CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Yager, November 9, 2016

Entrepreneur. Consultant. Journalist. Political Activist.

The greatest gift to shareholders of a vast array of global oilfield services (OFS) firms in the past 20 years has been the entry of storied industrial giant General Electric Co. into the sector. Starting in 1994 GE began buying companies supporting oil and gas development, transportation or processing. By 2015 GE had invested well over US$15 billion around the world. The table below shows US$14.875 billion of disclosed deals. Four transactions of undisclosed value pushes the total higher.

When the target companies were public GE usually offered a handsome premium to market, often in the 1/3+ range. Virtually everything GE wanted GE got because of the strength of its balance sheet and the conviction of its vision. OFS was going to be a significant part of the conglomerate’s future. GE faced little resistance from reluctant sellers searching for higher offers once GE’s offer price was revealed. Private equity – which often employs its own capital to unlock shareholder value – were sellers not competitors. They had bought control of companies in prior years then were delighted to sell to GE at a substantial profit.

When GE started making major OFS investments a decade ago this writer wondered what attracted GE to this notoriously cyclical business. GE was not just another company with cash to burn. Starting in 1879 with the commercialization of the electric light bulb, GE has always been at the forefront of the next big thing for the industrialized world be it railroad locomotives, aircraft engines, health care, industrial water treatment or renewable energy. GE used its financial might, marketing skills, distribution network, management experience and technological expertise to become major players in whatever business segment it chose to enter.

Books have been written about the genius of GE’s legendary management techniques and financial discipline. When the now famous Jack Welch was GE’s CEO he implemented the “Sigma Six” industrial and business process improvement system in 1995. Sigma Six came out of Motorola a decade earlier. This signaled GE was going to be best it could be at everything it did. After retiring Welch wrote a bestselling book about how to make businesses great. Not often discussed was while GE was outwardly purporting to be a leader in efficiency and processes in heavy industry, a pillar of its earnings was consumer and corporate financial services through GE Capital. Even poorly run banks usually make money.

GE began expanding into OFS through the compression business which appeared logical. More big things that rotate and reciprocate. Turbines driving huge compressors were similar to jet engines. But by 2002 GE was expanding into highly specialized OFS niches like electronic internal pipeline inspection. In 2007 and 2008 GE was full-on OFS with wireline logging systems, subsea wellheads and blowout preventers, products with zero multiple-market opportunities. GE made major investment in subsea and natural gas transportation hardware, both expanding sectors.

Looking back to early this century when GE start emptying the vault for OFS in a big way, GE’s expansion mirrored what will surely be remembered as one of – if not the – greatest and most stable period of expansion for the upstream oil and gas industry in history. Everybody in the OFS looked smart, GE included.

The official line goes today’s oilpatch is a high-tech marvel. While certain elements of it rely on interesting new technology and more is being deployed every day, much of the process of finding and extracting oil and gas remains so low-tech to suggest otherwise should be embarrassing. In 2013 GE paid US$3.3 billion for Lufkin Industries Inc., an early inventor of the pumpjack. Founded in Lufkin, Texas in 1902, Lufkin pumping units became the industry standard because they were so decidedly low tech. The horsehead pumping unit is a simple piece of equipment that rarely quits and something even the most inexperienced or poorly trained field hand can operate and maintain.

This is in sharp contrast to the message on GE’s website today which is “We are repositioning GE to be the world’s best infrastructure and technology company”. On another page GE’s purpose reads, “We are transforming GE into the world’s premier digital industrial company using our scale and diversity to drive outcomes for customers.” That the product line of Hydril blowout preventers GE paid over US$1 billion to acquire is congruent with this strategy was not obvious when they bought it eight years ago or today.

