CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Heesu Lee and Alex Longley

Oil is still set for a weekly gain because of shrinking American crude stockpiles and signs of progress on a possible U.S.-China trade deal. Following days of mixed messages, the shape of an OPEC+ deal emerged, but with few details. Russia, which has complied with its production quota for just three months of this year, had its proposal to exclude a very light oil called condensate approved on Thursday, potentially giving it space to keep pumping above its target.

“What they do in the second quarter remains unclear, on paper it is still heavily oversupplied,” said UBS Group AG analyst Giovanni Staunovo, referring to the entire group. “It will all come down to how they communicate it at the end.”

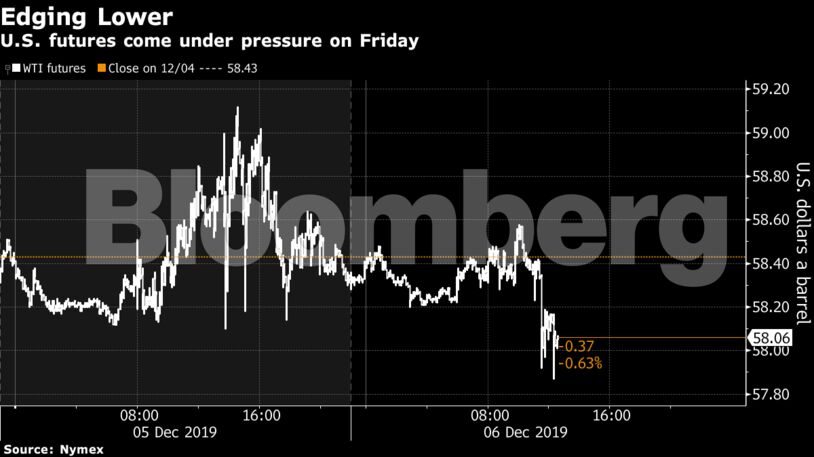

West Texas Intermediate for January delivery fell 15 cents to $58.28 a barrel on the New York Mercantile Exchange as of 7:55 a.m. local time. Brent for February settlement lost 3 cents to $63.36 a barrel on the London-based ICE Futures Europe Exchange. The global benchmark traded at a $5.16 premium to WTI for the same month.

See also: OPEC, Aramco Control Headlines More Than Oil: Liam Denning

OPEC+ agreed to curb its output quote by 500,000 barrels a day. But some analysts think just a reduction would largely be symbolic, as it simply formalizes the deeper cuts the group has been making for most of this year, rather than taking additional barrels off the market. The group is set to have further full ministerial meetings in March and June, a delegate said.

| Other oil-market news |

|---|

|

Share This: