CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

David Yager – Yager Management Ltd.

Oilfield Service Management Consulting – Oil & Gas Writer – Energy Policy Analyst

The old saying goes in the investment business, “when the ducks are quacking you feed them”. And so it goes for Canadian publicly traded oilfield service (OFS) companies which are busily raising equity from the sale of treasury sales for working capital, balance sheet repair and possibly an opportunistic acquisition. Over the past year a number of companies have been able to raise money with the frequency of financings accelerating in the past three months. There are several factors at play – not all positive – but at least the lights are on in the public equity markets for companies which investors believe are poised to participate in the recovery of 2017 and hopefully beyond.

That OFS is notoriously cyclical need not be restated here. The collapse in oil prices resulted in a collapse in business for suppliers followed by, or often preceded by, a collapse in the share prices of publicly listed OFS companies. Listed companies generally trade at some multiple of their current or anticipated cash flow. When companies are cash-generating machines the market rewards them with high valuations. When it is clear cash flow is heading for zero or less, trading prices for their shares respond accordingly.

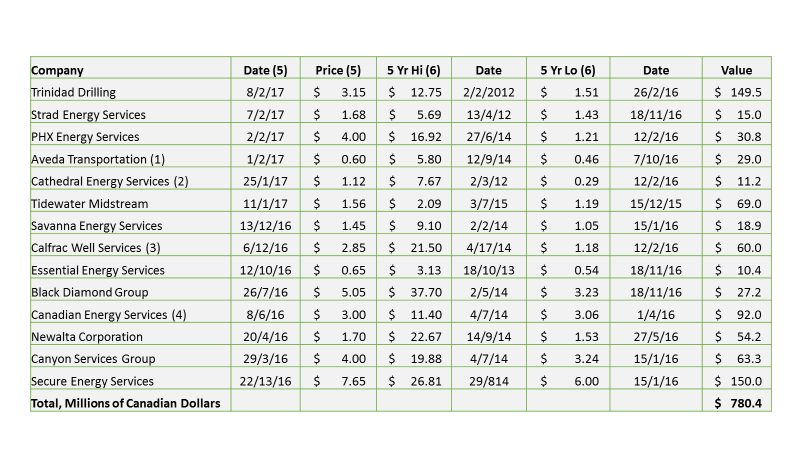

The following chart is a cross section of companies that have been able to raise equity (or have announced equity issues) in the past year, the share price the deal was done (or will be done) at, the gross proceeds before expenses from the offering, and a reference of the recent issue price to the five-year highs and lows. In total these 14 companies have raised over three quarters of a billion dollars.

1) Not closed at time of writing. Value equals maximum proceeds from two concurrent private placements

2) Not closed at time of writing

3) Adjusted for 2:1 share split July 2014

4) Adjusted for 3:1 share split July 2014

5) Source: Company news releases

6) Source: Google Finance 5-year stock price chart

The use of proceeds of the financings are varied but the bias is towards debt reduction or balance sheet repair, a problem not uncommon in OFS after two years in the trenches. This will give the companies the flexibility with their credit facilities to access working capital to pursue new business as it comes in the door. Canadian Energy Services & Technology Corp. and Tidewater Midstream and Infrastructure Ltd. specifically noted they were raising the money for acquisitions and expansion of the business.

The comparison of the share price of the recent equity issues and the price history of these companies over the past five years show that oilfield services – at least as defined by these companies – is a hardly a “buy and hold” proposition for investors. The problem for everybody in this cyclical business – from shareholders to founders to managers to staff and even clients – is managing the expectations of all key stakeholders through the cycles in the business.

Averaging of above data reveals the perils this sector for shareholders. This is not unique to oil. The same volatility is associated with virtually all commodity-driven businesses. For the 14 companies the average price of the recent equity issues is 77% below the average of their five-year highs. Most of the peaks were in 2014 when oil was still on the sunny side of US$100 a barrel. All but one of the five-year lows were last year with a heavy bias towards the first quarter when oil traded as much as 75% less than in June of 2014.

There were several reasons why equity issues have been somewhat sporadic. Managers looked at their current versus historical share price and concluded the cost of equity was too high until all other options had been explored. This was assisted by investors who were reluctant to make a move until they were confident they were buying at the absolute bottom of the cycle. Since the downturn began there have been multiple announcements of the creation of new, special purpose pools of capital designed to buy cheap and exploit the recovery. But for the longest time few deals were done.

However, when oil prices stabilized halfway through last year and a de-facto floor was set under crude by November’s OPEC supply-management decision, the phone started to ring. OFS operators, starving for working capital with no capacity to borrow after two years of deteriorating financial performance, figured the upturn was no time for heroics about protecting share value. If a recovery was underway and you couldn’t even go to work because of a working capital shortfall, what was the point of being in business?

Therefore, the necessity of raising money coinciding with the creation of a basement resulted in willing sellers and buyers for the first time in a long time. Deals are getting done and if commodity prices and capital spending plans hold or improve, it is likely more money will be raised over the course of 2017.

Of course, waiting until the risk was reduced was punishing for the self-declared bargain hunters. If you’re a savvy investor and know when and how to play the OFS cycles, there was a bunch of money left on the table. The above equity issues are on average 73% above the five-year low share prices (this methodology is not dollar-weighted). There were some fabulous bargains during the absolute depths of despair for the Canadian oilpatch. In terms of names, PHX Energy Services and Cathedral Energy Services raised or are raising capital at more than double their recent low prices. Only one company – Canadian Energy Services and Technology – raised money below their five-year low but the difference, only $0.06 per share, is hardly material.

The simple lesson is you buy oilfield services shares when everybody hates them then sell when they are popular. But knowing investor psychology, selling at the top is always easier than buying at the bottom. Capital markets are full of so-called “contrarians” with track records demonstrating varying degrees of success. It would have taken a lot of courage to buy some of the above names in the first half of last year when their major news announcements were how many people they had laid off, how many assets they were selling to keep the lights on, or the latest blow-by-blow description of yet another covenant amendment with their senior secured lender. This was against a backdrop of major and minor OFS operators going bankrupt after lenders called their loans because the likelihood of their recovery was deemed hopeless.

Volatility in oil prices and share values is once again well understood. What is less understood is the volatility of OFS to be able to respond to a ramp up in business. While clients took full advantage of lower prices created by significant OFS overcapacity, most vendors lived on their balance sheets while trying to figure out when and where the bottom was and how to respond. Because exploration and production (E&P) companies have focused on their own survival rather than that of their supply chain, that their purchasing policies had left vendors in many cases too broke to do more business has recently become obvious as operators resume spending.

While the publicly-traded companies have the advantage of transparency, liquidity and the ability to raise equity at whatever the price, many private companies are also up against the wall at the bank and will have difficulty finding equity investors at any valuation. What is interesting about the valuations of some of these companies as they raise equity is the price is based on assets and the future, not the past. If share price valuations were based on enterprise value – a key component being trailing EBITDA – a lot of these companies would have negative value.

In the U.S. the chequebooks are also out for OFS equities. Bloomberg News reported February 8 that in January alone oil and gas outfits raised US$6.64 billion in 13 equity offerings, 22% of which went to OFS operators. Higher demand has lifted prices. Weatherford interim CEO Krishan Shevram was quoted as saying, “We’re seeing signs of improved pricing of roughly 25 percent on average, versus December levels. There is considerable optimism.”. Fracker Keane Group raised US$508.4 million on January 20 for an Initial Public Offering, the first U.S. OFS IPO in a long time.

Nice to see a pressure pumper going public when a year ago the entire sector was struggling under massive debts which claimed private Canadian success story Sanjel Corp.

Considering where OFS has been, this should all be considered good news. Oil prices are up. E&P companies are going back to work. OFS operators are raising the capital they need to supply goods and services. Prices are rising out of necessity. Investors are writing cheques because they think they will make money. The only way this will happen if the combination of client spending and OFS delivery results in positive cash flow for the service sector, which it will. Finally.

See David Yager’s Corporate CV

List of David Yager’s Consulting Services

David Yager can be reached at Ph: 403.850.6088 Email: yager@telus.net

Share This:

COMMENTARY: Activists Suddenly Care About LNG Investors