GE’s 23 Year Acquisition Binge

- Company purchased may be all the shares or only divisions, assets or product lines

- MM millions of U.S. dollars, ND Not Disclosed

Which leads us to the October 31 announcement GE is repositioning its oil and gas division through the acquisition of 62.5% of Baker Hughes Inc. for US$7.4 billion and the contribution of its businesses and assets into the new company. Trumpeted as a global competitor to long-established OFS giants Schlumberger Limited and Halliburton Company, the merged GE Oil & Gas/Baker Hughes is reported to have revenues of US$24 billion next year, number two in the world. Some US$1.6 billion in synergies and SG&A cuts have already been identified. Every attempt has been made to put a positive spin on the deal which is predictable now that GE is the controlling shareholder. GE doesn’t make bad decisions.

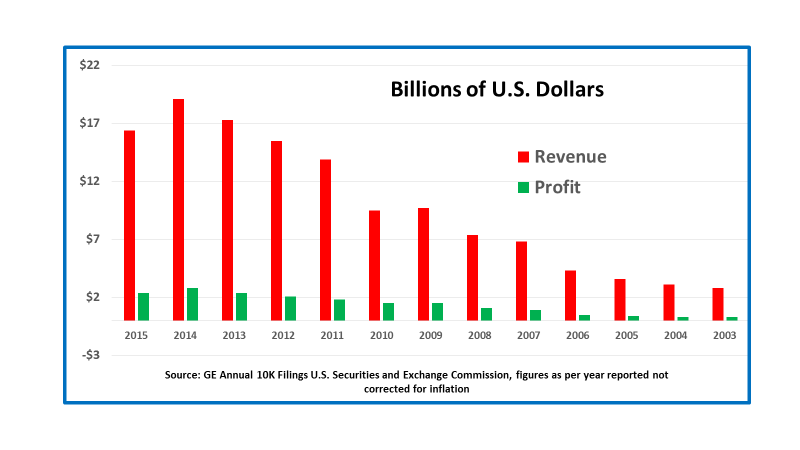

12 Years of Growth (except 2010) Followed by 2015

GE’s US$15+ billion investment grew the top and bottom line. The above graph shows GE’s Oil & Gas business unit growing from revenue of only US$2.8 billion in 2003 to its peak of US$19.1 billion in 2014, a year when everybody in OFS worldwide had what might be their best year in a long, long time. It was always profitable. In 2014 the division contributed profits of US$2.8 billion, 29% of the company’s US$9.5 billion total. GE Oil & Gas did this with only 16% of total revenue meaning GE’s OFS investments were more profitable by comparison that other GE business units.

In 2015 Oil & Gas revenue shrank by over US$2.5 billion but still contributed with 14% of total sales and a U$S2.4 billion divisional profit. But last year GE took a US$7.5 billion write-down as it exited financial services resulting in significantly lower profits. As 2015 progressed it became evident 2016 was going to be even worse as everybody’s oil and gas company global client base continued to wind down capital projects upon completion without replacing them. Half the world’s offshore rigs GE invested so heavily to support are idle today.

The trade press reports the very day the Halliburton/Baker Hughes merger was called off on May 2, 2016, GE picked up the phone and called Baker Hughes. After six months of discussions and negotiations the GE/Baker combination was announced.

While nobody has expressly said this, what this transaction done this way means is GE is positioned to exit OFS. Owning 62.5% of the combined entity is a problem. Public capital markets don’t like investing in companies with huge control positions unless the controlling shareholder will eventually purchase the minority interest. When Baker Hughes’ stock declined after the announcement the market didn’t anticipate an offer from GE for the rest of the shares was forthcoming.

On Friday November 4 Baker Hughes had a market cap of US$24 billion. This gives GE’s 62.5% an implied value of US$40 billion after the deal closes next year. Based on 2015 divisional profits of US$2.4 billion this is a trailing value of 17X 2015 profit. But 2016 was much worse for everybody. Nobody is going to write GE a US$40 billion cheque for this division in this market for a valuation which is probably three times 2016 revenue. For the nine months ended September 30, 2016 30 GE’s SEC filings reported closed orders of US$7.7 billion this year compared to US$11.8 billion for the same period in 2015. But the good news for GE is its outstanding order book has not diminished as much on a year-over-year basis.

