CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Saket Sundria and Grant Smith

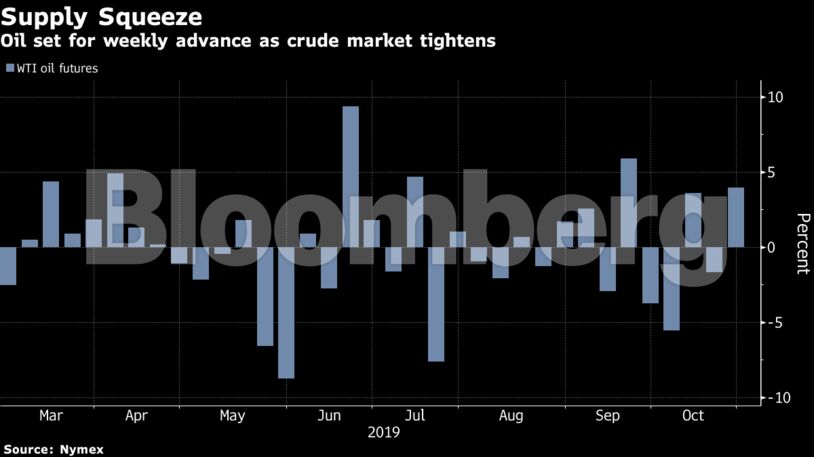

Futures were little changed in New York, on course for a weekly increase of more than 4%. U.S. government data on Wednesday showed a surprise pullback in the nation’s crude stockpiles last week, and on Thursday a critical North Sea pipeline was briefly halted by a power loss. Yet weak economic data from Germany and South Korea fanned concerns that world fuel demand is flagging, and the U.S.-China trade clash continued to put a dampener on investor sentiment.

“The near-term fundamentals are actually tight,” Abhishek Deshpande, head of global oil-market research at JPMorgan Chase & Co., said in a Bloomberg television interview. “If you were to see any positive trade dialogue emerging,” then “you could see a quick switch in investor positioning.”

Oil is down about 16% from an April peak as the trade spat between Washington and Beijing dents demand, though President Donald Trump has raised expectations that he and Chinese President Xi Jinping will sign a phase-one deal in Chile next month.

West Texas Intermediate for December delivery lost 10 cents to $56.13 a barrel on the New York Mercantile Exchange as of 10:18 a.m. London time. The contract added 26 cents to close at $56.23 on Thursday. Prices are up 4.4% this week, the most since the week ended Sept. 20.

Brent for December settlement was almost unchanged at $61.66 a barrel on the London-based ICE Futures Europe Exchange. Prices are 3.8% higher this week. The global benchmark crude traded at a $5.51 premium to WTI.

| Other oil market news |

|---|

|

Share This: