state-issued quotas for independent refiners dwindling following a crude buying spree earlier this year.

Share This:

COMMENTARY: Taxes and Regulations Will Increase the Cost of Producing New Energy In Alberta, Making it Less Competitive Than the US – Jack Mintz