More importantly, the outlook for a major recovery – defined as anything near the capital spending that took place in 2014 and the years prior thereto – looks increasingly unlikely in the short or even medium term. It is no longer just about oil markets and what OPEC may or may not do. On November 4, the Paris climate change commitments became binding for the 55 countries that ratified them. Oil is no longer a miracle source of energy but the end of the world as we know it. GE is invested heavily in renewable energy as well as hydrocarbon fuel. While the end of oil will probably take longer than its opponents hope, both cannot win. Government and public support for capital investment is on the side of renewables, not more oil.

As much as the spin may indicate this is a strategic move towards a globally-competitive “one stop shop” for clients through an integrated OFS provider, it is also defensive financial engineering. After the deal was announced the Wall Street Journal ran a headline stating, “With Oil Deal, GE CEO Immelt Revamps His Strategy”. That was the nice part. The first paragraph read, “Jeff Immelt steered General Electric Co. out of the financial crisis and straight into the depths of a global oil rout. Now, GE’s chief executive is expanding his wager on the battered energy business through a combination that unloads much of the risk onto shareholders of a proposed new company. He is calling GE’s planned merger of its oil-and-gas unit with Baker Hughes as opportunistic bet on the recovery in the energy sector, dismissing the idea the deal would shrink GE’s industrial reach by spinning off assets”.

Others were more generous. In a post on website InvestorPlace a commentary was titled, “The Real Reason … GE Bought Baker Hughes”. It is all about Predix a GE investment in expanded applications for the internet in industry. The article read GE touts Predix as, “the operating system for the Industrial Internet (which) is powering industrial businesses that drive the global economy. By connecting industrial equipment, analyzing data, and delivering real-time insights, Predix-based apps are unleashing new levels of performance of both GE and non-GE assets”. Apparently GE is going to take all that information from all it and Baker’s products and services and deliver value for its clients.

The trouble is packers, blowout preventers, wellheads, pumpjacks and other “pig iron” equipment don’t have much of a story to tell. You can certainly monitor and automate everything, but that is hardly a business concept on which GE has a hammerlock. This is not to say GE isn’t applying technology to upstream oil and gas because it is. But smarter equipment and services delivering greater value to clients provides little protection from a massive cyclical contraction of this industry when clients re almost totally obsessed with cost until commodity prices recover. Productivity improvements will be important once the industry stabilizes but at these oil prices cash management is paramount.

By controlling a listed OFS company GE will realize greater value and liquidity than owning a significant but shrinking division of assorted assets nobody will likely buy. To satisfy public markets GE will probably own less of GE/Baker Hughes over time than more. This will happen by dividending out Baker Hughes stock to GE shareholders or gradually placing large blocks with institutions who like the story.

Bloomberg News reported this deal could be good for the CEO’s compensation packages and other shareholders as the combined company delivers greater future earnings than GE’s stand-alone Oil & Gas division. Probably true. But that doesn’t mean GE has to be in the business forever.

Over the years GE has invested heavily in assets and industries that looked promising or experienced strong growth. It then divested them when the market matured. GE sold its trademark home appliances division twice after the first sale was blocked by European anti-trust agencies. It has also largely exited financial services.

Looking back at GE’s 137-year remarkable history the company has been in and out of a dizzying array of industries and sectors. The idea the company would declare OFS a core asset after this business has endured such a punishing correction leading to an uncertain future ignores the history and flexibility of the company.

About David Yager – Yager Management Ltd.

Based in Calgary, Alberta, David Yager is a former oilfield services executive and the principle of Yager Management Ltd. Yager Management provides management consultancy services to the oilfield services industry in a number of areas including M&A, Strategic Planning, Restructuring and Marketing. He has been writing about the upstream oil and gas industry and energy policy and issues since 1979.

See David Yager’s Corporate CV

List of David Yager’s Consulting Services

David Yager can be reached at Ph: 403.850.6088 Email: yager@telus.net

Share This:

COMMENTARY: Workers Must Be Part of the Energy Transition – Resource Works